The Capital Markets – Is there a Bubble?

A bubble in financial assets is a situation in the capital markets in which asset prices appear to be based on implausible or inconsistent assumptions or expectations. It is indicative of an asset trading in excess of its intrinsic value and is often fueled by a lack of price transparency. It is very difficult to recognize a bubble when we are in it. It isn’t until after the bubble bursts, that we often see the telltale signs of excessive prices.

While valuations are near the higher end of the historic range, we do not believe we are currently in a bubble in the U.S. equity market. For this reason, we do not believe we are in a bubble in the equity ETF market.

Furthermore, we do not believe we are currently in a bubble in the publicly traded corporate bond market. There is significant demand for investment grade and high yield credit which continues to absorb new issue supply and makes secondary trading challenging. For this reason, we do not believe we are in a bubble in the fixed income ETF market either. However, we are concerned about liquidity in the bond market in periods of heavy redemptions. This is a structural issue and not related to excessive valuations.

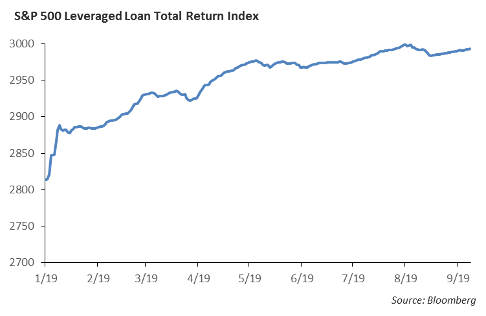

The two areas of concern are leveraged loans and commercial real estate. The leveraged loan market has grown to over $1 trillion in size and is larger than the high yield market. The largest vehicle for leveraged loans is the collateralized debt obligation (CDO) which is illiquid and lacks price transparency.

Commercial real estate has posted strong returns for investors over the past ten years. Fueled by low interest rates, the commercial mortgage loan market is the primary funding source for commercial real estate. Again, the lack of liquidity and price transparency makes commercial real estate vulnerable in an ultra-low interest rate environment.

Monetary Policy

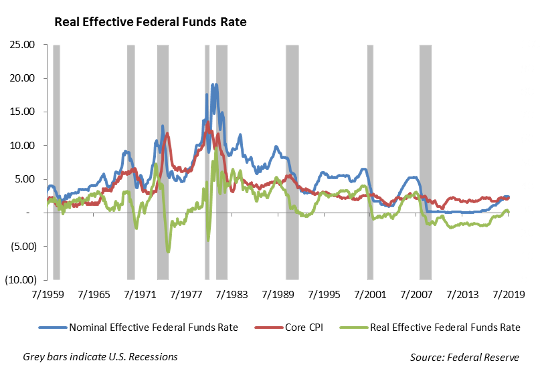

We expect the Federal Reserve will lower interest rates 25 basis points at its next meeting. In spite of weaker global economic growth, the U.S. economy is still growing, albeit at a slower pace than last year. A primary catalyst to the increasing prices of financial assets has been Fed shift from a policy of tightening in the fourth quarter of 2018 to today’s easing policy.

Adjusted for inflation, the real Fed Funds rate is zero. There has never been an instance when the economy has moved into a recession with the real Fed Funds rate at or below zero.

Equities

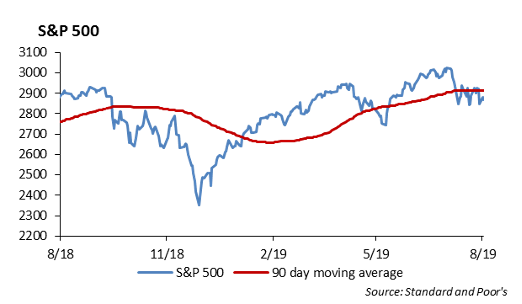

The S&P gained 1.8% during the shortened trading week, and the index currently up 18% YTD and less than 2% from all-time highs. Most of the gains came from news that the United States and China had agreed to meet in Washington next month for another round of trade negotiations. We have seen the S&P stuck in a trading range for about 3 weeks now with support at 2825 and resistance at 2940. This week, there was a break out of the trading range, with the index ending the week at (2978), and up above its 200 day moving average.

With the continuous rise in the index combined with earnings deterioration, we have been in risk off mode. We have been slowly shifting some of our large cap exposure into the low volatility ETFs. Specifically, we have added to the IShares Min Vol Fund, which is a sector neutral ETF that maintains index sector weights, with low volatility stocks in each sector. We prefer this ETF as it maintains exposure to all sectors, rather than an ETF full of REITs and Utilities. Both our Tactical Series and our Core Series have shifted toward a higher exposure in low volatility.

Additionally, in our large cap blend strategy, we have been shifting towards defensive sectors. We are overweight Consumer Staples and are looking at names such as Pepsi and Dollar General, as they have continued to navigate tariff headwinds effectively with continuously strong top and bottom line numbers. Additionally, we continue to like both Walmart and Costco as our top positions within that sector.

A couple of quick stock notes from the week:

- Facebook: Fell 2% after New York general attorney announced it would be investigating the company for antitrust violations

- Costco: Rose 2% on August same-store sales increase of 5.5%.

- Lululemon: Jumped 7% after earnings results, with growth in men’s sales.

- Grubhub: Up 2% on delivery partnership with McDonald’s

- AT&T: Up 9% after activist Elliott Management takes a $3.2 Billion stake, believing the company could eventually be worth $60/share.

- Eli Lilly: Up 3% this morning after their lung cancer drug shrank tumors in almost 70% of advanced lung cancer patients.

In IPO news, the market is picking up again with 6 new deals expected to raise $2.2 Billion in the week ahead. 3 companies are targeting IPO valuations of $3.5 billion of more, the biggest being SmileDirect Club and CloudFlare. The Renaissance IPO Index is up 34.4% YTD with top holdings Roku and Spotify.

Europe – Boris Johnson’s Brexit Chess Game

In his effort to move Great Britain out of the European Union, Prime Minister Boris Johnson has made his move, and now, the British Parliament has blocked Johnson’s queen.

Last week, after Johnson sought permission from Queen Elizabeth II to suspend Parliament for a month in order to reduce the political brinksmanship, Parliament blocked Johnson’s move. Now, any Brexit initiative is forced to go through Parliament and the deadline has been extended to January of 2020, effectively reducing Johnson’s negotiating position with the EU. In his next move, the Prime Minister sacked 21 members of parliament (MPs) from his party who were disloyal to his Brexit agenda, and he has called for a snap election. With fewer chess pieces on the board, including his brother, the Prime Minister indicated that he would not comply with the directive for a Brexit delay saying that he “would rather be dead in a ditch than ask for a delay.”

Largely effected by Brexit and China trade issues, the European economy has been slowing over the past year in tandem with the global slow down. As a result, European equities have lagged U.S. stocks on a year-to-date basis. However, the gap is beginning to narrow. While the S&P 500 has increased 18.65% year to date, the DAX is up 15.23%. The London FTSE is increased a mere 8.14% over the same time.

We are beginning to increase International developed country exposure in our Portfolio Models heading into the fourth quarter. There are several reasons for our change in bias. First, negative interest rates throughout Europe should help to spur growth. We expect that Germany, which has been running a budget surplus, will take steps to loosen its purse strings and provide fiscal stimulus to help combat its slowing economy. In addition, we expect the European Central Bank to reignite its bond purchase program this week. Finally, we believe that we are closer to a resolution on both China trade and Brexit, which will serve as catalysts for business investment.

Fixed Income

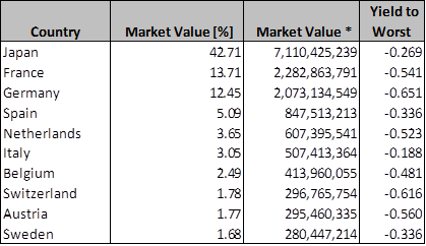

Rates generally rose during the week as investors moved back towards the risk on trade in hopes that a deal with China could happen sooner rather than later. While the trade war has taken up much of the media’s content, we continue to get questions about negative interest rates across the globe and whether they really matter. Measured by market value, Japan, France and Germany make up the largest portion of negative yielding debt. While negative yielding debt should spark borrowing and investment, the significant problem is that the banking sector cannot effectively operate in this environment. We fear that a prolonged period of negative rates will challenge the viability of the banking sector going forward.

Corporate credit was a singular story over the past week as the entire market was focused on the largest new issuance ever in one week at $73bn. The amount issued during the short week almost matched the entire $75bn issuance of August. Despite the heavy issuance and slow secondary market, spreads did tighten over the week due to rising interest rates. Our defensive tone remains constant and we are using market rallies to take risk out of our portfolios. We see signs that we are in the late stages of this credit cycle, meaning that it is time to focus on capital preservation and not reach for returns.

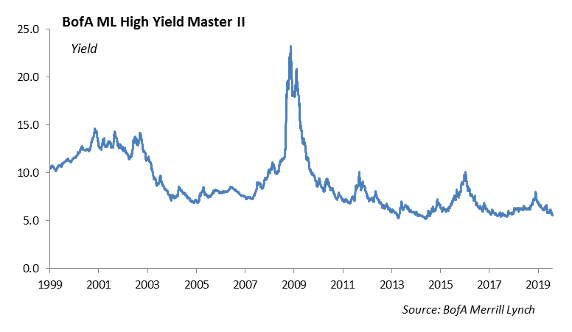

High Yield

Much like the equity markets, high credit performed on the back of positive news on the China trade front. The index tightened 3 basis points to an option adjusted spread of 405 basis points net of rebalancing. For total return, U.S. high yield credit delivered 25 bps last week. Bs were the outperformer for the second week in a row returning 30 basis points, and BBs were not far behind with 26 basis points of total return. CCCs continue to be the laggard, but returned a positive 5 basis points. BBs are still the best performer year-to-date, especially when considering risk adjusted returns. The risk tier has seen over 13% total return in 2019.

High yield fund flows were negative this week with an outflow of $318 million. This is the first outflow in three weeks after $2.2 billion of inflows in the weeks prior.

New issues came nowhere near the record breaking activity we saw in their investment grade counterparts, but we did see activity pick back up from its two-week hiatus. $3.8 billion priced last week on six deals. This is tracking a bit below the volume expectations of $25 billion this September and last year’s September activity of $22 billion pricing this month. 5 out of the 6 deals that priced were BB issuers, which we see as high yield issuers finally taking advantage of this environment to lower interest expensive and improve credit profiles. The high yield primary market was well received all week and priced at the low end of initial price talk.

Despite recent outperformance from single B issuers, we still favor allocating the majority of high yield resources to BB credits. We remain wary to invest in maturities trading with negative yields as we are finally seeing refinancing activity in high yield. Duration is the main question here as significant tradeoffs even between 2-year and 5-year maturities are present. There appears to still be a fairly decent yield value even out five years, but we believe much of the risk may be priced in with a looming cyclical downturn before then. Short duration BB credits are trading very tight, and it is difficult to get just 2.5% for a well-respected 2-year issue. We recommend approaching this space on a name by name basis and investing to both duration groups. For longer dated high yield debt, we believe new issue is the most reasonable entry point into the market.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.