This was supposed to be the year of economic recovery after a two-year pandemic nearly destroyed the global economy. However, the International Monetary Fund (IMF) recently reduced its growth forecast for the world economy. According to its latest World Economic Outlook, published in January, the IMF now expects global gross domestic product to grow 4.4% this year, down from its October 2021 forecast of 4.9%. The 2022 World Economic Outlook will be released April 19.

The war in the Ukraine is compounding a global slowdown in economic growth, contributing to supply chain disruptions and dislocations in trade, and accelerating the rate of global inflation. Layer on top of that rising interest rates, the sanctions on Russia and the posturing with China and their potential support for Russia, and there is the potential for stagflation in Europe. We are moving through shifts in global trading relationships, which will have long-term impact on how the global economic machine functions. We are moving away from globalization and trade integration.

The Shifting Landscape of Global Trade

In 1989, the Berlin Wall fell, leading to the reunification of Germany the following year. Then, in 1991, the U.S.S.R. was dissolved after Mikhail Gorbachev‘s two major reforms, glasnost and perestroika, failed to save the Soviet conglomerate and made all the world maps in elementary schools obsolete. This also led to the end of the Cold War, which allowed for more integrated world trade. The World Trade Organization (WTO) was established in 1995 to provide a system for member countries, including China and Russia, to trade amongst each other.

However, the trade war between the United States and China is now moving into its fourth year, and the sanctions placed on Russia following its invasion of the Ukraine last month have begun to dismantle several pillars of global trade. We are seeing signs of moving back toward a system of trading blocs where countries trade with preferred countries and away from globalization that supported global growth over the past three decades.

Over the past forty years, China and Russia have been considered emerging economies and both the yuan and ruble have been considered unstable. The U.S. dollar was initially positioned as the reserve currency following the Bretton Woods Agreement in 1944. Most global trade settles in U.S. dollars, which provides substantial support to the value of the U.S. dollar. However, China has required its trading partners to settle in yuan with its global trade. This past month, Russia has announced that its trading partners must settle in rubles. This will provide momentum to shifts toward trading blocs and preferred trading relationships, undermining the WTO.

Equity Valuations Slightly Elevated

With the S&P 500 trading at 4463 and earnings expected near $181.38, the S&P 500 is currently trading at a Price/earnings multiple of 24.6 times. In the context of historical data going back to 1880, this is an elevated valuation level relative to the 15 to 18 times multiples. However, in the recent market context supported by aggressive monetary and fiscal stimulus, this appears to be a slightly elevated valuation.

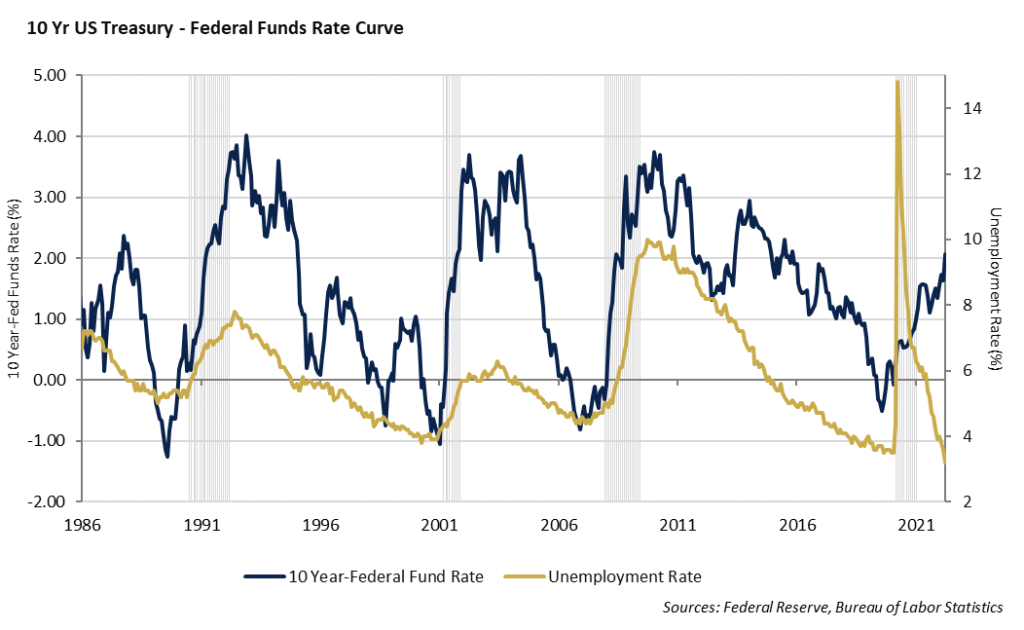

The inherent risk to this perspective is that the earnings part of the equation is actually achievable. The yield on the 10-year US Treasury is now at 2.75% and the yield curve is flattening. The risks of a global economic slowdown are increasing. With rising inflation, rising interest rates, a labor shortage, and shifting demand, the risks to S&P 500 earnings are to the downside.

The S&P fell 1.27% last week, bringing its year-to-date decline to 6%. After a slow start to the year and subsequent rebound, the index has been struggling to go positive for the year. Technology and communication services led the decline last week with each sector falling 4%. In general, cyclical sectors have been crushed recently, which includes industrials, discretionary, technology, and financials. The health care and energy sectors both climbed 3% last week. Defensive sectors outperformed again, with staples and utilities also finishing positive for the week. Additionally, small caps fell over 4% and the semiconductor ETF fell 8%. These two sectors often gauge the direction of the economy. The semiconductor index is now close to lows for the year, and down about 21%.

Earnings season is set to begin this week with Financials reporting. This includes JP Morgan, Citigroup, Goldman Sachs, Morgan Stanley, PNC, and Wells Fargo. The current estimate for quarterly earnings is $51 per share, putting 12-month earnings per share for the S&P at $211. This implies a valuation on the index of 22x earnings. Although this is historically high, this is well off highs from last year when the index was trading over 30x earnings. Earnings surprises have been quite positive over the last few years and the level of beats have been high. However, this has moderated in recent quarters and we expect the beats to be closer to the 15-year average of 5.3%.

The Federal Reserve

After growing their balance sheet to $8.95 trillion through the period of the COVID pandemic, the Federal Reserve is finally preparing to take their foot off the stimulus accelerator. A combination of supply chain issues, fiscal stimulus, and record low interest rates has fueled inflation that the U.S. has not seen since the 1980s. The Fed has begun a tightening cycle by shifting the Fed Funds rate target up 0.25% and signaled the intent to increase rates a total of seven times in 2022. Further narratives out of the Fed have demonstrated a move to reduce the balance sheet rapidly and potentially increase rates by 0.50% in May.

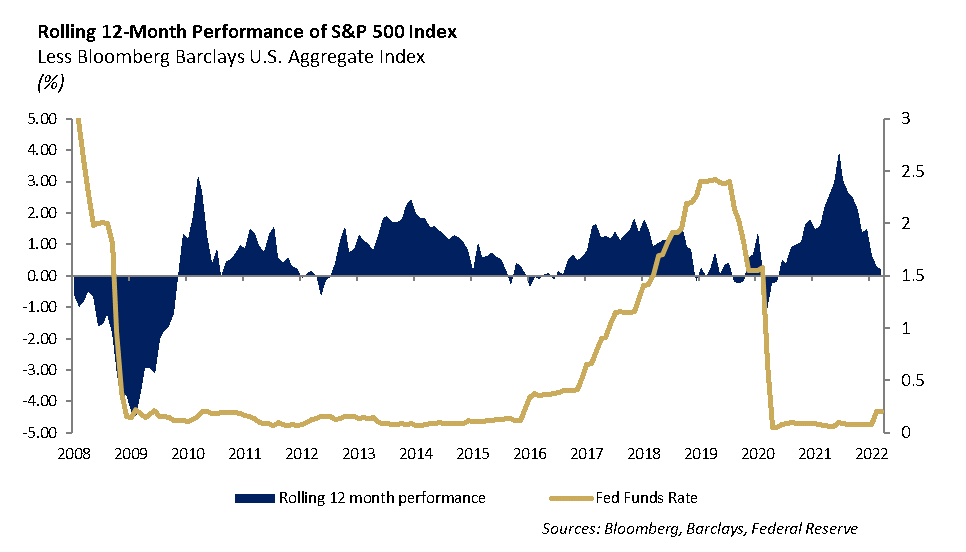

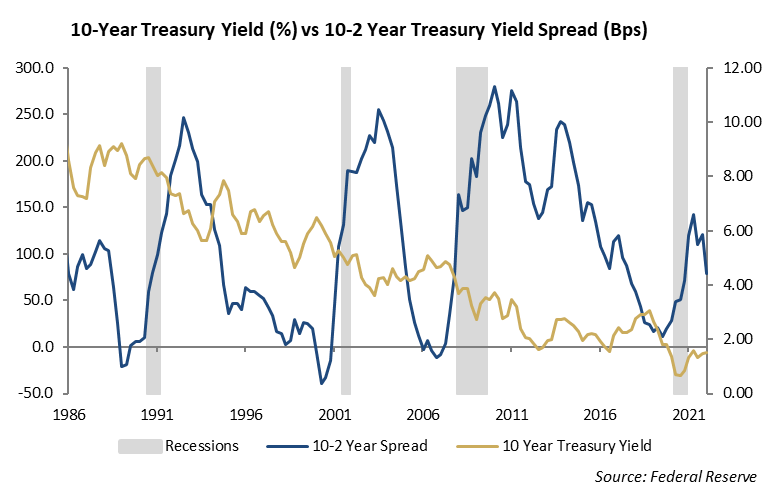

Either the Fed believes the economy is strong enough to handle more aggressive tightening, or they are willing to sacrifice economic growth to get in front of rapid rising inflation. We believe the economy is not as strong as the dialogue would suggest. Real wages continue to decline and savings rates are back to pre-pandemic levels, leaving consumers to begin reducing their discretionary spending. The yield curve from the 2-year to the 10-year U.S. Treasury rates has declined from 1.60% to 0.16% over the past 9 months. The bond market is foreshadowing an economic slowdown and the Fed is backed into a corner trying to get ahead of inflation and reduce its massive stimulus. If the Fed follows through and increases short-term interest rates 1.5% to 2.0% this year, we expect economic growth prospects will decline sharply by 2023. We expect the Fed will sacrifice economic growth in order to get inflation under control.

Fixed Income

The rate on the 10-year U.S. Treasury has increased by 1.30% in 2022 and is currently trading at 2.75%. This is now in line with where interest rates were in 2018-2019 prior to COVID spreading globally, following the Fed’s last initiative to tighten monetary policy. Credit spreads have widened over 0.50% on investment grade corporates as market volatility has increased. We continue to see value in high quality corporate debt of companies with negative net debt and rationale for a rating upgrade.

With the exception of COVID-impacted sectors such as airlines and hospitality, credit quality has held up remarkably well over the past several years. However, we see growing risks in the credit markets. The increase in the collateralized loan obligation market has shifted credit away from bank lending toward institutional investors. With this shift, credit risk will be borne by the markets, less the financial system. The growth in private credit markets and the business development (BDC) structures will further compound the growing risks in the credit markets. We believe in a credit cycle.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2022 Winthrop Capital Management