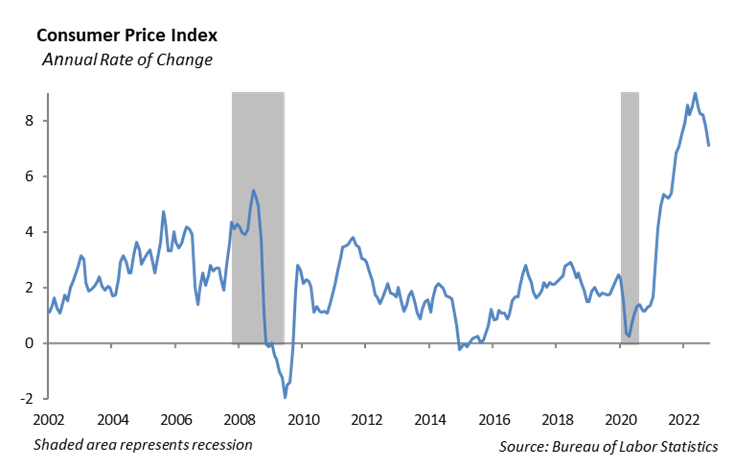

Inflation

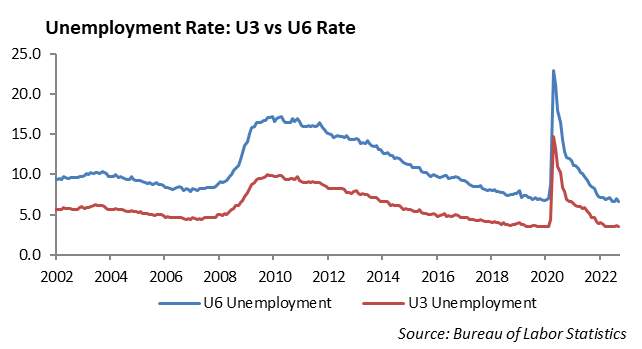

Underlying price pressures continue to build in most major developed economies despite the recent decline in domestic headline inflation. This indicates that global central banks will have to keep tightening monetary policy, albeit at a more moderate pace, in the coming months in order to shift demand and slow the pace of inflation. We expect further tightening will impact the labor market, resulting in increased lay-offs and deterioration in the unemployment rate, which currently rests at a healthy 3.7% in the U.S.

Core inflation, measured by Consumer Price Index, excluding changes in food and energy prices, is accelerating in many parts of the world. The November CPI release by the U.S. Bureau of Labor Statistics indicated that the CPI all items index increased 7.1% for the 12 months ending November, its smallest annual increase this year. The all items less food and energy index rose 6.0% over the last 12 months. In November 2022, the core inflation rate in the United Kingdom was 6.3%, compared with 6.5% previous month and European Union Core Inflation Rate is at 7.8%, compared to 7.6% last month.

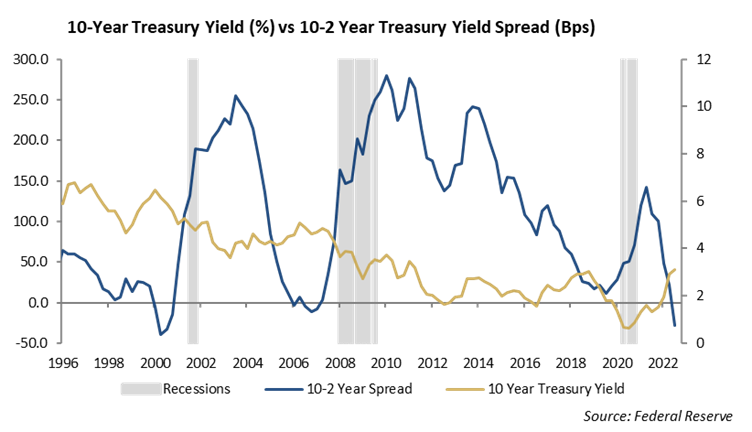

Yield Curve Inversion Steepens

Heading into the end of the year, the yield curve continues to steepen as an increase in expectations for slower economic growth pushes yields on long dated US Treasuries lower while the Fed increases short term interest rates. The yield curve inversion is matched by periods in 2000 and 2006 which were both followed by recessions within 18 months.

The difference today is the rate of unemployment, measured by the Labor Department U3, which is running near 3.7%. Back in 2000 and 2006 unemployment was marginally higher at 4.0% and 4.7%, respectively. Periods following a sustained inversion in the yield curve resulted in slower economic growth and an increase in the rate of unemployment. We expect the same for this tightening cycle.

This report is published solely for informational purposes and is not to be construed as specific tax, legal, or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2022 Winthrop Capital Management