A New Year, A New Problem

On the surface, the US economy looks fairly strong. Third quarter Gross Domestic Product (GDP) increased 3.2% according to the BEA and consumer confidence increased sharply in December according to the Conference Board. In addition, the employment market remains extremely tight as employers added 4.5 million jobs in 2022, the second-best year of job creation after 2021, and the unemployment rate is running at 3.5% in December. The manufacturing sector also is showing strength with supply chains no longer a barrier, and a mild winter thus far, easing pressure on energy demand.

However, when we look beneath the surface, the picture turns more gloomy. There are a series of compounding factors that are accumulating to cloud our forecast for the coming year. First, we know that historically employment is a lagging indicator that typically peaks at the inflection point of economic activity. With increased pressure on corporate profit margins, we expect to see some deterioration in employment in 2023.

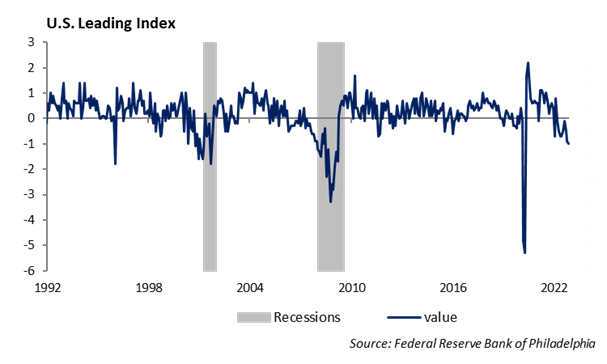

The inversion in the yield curve is often mocked for predicting 13 of the last 10 recessions; however, we are choosing to give it credence leading into 2023. We believe the current inversion of the yield curve is a leading indicator of a pending recession. Whether measured by the 3-month, 1-year, or 2-year US Treasury rate, the yield curve has inverted, which has an over 80% success rate of implicating an eminent recession. Further, the monthly Conference Board US Leading Indicator Index has declined for 9 months in a row. On average the index declines by only 3 months in a row prior to the US economy slipping into recession.

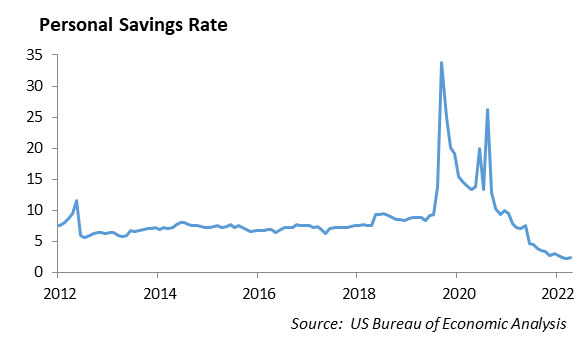

Finally, US personal savings rate, which has averaged over 6% the past 15 years, has slipped to 2.4%. The US savings rate received a boost over the past two years as a result of government support during the pandemic, and the last time the savings rate was this low was just prior to the 2007-2008 financial crisis.

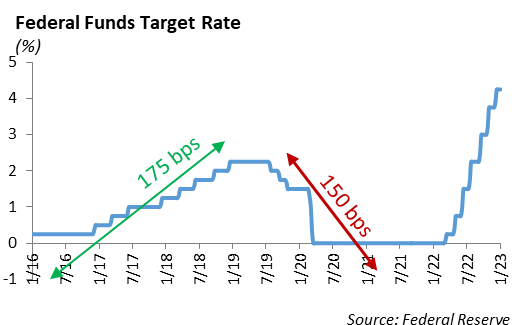

Tighter monetary policy will also combine to slow economic growth in 2023. The Federal Reserve’s monetary policy was the singular story driving capital markets in 2022. Labelling it “transitory”, the Fed was slow to recognize the growing rate of inflation in 2021 resulting from sustained low interest rates, the rapid growth in money supply, and supply chain disruptions. However, in 2022 the highest rate of inflation in the US since the 1970s was met with an aggressive shift in monetary policy. The Fed increased the short term interest rate seven times through the year from a level near zero to a target yield of 4.50%, the highest level for the overnight borrowing rate in 15 years.

The Fed has indicated a continued diligent aggressive push to higher short term interest rates. We expect their estimated terminal rate is 5.1%, while the capital markets are implying that after reaching 4.75% the Fed will begin reducing rates. We would be careful with this premise and expect the Fed to pause and hold rates steady for a sustained period. The time old testament of don’t fight the Fed was challenged over and over in 2022 as investors tried to front run the Fed and bet against the potential Fed shift in policy only to be wrong.

While we expect inflation will likely decelerate below 4% quickly, it will also take aggressive policy to reach 2% inflation target once again. This will likely lead the Fed to, at a minimum, maintain the current range of Fed funds rates for longer. An extended period of tighter monetary policy will likely cause a further credit contraction and lower global liquidity.

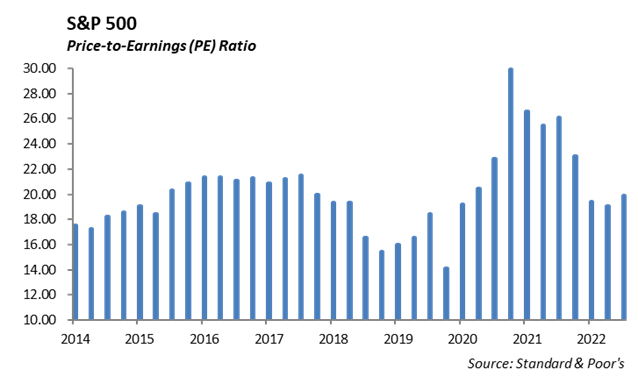

We believe this will lead to a dramatic slowdown in economic growth which is not fully priced into the capital markets. The current Fed policy has one objective, demand destruction. The bond market seems to understand that this is occurring. Slower long term economic growth will result in lower long term interest rates. Equity markets are misreading the decline in long term interest rates as a sign that the Fed is likely to pivot. The reality is that equity valuations have only returned to a historically normal levels. We believe interest rates will continue to decline out the yield curve. As a result, we like current bond valuations, but until we see a full reset of valuation in stocks to make them relatively cheap, returns will be challenging in equities.

This report is published solely for informational purposes and is not to be construed as specific tax, legal, or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2023 Winthrop Capital Management