Macro View

The factors that investors evaluate to determine valuation and risk have changed dramatically over the past five months, which has shifted expect returns lower. Here is a summary of the changes in the factors investors are evaluating:

- The global economy is slowing instead of expanding as initially thought. The spread of the Delta variant put a damper on last year’s economic recovery. This year, the Russian invasion of Ukraine has slowed global growth as resources shift to support the war. A prolonged war will further impede global economic growth.

- The Federal Reserve has indicated an intention of pulling its stimulus out of the market. During the pandemic, tremendous fiscal and monetary stimulus was thrust into the capital markets and economy. Stimulus has the effect of inflating asset values; the absence of stimulus will allow asset values to decline.

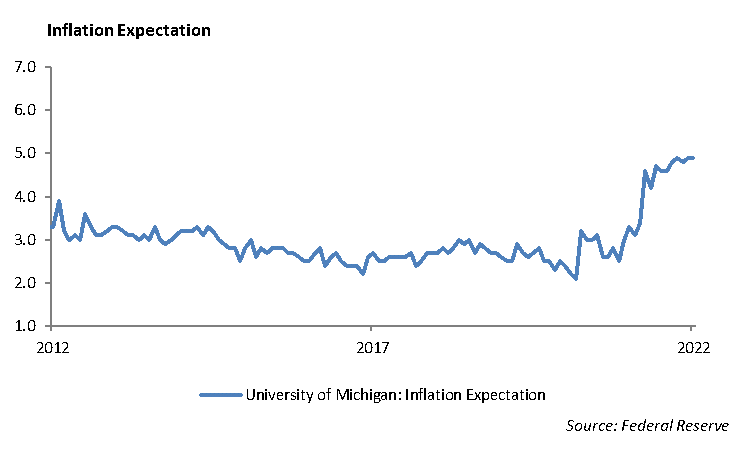

- Inflation has accelerated over the past year well beyond the Federal Reserve’s target of 2%. CPI is running at an annualized rate of 8.5%, its fastest pace since December 1981. Inflation expectations based on the University of Michigan Survey are running in excess of 5%.

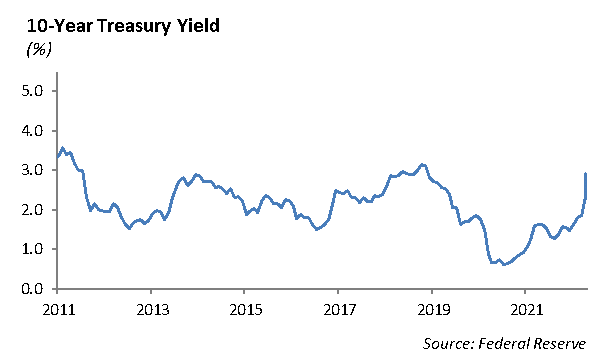

4. Interest rates have increased sharply with the yield on the 10 year US Treasury at 2.93%, its highest level since 2018. Higher interest rates have translated over to high mortgage rates with a 30 year fixed rate mortgage now over 5%.

5. According to FactSet, of the companies reporting earnings this past quarter, roughly 80% have beaten analyst expectations. However, corporate earnings are showing signs of slowing. Recent earnings and guidance from Netflix cast a cloud over the market. Downbeat reports from retailers, healthcare and technology companies helped to contribute to a significant sell-off last week in domestic equities.

The Federal Reserve’s Push to Neutral

The Federal Reserve has indicated that it would like to get back to neutral on its policy. We are not sure where neutral is, but with that said, we expect the Fed will move expeditiously to reduce the size of its bond portfolio and continue to push interest rates higher from here. The battle to get control over inflation is, in some regard, out of the Fed’s control. To the extent that inflation is a function of increased demand for goods and services, increasing short-term rates will help to curb demand.

However, much of the increase in the rate of inflation is due to supply/demand dislocations and supply chain disruptions. These structural issues will take time to sort out. For example, if a U.S. company decides that it is going to relocate manufacturing from China, it will need to identify a new site, build the facility, and hire labor. All of this takes time and increasing interest rates will only compound the expense of fixing the supple chain problem. Increasing short-term interest rates to dampen demand will complicate fixing supply chain issues.

Fixed Income

Interest rate volatility remains elevated with credit spreads wider so far this year. Markets seemed in gridlock as both buying and selling bonds at reasonable levels was difficult. With interest rates rising, fixed income investors are growing loss constrained which is further impeding liquidity in the market. Conversely, the Fed’s aggressive narrative around tightening monetary policy and raising rates has many bond investors scared to buy as the momentum for rates is currently to the upside.

The bond market is currently pricing in a total of 2.75% increase in short term interest rates from the Fed in 2022. While the Fed’s aggressive shift in policy is an attempt to reduce inflation that is at its highest rate in 40 years, the reality is that a massive shift to tighten monetary policy will have an adverse effect on economic growth. The consumer sector is showing signs of weakening due to negative real wage growth, more expensive housing, and low savings rates. Consumer confidence is below pandemic levels, which can create a self-fulfilling slowdown in the economy. We do not believe the Fed will be able to raise rates seven times this year. If the economy does begin to slow, we would expect inflation to naturally decline and the Fed would likely pivot towards a pause in their tightening policy. Ultimately, this would lead to a positive for risk markets and we would expect spreads and rates to fall.

Equities

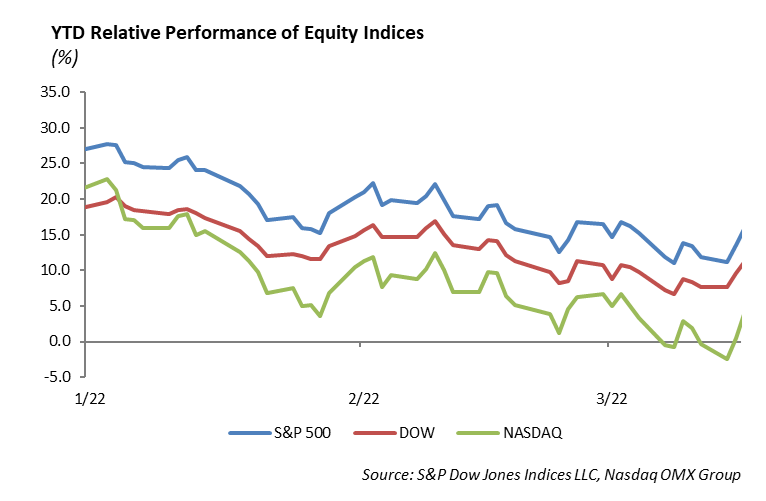

The major indices suffered heavy losses on Friday, sending the S&P and the Nasdaq down almost 3%. The S&P is down 10% for the year and the Nasdaq is down 18%. Last week, only real estate and consumer staples finished slightly in the green. Health care, materials, and energy dropped 4%. Communication services was hit the hardest; this was due to a huge disappointment on Netflix earnings, sending shares of the entire sector down 8% for the week.

Netflix [NFLX]

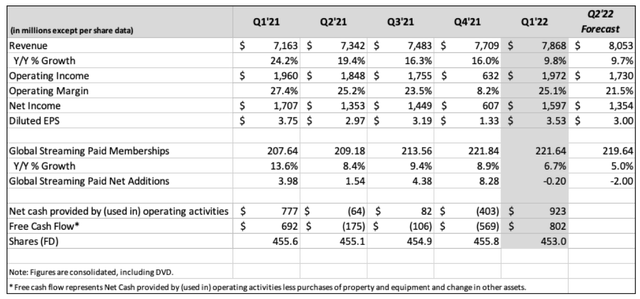

Netflix reported a net loss of 200k subscribers in the first quarter, its first ever loss. They lost 700k paid subscribers in Russia after suspending its service. The company expected 2.5 million subscriber adds, so even excluding Russia, they would have missed expectations by 2 million. For the first quarter, Netflix earnings were $3.53 per share on $7.87 billion in revenue. For the second quarter, Netflix expects to lose 2 million subscribers and earn $3 per share on $8.05 billion in sales. The company also suggested that 100 million households are watching without paying, compared to its 222 million paying members. Moving forward, Netflix will work on an ad-supported tier to boost growth. Shares of the company fell 35% and are down 64% this year after two terrible quarters in a row. The continued risks in competition and the difficulty the company is facing in growing subscribers makes Netflix a risky holding at the current time, with no real catalysts to suggest a rebound in shares.

Johnson & Johnson [JNJ]

Johnson & Johnson reported earnings of $2.67 vs. $2.58 expected. Revenue was $23.4 billion, missing expectations of $23.6 billion. Revenue still grew 5% year over year. JNJ reported $12.87 billion in pharmaceutical sales and $6.97 billion in medical device sales. These segments were up 6% from last year. The consumer health business declined 1.5%, but is spinning off into a separate company. The Covid vaccine brought in $457 million in total revenues. The company lowered both its full-year revenue and earnings outlook and did not provide guidance for its Covid vaccine. The company is trading 3% higher on the news. Johnson & Johnson is up 6% this year, outperforming the S&P and the health care index. The company is still trading fairly cheap at 17x earnings, but there are other peers that are trading even cheaper and offer better opportunities at current levels. This includes Merck (MRK) at 12x forward earnings and Bristol-Myers Squibb (BMY), trading at 10x forward earnings. Although this remains a core holding in any portfolio, we would prefer to add to these names at current levels.

Here is What Investors Should Consider Heading Into the Summer

- Income-oriented investors have the ability to reinvest at higher rates and wider credit spreads. Consider selling short maturing bonds and reinvesting out the yield curve and wider spreads. With the US Treasury at 2.90% and BBB spreads at +150 bps, yields are at 4.40% now.

- Income-oriented investors should consider municipal bonds. Investors can earn 3% in high quality municipal bonds out 15 years. There are bargains out there if you are patient.

- Stay away from leverage including closed end funds. It’s still too early.

- Domestic equity is all about valuation. There is no need to run away if you are a stock picker.

- This is a wonderful entry point for growth companies with solid business models and recurring revenues. This includes companies like Microsoft and Alphabet.

- We are not in retail or health care right now.

- We are still in defense stocks, including Lockheed Martin.

- Dividend stocks have performed better than the broader market. Be careful to not overweight financials through that allocation.

- In REITs, we are invested in data warehouses and multi-family.

- Use the equal weight ETF to diversify the concentration in the S&P 500.

- Cash is higher in all of our portfolios and strategies. This is a tactical strategy and not market timing. Cash is a way to preserve principal in periods of high volatility.

- We are significantly underweight International and Emerging Markets. There is no significant catalyst for us to allocate to those sectors at this time.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2022 Winthrop Capital Management