Macro View

Our concerns of a slowing economy were laid bare over the past two weeks as the Commerce Department reported a decline in Gross Domestic Product of -0.4% for the first quarter of 2022. This was the first decline since the early days of the pandemic, and a reversal of the 1.7% growth seen in the fourth quarter of 2021.

The decline in economic growth is a function of the continued supply chain disruptions, ongoing trade disputes, overhang of the Omicron variant, and increased raw material and labor costs. While the consumer sector, which represents the largest portion of the domestic economy, continued to grow during the quarter with a 0.7% increase in spending in spite of rising gas prices, fears of a slowdown are growing. The soaring cost of living resulting from the increasing rate of inflation is chipping away at consumers’ spending power.

In the face of a decline in monetary and fiscal stimulus, which has helped support asset prices over the past 15 years, prices on publicly traded securities appear vulnerable to increased volatility and further declines. The Federal Reserve increased short-term interest rates by 0.50% last week in an effort to subdue the accelerating rate of inflation. At the same time, the economy is slowing and real wage growth has declined over the past four quarters. In other words, the average American has less to spend today after adjusting for the impact inflation has on rising prices.

In order to sustain growth, the economy needs demand for goods and services to remain strong; however, the Fed’s push for higher rates is intended to reduce demand. The conundrum appears to be that the Fed is willing to sacrifice economic growth in order to have the perception of credibility with respect to fighting inflation. This does not bode well for stock prices.

Fixed Income

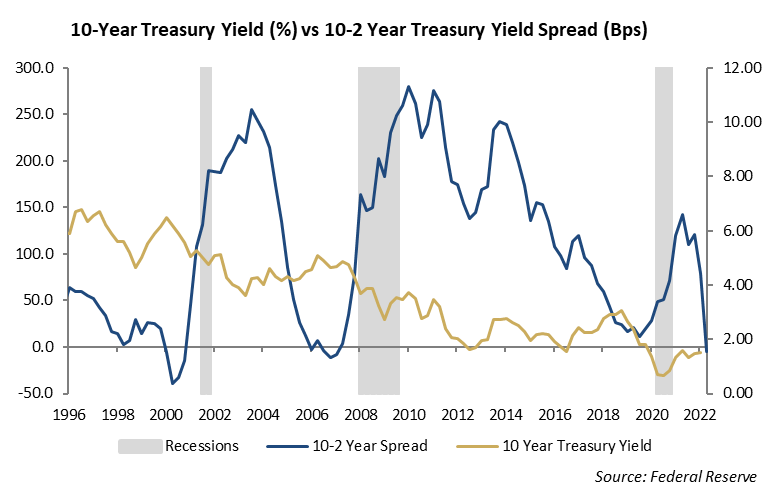

The yield on the ten-year U.S. Treasury note closed at 2.89% at the end of April and then surged to 3.09% last week. The month of April was the worst month of fixed income performance in over ten years. The spike in yields of over 0.50% in the month is the highest one-month move since 2009. The Federal Reserve raised its target for short-term interest rates by 50 bps at last week’s meeting and further reduced its balance sheet portfolio of bonds. The accelerating rate of inflation has forced the Fed to pivot its focus away from the economy and labor markets toward addressing price stability.

With the sharp rise in bond yields, the yield curve has steepened. We expect that as evidence of a slowing economy accumulates, the yield curve will eventually flatten and the 10-2 year spread will approach zero.

With the rise and interest rates, spread volatility has increased with credit spreads on corporate and municipal bonds widening to levels not seen in several years. This has created a wonderful buying opportunity for income-oriented investors who can now earn 4.5% on ten-year BBB bonds. With the economy showing signs of slowing, further increases in short-term interest rates will compound the recovery as floating rate debt reprices at higher rates, resulting in increased interest expense. This will put more pressure on corporate earnings, which are already pinched from higher labor costs and increased corporate expenses.

Investment Strategy

In portfolio management, security valuation matters. Markets have a way of adjusting to new inputs with the result being a change in the underlying valuation. Both equity and fixed income investors are navigating difficult markets this year as the potential for slowing economic growth, slowing corporate earnings, rising inflation, and rising interest rates bear down on the capital markets.

With the increase in interest rates and widening in credit spreads, investors in the bond market are now able to earn a 4.5% yield in ten-year investment grade credit. In addition, municipal bonds have become much more attractive investments as yields moved to over 3.5% in the ten-year area.

We expect inflation to slow from its current 8.5% pace in the second half of the year, but remain elevated above the 2% target. We expect improvement in supply chains, which will help improve costs for semiconductors and appliances.

The stock market decline this year has been brutal for investors. While forward price-to-earnings ratios have declined from 21x to 17.7x today, they are still trading above their long-term average of 17.1 times earnings. The technology sector has been hit the hardest and many of last year’s darlings, which include Netflix and Amazon, are down by -70% and -31% so far this year. With technology representing nearly 40% of the S&P 500, it is no wonder the index is down -13.5% so far this year.

We are not advocates of trying to pick the bottom of a market. Valuations are getting more interesting and we expect to shift portfolios and put some cash to work in both stocks and bonds.

Equities

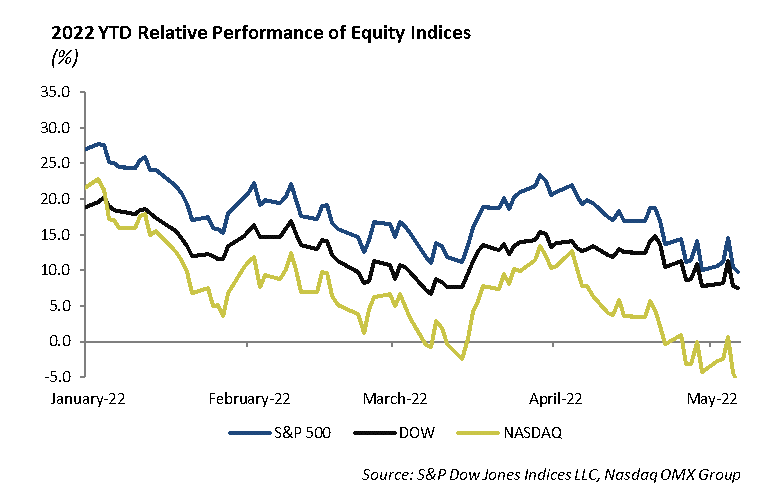

Investors are facing the most treacherous equity market in over a decade. The S&P 500 is down 17% from its high, and the NASDAQ is down over 24% so far this year. At the same time the volatility of the stock market pushed to new highs last week.

The decline in the S&P 500, which recently traded below 4000, was nearly 9% in the month of April. For the first four months of the year, the Nasdaq suffered its worst losses on record.

Investors are facing a myriad of challenges including a shift toward tighter monetary policy, an eminent slowdown in the economy, rapidly rising inflation, and slower earnings growth. The abrupt decline in stock prices brings equity valuations more in line with historic norms. The S&P 500, for example, is trading at 17.7 times forward earnings and approaching its 10 year average of 17.1 times earnings.

So far, the best performing sector is energy which despite the selloff in the broad market, ended the week up about 3%. The worst performing sector was consumer discretionary, which fell over -6%.

With disappointing first quarter earnings from Amazon last week, investors turned their attention to other online retail companies. These included Etsy, eBay, and Wayfair. Earnings disappointments were a common theme for all of the online retail companies as they each fell double digits on their earnings release. There has been a large deceleration in post-pandemic sales growth compounded by higher costs. These companies thrived during the pandemic, sending their valuations to extremely high levels. There was weak guidance across the board, as these companies continue trading near 52-week lows. Etsy guided for Q2 revenue of $565 million versus the $630 million consensus and fell -15%. eBay guided for Q2 revenue of $2.35 billion versus a $2.54 billion expectation. Shares of eBay fell over -10%. This is after Amazon guided for $118 billion in revenue for the second quarter, $7 billion below expectations.

We expect volatility to remain high as the high rate of inflation, the Russia-Ukraine war, and rising interest rates continue to weigh on the market. In our portfolios, we remain positioned defensively. Within our equity allocation, we continue to hold sleeves of dividend and low volatility ETFs. Year to date, our dividend ETF (SCHD) allocation has fallen -5%, outperforming the -14% drop for the S&P. This ETF has a higher weight to financials and healthcare and provides exposure to value stocks, while the exposure to growth is quite limited. Our allocation to the low volatility ETF is the iShares Min Vol ETF (USMV). The purpose of this ETF is its exposure to stocks with low beta. These large cap stocks are less correlated to the movement of the indices and provide downside protection in periods of high volatility. This ETF is down about -10% for the year. In our Core Series models, these ETFs account for over one-third of our large cap exposure. We plan to make shifts to growth as soon as we see inflation numbers start to level, as we believe the market has already priced in the expected rate hikes for this year and see the 25% correction on the Nasdaq as a buying opportunity in small increments.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2022 Winthrop Capital Management