“It turns out many of today’s problems are the result of yesterday’s solutions.” –Thomas Sowell

Easy come, easy go seems to describe the market sentiment over the past two years. After the past several years where larger than normal returns came easy for most investor’s portfolios, 2022 humbled even the most seasoned investor. For the year, the S&P 500 was down over -18% and Bloomberg Aggregate Index down -13% through the year, but this minimizes the declines in some sector and securities. Many stocks, particularly in the technology sector such as Zoom, Shopify, PayPal, and Amazon, were down over -50% during the year.

There are many lessons for investors from 2022, one of which is that valuation matters. However, now we must shift to what do we do in our portfolio from here. Over time, markets can move to excesses in valuation ranging from bullish optimism to extreme pessimism. In the end, markets are an unbiased tool for the pricing of risk. We are focused the on pricing of risk in markets and the valuation of securities over the coming year.

As we navigate the next move by the Federal Reserve, the domestic and geo-political environment and the shifts in economic activity, we have summarized our major investment themes, which we believe will impact both valuation and volatility of assets in 2023.

Stressed Consumer will Contribute to a Slowdown in Domestic Economic Activity

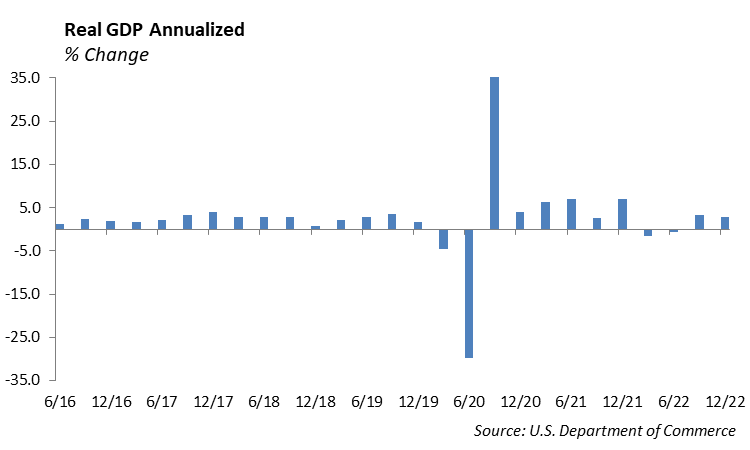

The Fed’s aggressive shift to increase short term interest rates, combined with slower economic growth in Europe, and a dysfunctional trade policy with China, is resulting in slower domestic economic growth. According to the BEA, Real gross domestic product (GDP) increased at an annual rate of 2.9% in the fourth quarter of 2022, which is lower than the 3.2% increase in the third quarter.

Representing nearly 70% of Gross Domestic Product, the US economy is fueled by the consumer sector, and is beginning to show signs of stress. If we see a sharp reduction in consumer spending, we expect a recession is likely as a result.

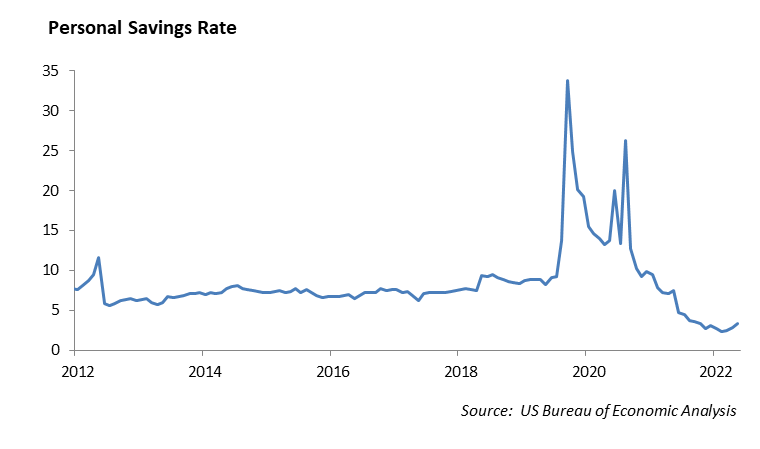

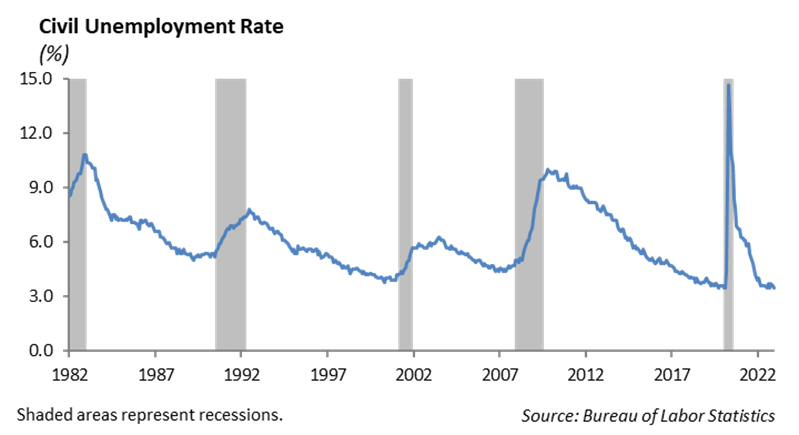

Stimulus checks, working from home, low interest rates, and lower expenses led to a short-term golden era for working Americans during the pandemic. Following the 2020-2021 period, spending increased, despite tight supply chains, and the net effect was a rapid increase in the rate of inflation. Now we are left with the hangover. Consumer savings has dropped from 6.0% during the pandemic to a paltry 2.1%, a historically low amount. At the same time consumer credit increased 8% in 2022 and 30+ day delinquency rates increased 15%. With more job openings than people seeking employment and the rate of unemployment at 3.4%, the labor market is still considered tight. But history has shown that employment generally peaks as we enter a recession and is a lagging indicator in the economic cycle. With savings tapped and credit card debt increasing, the consumer seems to have fewer levers left to pull to prop up spending and, if the employment market begins to roll over, we could see a rapid decline in consumer spending.

The Reopening of China’s Economy

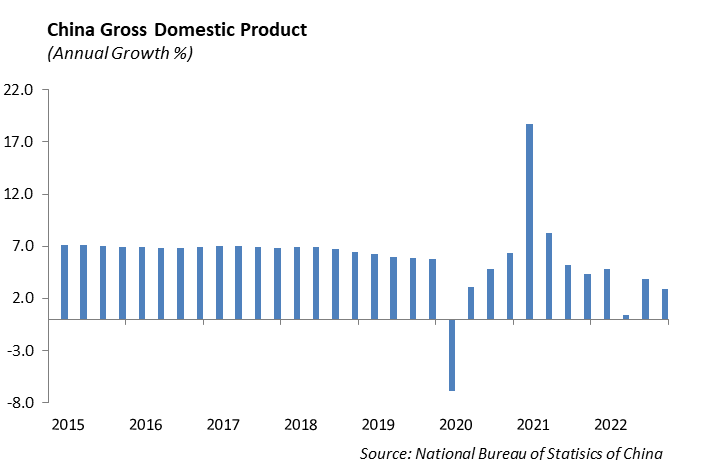

Following Covid lockdowns in China last year which dampened economic growth, we expect China’s growth rate to exceed 5.2% this year. The government has shifted to providing more stimulus to the economy; however, growth is challenged by a shrinking population and decline in productivity. The structure of China’s economy has shifted to larger state-owned companies, which are playing an increasingly important role.

China has been one of the most challenging places to invest over the past 3 years, and it is always dangerous to look at any foreign investment, particularly China, through the distorted lens of western capitalism. While relative valuations have been better than many countries outside of the US, the political and regulatory environment has muted valuations and potential growth. A strict Covid-Zero policy shut down critical cities for weeks at a time which totally impaired economic activity. The Chinese Communist Party also clamped down on Hong Kong, its pro-democracy movement, and the large profitable tech companies that seemingly became more powerful and vocal than the government was comfortable.

However, 2023 has proven to be an inflection point for the Chinese stocks. The communist party has backed off its crack-down on the corporate sector and, in some cases has taken golden share stakes in large tech giants including Alibaba and Tencent, which gives the communist party the input into the business they require. While China has challenges to navigate in its shifting technology and trade policy, we believe the communist party is intent on returning to higher rate of growth in 2023 and will create policy initiatives to achieve this goal. Outside of the US we believe China could be the best investment opportunity of the next 10 years.

Declining Rate of Inflation Through First Half of the Year

The direction of monetary policy of the Federal Reserve will be a major factor driving asset valuations this year. The key driver to Fed policy this year will be the direction and pace of inflation. The domestic rate of Inflation, measured by the Consumer Price Index (CPI), hit a 30 year high of 9.1% in June 2022 despite the Fed’s persistent narrative throughout much of the prior year that inflation was “transitory.” The Fed’s shift toward an abrupt tightening in monetary policy grew more aggressive through the past year in an effort to create a decline in consumer demand despite tight supply chain issues and a tight employment market. Estimates for year-end CPI are currently near 3.9% and we believe inflation will fall below 4% by 3Q 2023. For the first half of 2023, we expect a deterioration in the health of the consumer sector. An increase in corporate layoffs is already eroding the strength in employment as the consumer savings rate declines sharply and credit card debt increases. In addition, higher interest rates on auto loans and home mortgages are acting to slow economic growth.

Related to Fed monetary policy over the next year, we believe there are two major risks which may impact asset prices. First, an overly aggressive monetary tightening from the Fed could ultimately lead to a disinflationary environment much like Japan has lived in for over a decade. Second, if we experience a rebound in the rate of inflation as a result of the reopening of China and higher demand for energy and raw materials, we could experience stagflation if domestic economic growth continues to slow.

A Strong Labor Market will be Key to Economic Growth

During the pandemic, parts of the economy, including restaurants, hospitality, and entertainment, literally shut down. At its peak in April of 2020, 23.1 million people were out of work, and the rate of unemployment hit a record 14.7%. Today, in spite of recent layoffs in the technology sector, the unemployment rate has declined to 3.4%. The challenge is that a large number of workers have removed themselves from the labor pool and are no longer looking for work. The labor force participation rate is near a dismal 61.8 percent, down from 63.2 percent in October of 2019. The labor market is the key to sustained economic growth.

The acceleration in the growth in wages this past year will put additional pressure on hiring and operating margins, which in turn will act to slow job growth.

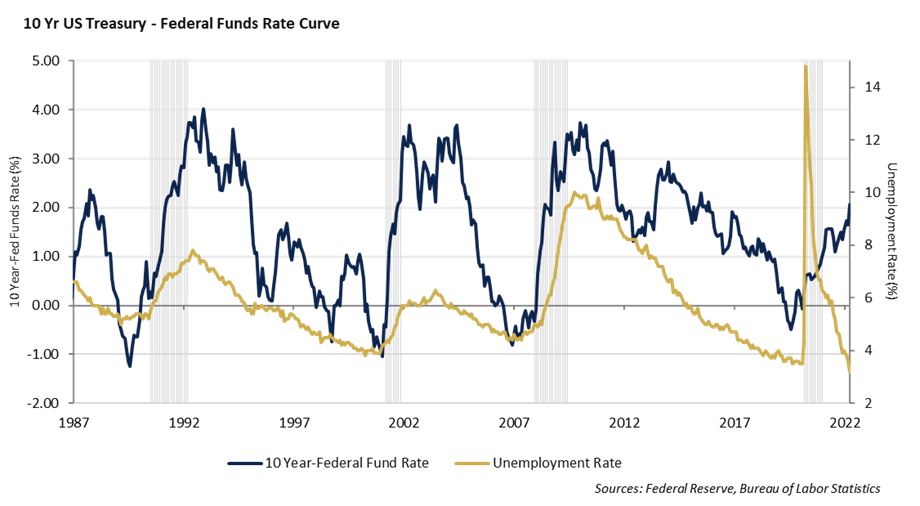

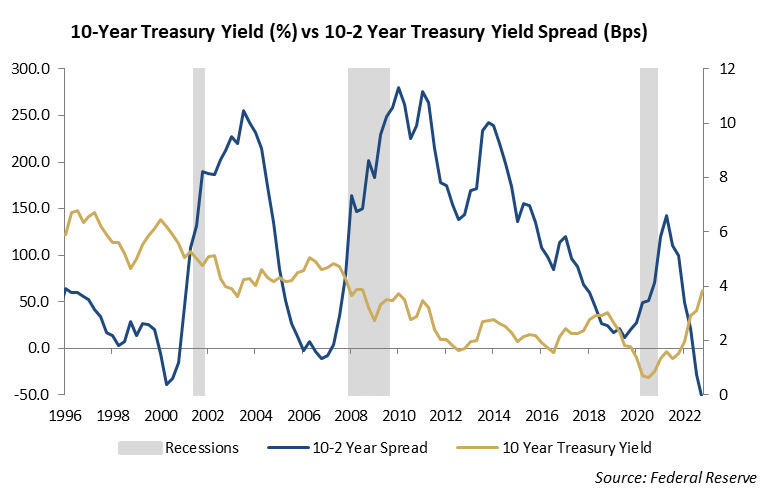

Yield Curve will Remain Inverted

As inflation subsides this year, we expect monetary policy to stabilize, and the bond market will become less reactive to the Fed’s next anticipated move. Lower volatility combined with lower interest rates will create investment opportunities across the fixed income markets. We expect the yield curve to remain inverted through the first half of the year until slowing economic growth and lower rate of inflation provides cover for the Fed to lower short-term rates.

Currently, 5-year BBB corporate bonds are yielding above 5% and similar maturity high yield BB rated corporate bonds are yielding near 6.50%. With interest rates higher relative to the past 10 years, and spreads wide, we see more buying opportunities in bonds. Higher expected returns in fixed income sectors favor increased allocation to bonds in 2023.

Expect Marginal Deterioration in Credit Quality

After many years of low interest rates and an increase in leverage, expectations for slower economic growth results in an increase in reserves for bad loans. Government assistance during the pandemic provided support to consumers and businesses which effectively masked financial problems for some companies and extended the length of this credit cycle. We would expect an increase in the number of troubled loans and reserves for loan losses in 2023.

While every tightening cycle results in a shift in the demand curve, not every tightening cycle results in a meaningful reduction of leverage in the system. While the cost of capital increases with the rise in interest rates, we do not expect a wave of distressed selling of assets due to a forced reduction in leverage.

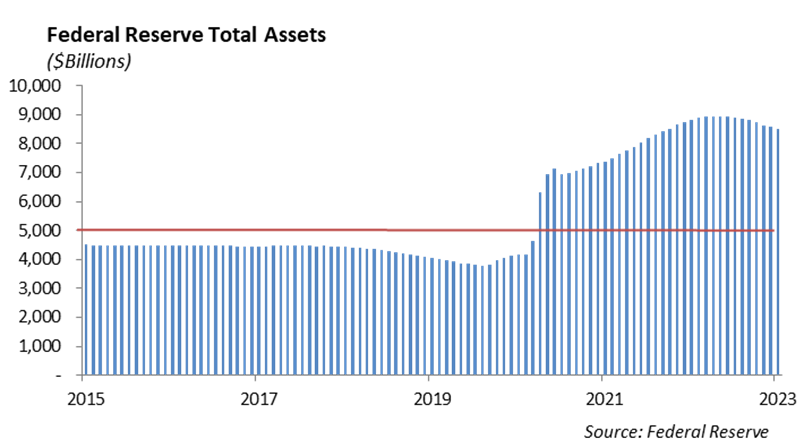

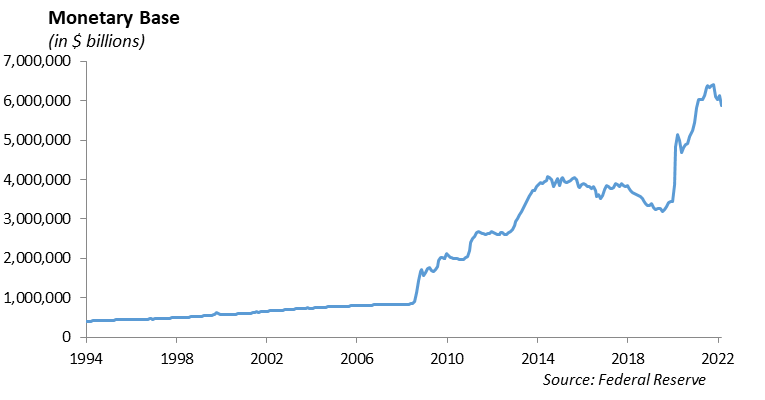

During the pandemic, assets on the Fed balance sheet doubled in size, ballooning to nearly $9 trillion. This created significant market liquidity and provided fuel for the appreciation in prices of risk assets. However, in an abrupt shift this year, the Fed sucked half a trillion dollars of liquidity out of the system, which resulted in a broad dislocation of prices of risk assets. The M2 Money Supply Index fell -15% in 2022 and the velocity of M2 remained at historically low levels.

Lower Expected Returns for Risk Assets

Over the three-year period of 2019-2022, domestic equities returned an average annualized rate of 22%. This is an impressive rate of return considering that, during much of that time, parts of the economy were effectively shut down due to the pandemic, and our trade policy with China resembled a broken plate on the kitchen floor. Equity valuations were stretched to extreme levels, and the flood of liquidity allowed companies operating with little or no profits to continue to exist, resulting in a dangerous increase in the number of “Zombie Companies” in the market.

Last year, investors were forced to incorporate a number of shifting variables including the risk of rising inflation, a tightening monetary policy, and a slowing economy into their valuation models. We believe 2023 will be a year of pricing in the risk of an earnings recession. We expect revenue growth will be challenged as the consumer has less buying power and the decline in the rate of inflation results in downward pressure on prices. In addition, operating margins will continue to tighten as a result of increased labor costs and higher interest expense.

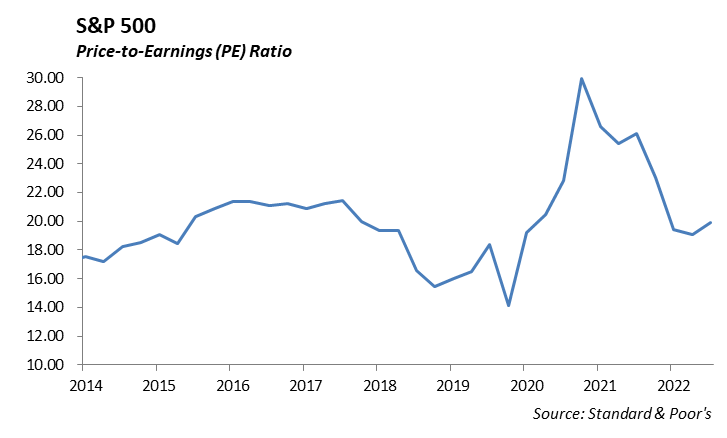

While the S&P 500 declined -19.6% for 2022, equity valuations did not adjust significantly lower with the market decline. The S&P 500 is currently trading at over 19x earnings, and, while this is considerably lower than the over 30x it was trading at in 2021, is still above the market average of 16.5x. If earnings are challenged as we expect in 2023, then heightened valuations will still be a headwind for stocks. We believe this will lead to lower expected returns over the next few years until the US economy can find its footing and return to a more stable growth environment.

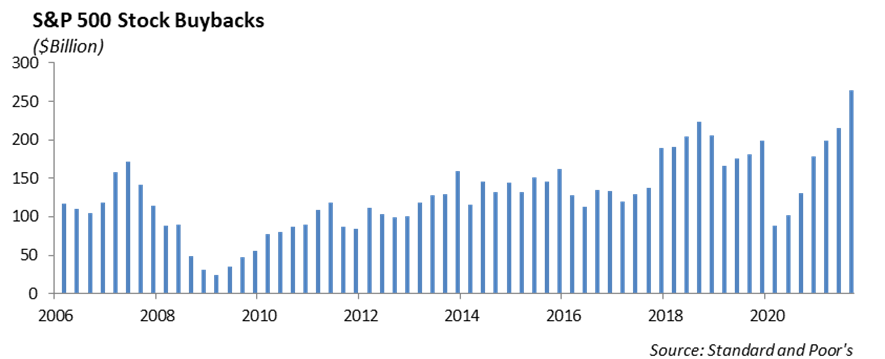

The next year will be marked by weaker corporate earnings and cashflow. The decline in stock prices will provide incentive for companies to increase stock buyback programs. We have already seen announcements from Meta, HCA, UPS, and Chevron with significant increases to their stock repurchase programs.

Deterioration in Fundamentals Supporting Commercial Real Estate

Over the past decade, investments in commercial real estate have performed well as sustained low interest rates provided support for increased valuations. Last year, based on revenue, the commercial real estate market was estimated to be over $1.2 trillion according to IBISWorld. However, after navigating major shifts through the pandemic years, the global real estate market faces challenges as companies evaluate the amount of space they need for employees and how buildings will be used. In addition, the sharp rise in home prices has forced an increase demand for apartments as first-time home buyers are priced out of the market. With the potential for a regional or global recession, valuations of commercial real estate will be under pressure.

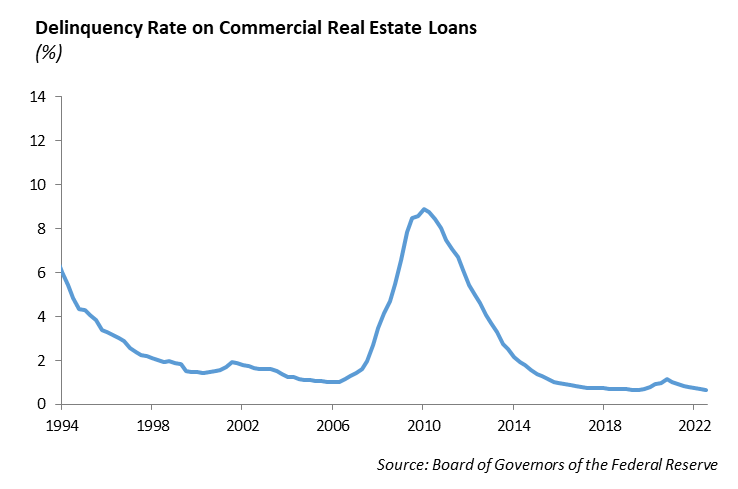

We expect both the office and retail sectors will be challenged this year. The pandemic has forced many companies to adopt a more flexible work environment. The result is that, for many employers, working remote has become normal; yet companies are sitting on large amounts of underutilized office space. While companies have been willing to cover the expense of this unused office space for the past 18 months, we do not expect that to continue this next year. We expect to see companies limit excess office space and reduce rent expense to offset increasing labor costs. As a result, the commercial real estate market may see shifts in valuations next year as rent rolls decline and cap rates remain elevated. Because of the relief under the Cares Act, the delinquency rate has not increased compared to the period of 1991 and 2008. This is masking the potential deterioration in the commercial real estate market. Any deterioration in commercial real estate will have a negative impact on valuations in the REIT and Collateralized Mortgage-Backed Securities markets.

Lower Long Term Interest Rates will lead to a Sector Rotation in Equity Performance

In 2022, higher interest rates contributed to the negative performance in technology, communications services, and consumer discretionary stocks. The sectors that have performed the best in the previous few years suffered immense declines. The technology heavy Nasdaq index fell -33% for 2022. Meanwhile, the energy sector rebounded over 50% last year and defensive sectors in general outperformed the broad market. Value stocks outperformed growth stocks by over 20% for the year.

This shift in sector and valuations was the result of several factors including the abrupt change in the Fed’s monetary policy resulting in higher interest rates. The result is weaker economic fundamentals and a decline in corporate earnings.

However, we expect the Federal Reserve to pause its aggressive push in short term interest rates in 2023 sooner than expected. The capitulation by the Fed in its monetary policy could mark a pivot for interest rates and provide a catalyst for stock prices in the growth sectors that were beaten down last year. A decline in interest rates will support a rotation back to growth stocks. Although we do not expect a large recovery in stock prices in the S&P 500 in 2023, valuations in large cap high quality growth stocks provide a good opportunity at currently levels. Similarly, defensive sectors such as Utilities and Staples, have reached stretched valuations and performance in these sectors may struggle to keep pace with the broad market.

Increase in the Growth of Cybersecurity/Connectivity Companies

While we are constructive on technology stocks, there are sub-sectors within technology that have attractive valuations including cybersecurity. The growing threat of cyber attacks and ransom has forced companies and the government to invest heavily in cybersecurity infrastructure. We expect double digit revenue growth for the foreseeable future for companies operating in the cloud security, data security, and identity access management segments. As data becomes more accessible through the internet, cyber-criminals have more possibilities to attack users. There have been many high-profile computer hacks over the last few years including Visa, Target, Home Depot, JP Morgan, and Equifax. As cybersecurity threats become more sophisticated, companies with weaker cyber protection systems will need to upgrade their cyber infrastructure. As a result, companies are spending more on cybersecurity software, as the cost of a computer breach increases. The global cybersecurity market has grown in size is currently valued at close to $200 billion. This will be an important industry in the coming decade with continued access to the internet and digitization of data.

Consolidation in the Media Streaming Industry

For many industries, the pandemic accelerated shifts in certain industries and business models that were already in motion. One of those shifts has been in the growth in streaming companies like Netflix and away from traditional cable. The shift to an increased consumption of streaming services that was no longer reliant on network programming, movie theaters or cable bundles accelerated during the pandemic. This also led to an increase in the amount of content providers, reducing the reliance on traditional network programing. With streaming services including Showtime, Disney+, Peacock, Amazon Prime, Discovery+, Apple TV, HBO, the market has become extremely fragmented. Production costs for content creation increased and sheer quantity of content produced accelerated.

Investors are expecting profitability and not just focused on increases in subscriber growth. With the potential for slower economic growth and reduced consumer spending, this year will likely challenge profitability of streaming companies as the consumer rationalizes paying for multiple streaming services. We believe 2023 will be a year marked by consolidation in streaming services and a renewed focus on producing high quality content. There are only so many eyeball hours in the day, and it seems that the industry has already found its saturation point.

DISCLAIMER

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2023 Winthrop Capital Management