Fed Policy is the Key Driver to Valuations

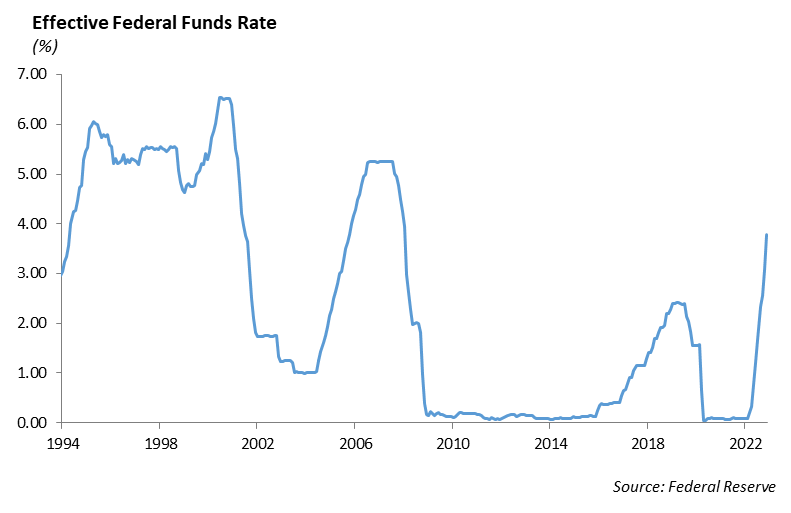

The sustained elevated pace of inflation is the focus of the global capital markets. Inflation, measured by the CPI, is running at a 7.7% annual rate in November which is lower than the 9.1% in June. The response from the Fed has been to increase short term interest rates by over 300 bps so far this year. The increase in short term interest rates has raised the borrowing costs and slowed demand. Given the persistent strength of global inflation, we now expect the Fed to push rates high enough to choke economic growth.

Higher interest rates are flowing through the capital markets and impacting corporate earnings, mortgage loans, and existing adjustable rate leveraged loans. Corporate earnings are negatively impacted by rising wages and increased interest expense. Companies are being forced to rationalize paying rent on office space that is still not fully utilized following the pandemic. In the face of slowing revenue growth, in order to preserve profit margins, companies will begin to reduce leverage, headcount, and rent expense.

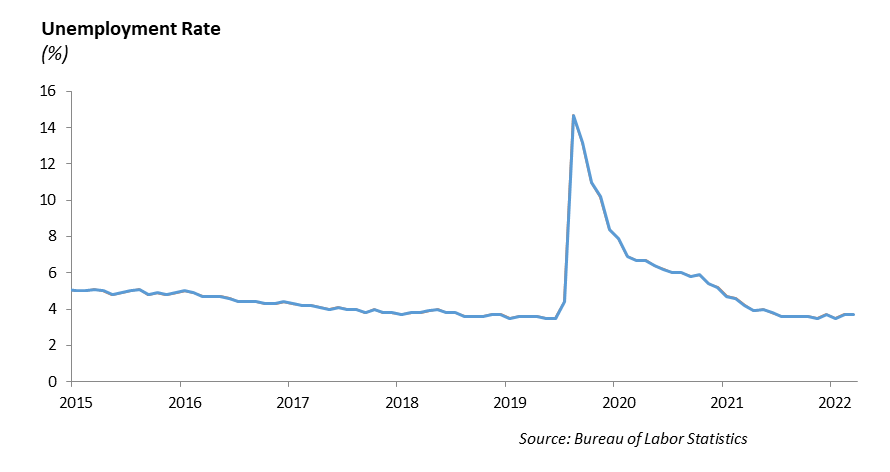

The labor market remains very strong. According to the Bureau of Labor Statistics, the November unemployment rate was 3.7%, which is near a 50-year low level of unemployment. While there are currently 6.1 million unemployed people, there are over 10 million job openings. The key to the sustainable economic growth is the health of the labor market. In November, 263,000 jobs were added to the market, and the labor force participation rate didn’t change much at 62.2%.

The Fed has increased short term rates by 300 bps this year. However, we expect the Fed to begin to slow the pace of rate increases. In the absence of a dramatic decline in the rate of inflation, at the current pace of inflation, we expect the Fed will have to push short term rates up to 4.5%.

This report is published solely for informational purposes and is not to be construed as specific tax, legal, or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2022 Winthrop Capital Management