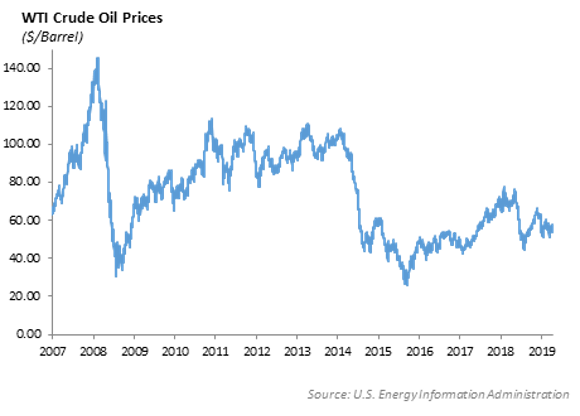

The Drone Attack on Saudi Arabia

On Saturday, a hostile drone strike hit the Khurais oil field and Abqaiq, a vital crude processing center in Saudi Arabia. While the U.S. has blamed Iran for the drone attacks, Iran-backed Houthi rebels in Yemen claimed responsibility. The U.S. says there is no evidence of attacks emanating from Yemen, and if Iran is behind the attacks, then there is reason to believe that Russia is involved.

What does this mean for oil prices?

Saudi Arabia is the major OPEC producer. With over 10 million barrels a day in daily production, it accounts for approximately 10% of global oil production. The attacks hit one of the most important global oil production facilities, and early estimates indicate it will cut Saudi production in half with a decline in output of over 5 million barrels a day, taking out most of the slack in oil supply.

Over the near term we would expect a rise in oil prices; however, Saudi Arabia has reserves it can ship from, and OPEC members are expected to step in to meet quota. Expect gas prices to increase as well.

What does this mean for the global economy?

Oil price shocks resulting in dislocations in oil prices will likely have a short term impact on the economy; however, the long term impact should be de minimis. To the extent that the U.S. increases production, we expect that this will have a near term positive impact on the energy sector and domestic economy. To the extent that consumers see increases in gas prices, we expect that this will act as a head wind for consumption as increased gas prices chip into discretionary spending.

Saudi Arabia used to ship over 2 million barrels of oil a day to the United States. Today, that number is down to approximately 600,000 barrels a day. In contrast, the Saudi’s ship a significant amount of oil to China, but China will now be forced to find alternative sources. The U.S., now a major exporter of oil, has a tariff on exported oil, which could result in a potential incentive for a resolution in U.S.-China trade negotiations coming up in early October.

Monetary Policy

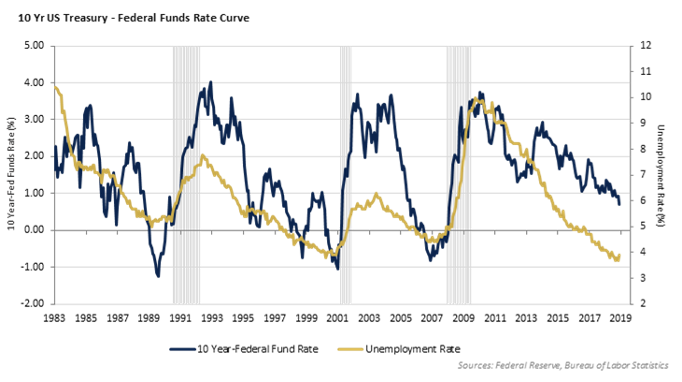

We expect the Federal Reserve will lower short term interest rates by 25 basis points this week at its September meeting. The move is in tandem with other central banks and sympathetic to global economic growth. With the shift in risk in the market, bond yields moved sharply higher last week with the 10 year U.S. Treasury hitting 1.9% on Friday, allowing the yield curve to steepen slightly.

The Fed takes some relief from a more dramatic easing of monetary policy by relying partially on the health of the labor market. In the fourth quarter, we expect to see a deterioration in the labor picture as businesses tighten up purse strings in the face of pressure on earnings.

Equities

The S&P was up about a percent over the last week, ending on Friday at 3007, up 20% YTD and less than 1% from all-time highs.

Last week, there was a shift out of momentum names into value names. The top 50 stocks in the S&P with highest YTD returns coming into Monday were down an average of 1.45% at the end of the week. Meanwhile, the 50 worst performing stocks in the S&P were up an average 3.37% by Friday. Growth stocks have outperformed value stocks for 13 years now. On a cumulative basis, the outperformance has been 140%, which is more than a 10% advantage every year. From a valuation standpoint, value stocks are trading at a 7% discount to their historical P/E levels, while growth stocks are at a 39% premium. We are hesitant to label it a trend, but YTD, momentum is still up 20%, while value is up 17%. It is also worth mentioning that the Russell 2000, which has underperformed large cap YTD, was up 5% over the last week, and is now posting a 17.50% return YTD.

A couple of headlines from companies to start the week:

- Streaming Services – The iPhone launch event last Tuesday revealed 3 new iPhones, ranging between $700-$1100. The biggest takeaway was the Nov.1 launch of Apple TV+, a streaming service for $4.99 a month, which undercuts both Netflix and Disney+ prices. On Saturday, the CEO of Disney, Bob Iger, announced his resignation from Apple’s board of directors in light of the competing service’s release.

- Energy Stocks – Exxon, Chevron and energy stocks in general are expected to rise between 3-4% following the huge spike in oil prices. Crude is up 9% to $65.49 a barrel after the attack on Saudi Arabia’s oil infrastructure knocked out 5.7 million barrels of daily crude production – equivalent to 50% of their oil output. Energy has been the worst performing sector YTD, returning only 5.50% YTD and lagging the S&P by 15%.

We are looking for a dip in the market at open. Look for airlines and cruise lines to trade lower (American, Delta, Southwest, Alaska, Royal Caribbean all down premarket), and energy and gasoline names to move higher (Marathon, Concho, Noble, Exxon, Chevron higher in premarket).

Europe – the ECB opens the Flood Gates for Liquidity

Last week, the European Central Bank (ECB) announced that it would lower short term interest rates and resurrect its controversial bond purchase program. The ECB is the central bank to Europe, but unlike the Fed, which governs monetary policy over a republic of states, the ECB is a cooperative organization governed by the countries it represents. As a result, monetary policy can be influenced by political overtones. Germany, which is very fiscally conservative, is against reinstituting the bond purchase program.

The ECB bond purchase program allows this co-op the ability to purchase the sovereign debt of member countries. As a result, the ECB is the natural buyer for the debt of Italy, Spain, France, and Germany, effectively subsidizing the interest rates in which they borrow. However, the challenge for the ECB, given its aggressive plans to purchase €20 billion per month of sovereign debt, is the logistics of buying bonds. The concern is that there are not enough eligible bonds for the ECB to buy which will inevitably result in the expansion of the program.

Fixed Income

Rates saw a sharp reversal to the upside this past week in front of a likely Fed rate cut. Investors began to move back into euphoria mode on the hopes that there will not be a hard Brexit, plus there seems to be a deal on the horizon with China, and jobs data is strong. 10-year and 30-year U.S. treasuries widened over 20bps with the 30-year ending the week at 2.37%.

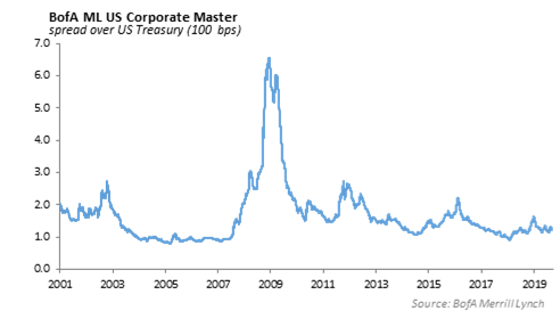

Corporate spreads began to tighten due to interest rates generally increasing through the week. Wall Street’s focus was once again on new issuance. Relatively low rates and flat curves has incentivized debt issuance and a refinancing of over $125bn in corporate debt over the past 2 weeks.

This past year has been a strong year for fixed income markets. Both investment grade and high yield indexes are up over 10% for the year, comparable to what is considered a good year for equity markets. After such a run in fixed income, and as we bounce off of historic lows in global interest rates, we are prepping our portfolios for compressed returns on the horizon. Historically tight spreads, matched with historically low rates, will inevitably result in lower returns, even if rates do not increase. While we see suppressed returns, we still believe fixed income will be a necessary portion of asset allocations as it remains a lower volatility, lower correlation alternative to equities.

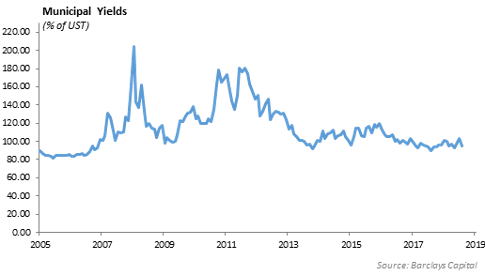

Municipal Bonds

Over the past 2 weeks, our thesis on municipal bonds has worked well. We’ve maintained belief that municipal bonds would be relatively cheap as 30-year bonds hit parity with U.S. treasuries. The yield ratio on 30-year muni’s now stands at 93% after outperforming. While a stopped clock is right twice a day, we continue to believe municipals will outperform U.S. treasuries throughout the rest of the year. Issuance in the sector continues to be short of maturing bonds, and demographic shifts will continue to lead to buying across the curve. 30-year AAA-rated municipal bonds are now yielding 2.35%, which translates to roughly 3.3% for top tax bracket investors.

High Yield

U.S. high yield credit tightened significantly last week on positive market sentiment. We saw 22 bps of tightening, which was also aided by the ECB’s approval of new stimulus package. We now sit 128 bps tight of year-end 2018 levels at an option-adjusted spread of 383 bps.

For total return, the high yield credit index saw 0.15% of performance with the riskier tiers outperforming relative quality. CCC’s returned just under a percent, B’s returned almost 40 bps, while BB’s were actually negative at -23 basis points of total return. This is a complete reversal from the total return we have seen over the past couple of weeks. We believe at least part of that negative performance from BBs was due to technicals on heavy new BB-rated supply. On a year-to-date basis, BBs are still the outperformer at 12.77% return vs. total U.S. high yield index return of 11.60%.

High Yield funds flow was a positive $1.86 billion, making this past week the largest inflow since June of this year.

The high yield new issue market had the biggest week of 2019, pricing $16 billion of new issuance. Year-to-date issuance now reaches nearly $185 billion, a 30% increase from this time last year. The week was heavily saturated in BB credits, with some lower rated issuers coming to market later in the week. Uber had its first debt offering since its IPO, issuing $1.2 billion in line with price talks. Altice France also issued lower quality debt, which included $1.1 billion U.S. dollar denominated senior secured notes.

This weekend’s drone attacks resulted in one of the largest sudden supply disruptions in history. Although we expect Saudi Arabia to get oil production back on track relatively quickly, concerns over further attacks should keep crude oil prices higher in the medium term. We look at this unfortunate event as an opportunity to de-risk some lower-quality energy names out of high yield portfolios. The effect on bond prices this morning looks mostly muted, but we expect industry wide dollar price appreciation if inflated prices are sustained. We would swap this exposure into BB credits in the short-end and intermediate part of the curve.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.