The Economy

The list of challenges that are impacting global economic growth includes significant growth in debt levels, the China – U.S. trade war, Brexit, and shifting financial regulations. The domestic economy has additional challenges, including slowing private credit expansion, weak business formation, and a shifting decline in aggregate demand. Now, we face a new problem: Hurricane Dorian. We expect the category 5 hurricane blasting the Bahamas, Florida, Georgia and South Carolina to have a near term slowing impact on the regional economy.

In the face of these challenges, US GDP has grown on average at a rate of 2.6% in the first half of 2019. We expect the economy to grow at 1.8% this year; however, the risks are to the downside heading into the remainder of the year.

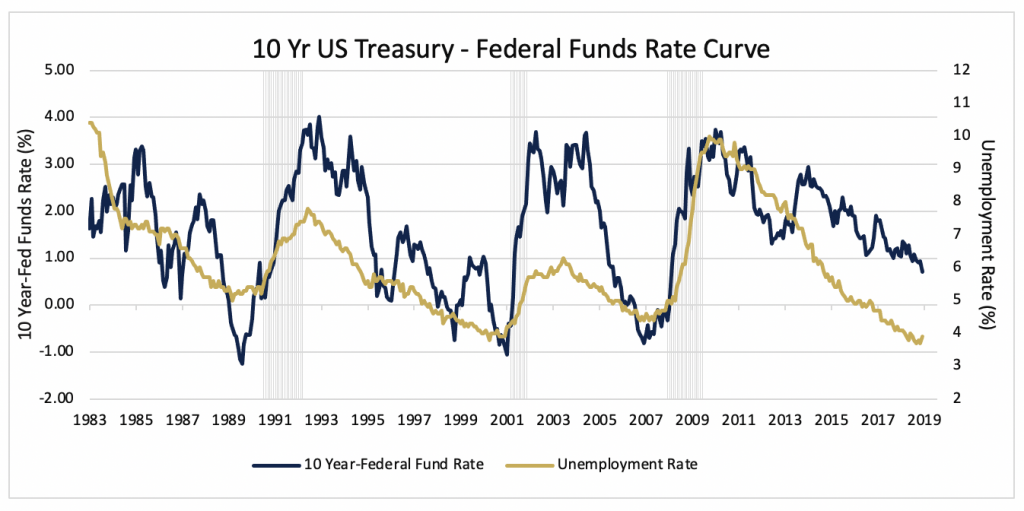

There has already been much written around the recent inversion in the yield curve and its potential impact on the economy. The bottom line is that the economy is slowing, and we are likely to experience a recession in 2021. However, the push to zero level, or in some cases, negative interest rates is not sustainable and will cause severe damage to the capital markets. More on this later.

Investors should focus on three things: corporate earnings, the next move from the Federal Reserve, and the health of the consumer sector.

First, corporate earnings are slowing. We expect earnings on the S&P 500 to come in around $175. We are encouraged by revenue growth, but we are cautious on operating margins. As management moves to protect earnings and sustain profit margins, we expect lay-offs to increase in the fourth quarter, which could shift the unemployment rate higher. In addition, the growth in debt in the corporate sector is magnified as earnings growth slows and the margin for servicing the debt becomes more challenging.

We expect the Fed will be more aggressive in lowering short term interest rates in light of the uncertainty around the U.S. – China trade war. To the extent that the trade dispute is settled, the impact on domestic economic growth will take six to twelve months. We expect the Fed will lower interest rates again at its September meeting.

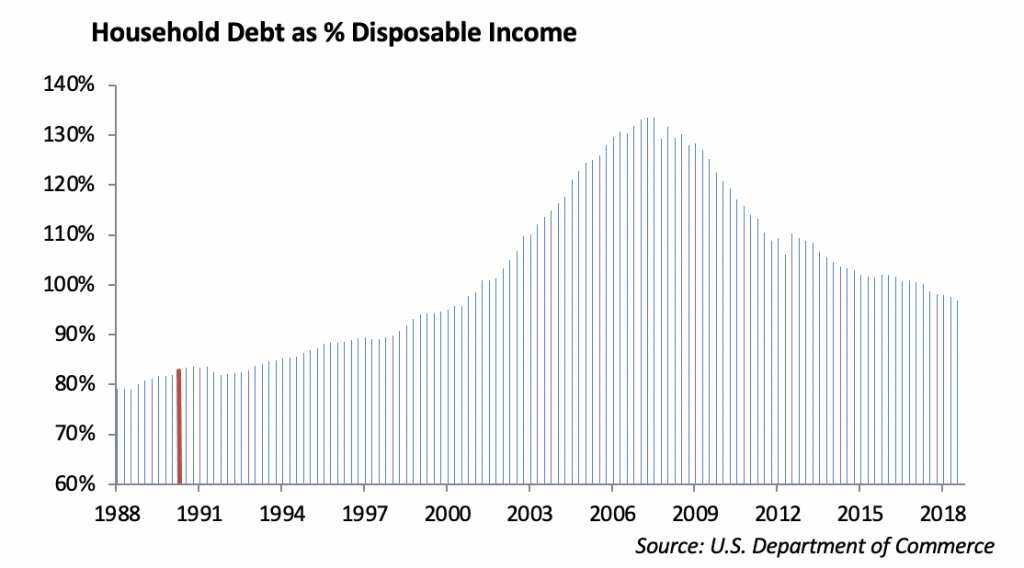

Finally, the consumer has shown resilient strength over the past year. As unemployment has declined, wages have increased. Household debt is still a problem, however, discretionary spending as a percent of household income has been healthy. Household debt as a percent of disposable income is below its peak level of 140% in 2008, but nowhere near the 95% level in 2000.

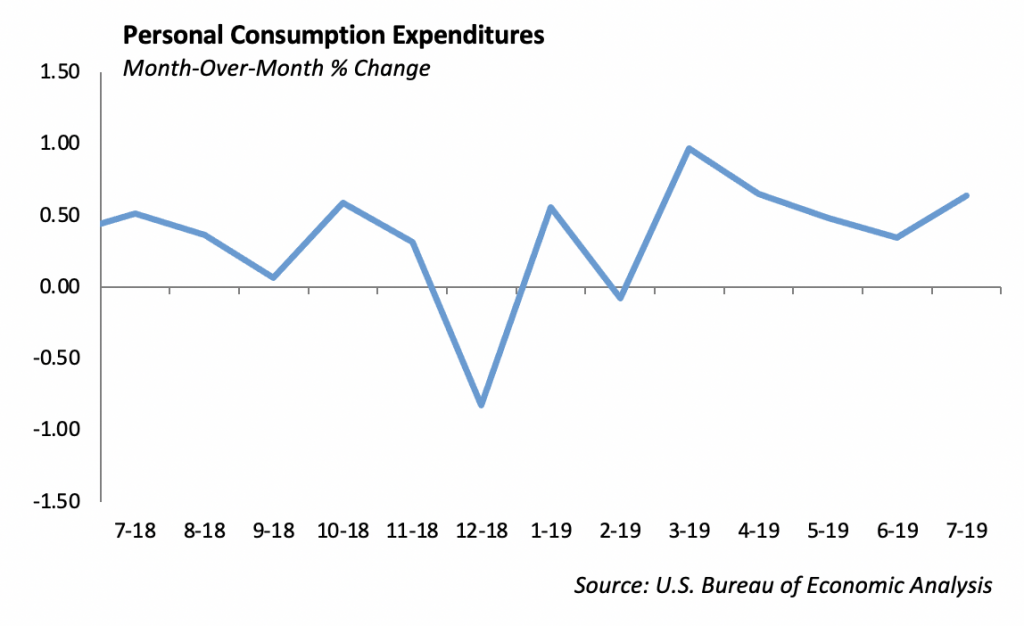

After a mild dip in the December of 2018, Personal Consumption Expenditures, reported by the Bureau of Economic Analysis have remained strong. It appears the consumer is utilizing debt to fuel consumption; however, their ability to service the debt at current income levels appears reasonable. When economic growth slows, the consumer debt burden will become an anchor for consumption.

Monetary Policy – This is not Normal

We have always maintained that capitalism and democracy go hand-in-hand. In the Wealth of Nations, Adam Smith wrote “Every man, as long as he does not violate the laws of justice, is left perfectly free to pursue his own interest his own way, and to bring both his industry and capital into competition with those of any other man.” Capital markets in a democratic society, with regulation designed to guide behavior of its participants and not impeded capital formation, are essentially a clearinghouse for the pricing of risk.

However, our form of capitalism (and our democracy) is evolving. Over the past ten years, following the Financial Crisis, monetary policy has been the main engine for economic growth of developed countries. Unfortunately, we believe this is not sustainable. And, with over $15 trillion of sovereign debt now trading at negative interest rates, capitalism is being challenged.

Investors require a risk free rate and a risk premium in which to measure their investment. Capitalism was not designed for a world of negative interest rates, and thus a negative risk free rate. Ultimately, a world with negative interest rates will require sovereign support in order to sustain capitalism.

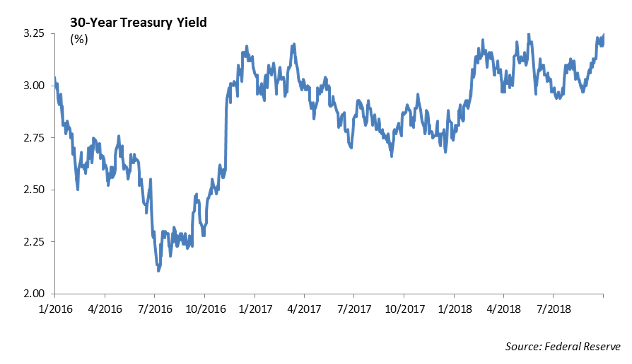

The yield on the 30 year U.S. Treasury bond dipped below 2.0% last week, declining to a level that is lower than the dividend yield on the S&P 500.

Equities

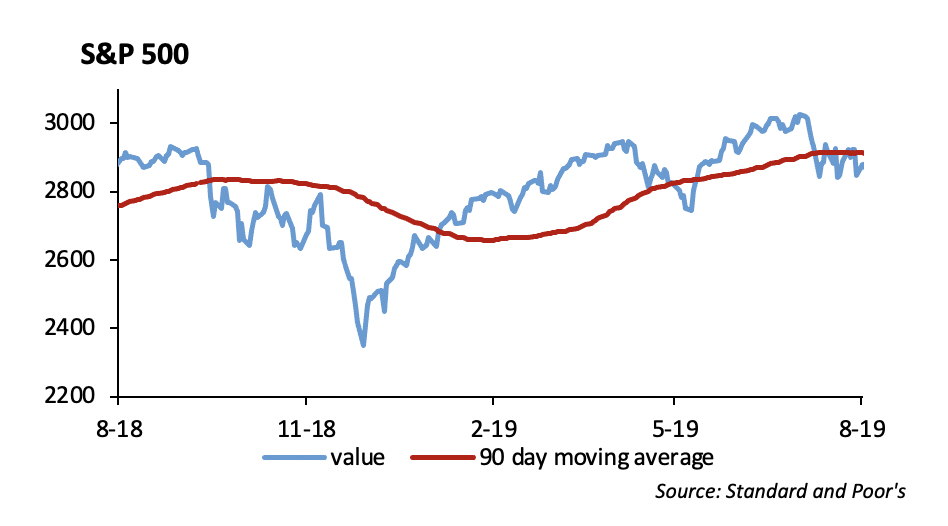

The S&P closed last week with a 2.79% gain, up to 2926. It is up 16.74% YTD and just over 3% away from all-time highs. The month of August was very volatile, but all in all, the S&P finished with a 1.8% loss for the month. Looking at sector performance, Real Estate and Utilities were the only sectors that were positive for the month rising 5%, and 3%, respectively. Energy was the worst performing sector, falling 8%, while financials also fell 6%.

Corporate results for the second quarter were in line. S&P earnings rose just 0.7% YoY. Sales and earnings were up 5% and 4%, respectively. For 2019, analyst expectations for growth have been revised to 2%. For 2020, forecasts are for sales growth of 5% and earnings growth of 11%.

In updated China news, China stated they wouldn’t retaliate against U.S. tariffs set for September 1. The Commerce of Ministry stated that they are willing to resolve the trade war with a calm attitude, which helped markets this week. Talks between the two countries will continue to be held throughout September. This will be the main headline as the S&P continues to be range bound for weeks, finding support around the 2825 level, while finding resistance at 2940.

Given the strong performance in domestic equities and a desire to play defense in portfolios, we are shifting our Large Cap Blend portfolio. We are OW both Consumer Staples and Utilities moving forward and hope to add some names alongside WMT and COST.

The dividend yield on the S&P 500 is currently at 1.92%. We are flirting with the yield on the 30 year U.S. Treasury trading below the dividend yield on the S&P 500. Clearly, this is not normal. However, what is more telling is that the dividend yield historically trades near a 4.3%. The dividend growth rate for the S&P 500 is 9.98% (annually ending June 2019) which is well above the average of 6.04%. While this underscores the strength in domestic corporate earnings, we expect the fundamentals to deteriorate over the second half of the year.

Fixed Income

As bond yields have generally declined, we began to see a sustained inversion of the yield curve as measured by the 2-year to 10-year US Treasury. As a firm, we are wrestling with the idea of whether an inverted curve matters in today’s economy. The question is whether unprecedented low yields make this time different. Yields across the globe continued to dip to all-time lows over the past week. The US 10-year is below 1.5% and the German 10-year is at -0.72%.

Investment grade credit outperformed treasuries over the past week as investors began to believe some resolution in the China trade war. We believe a near term resolution is not likely and have used market rallies to reduce credit exposure across portfolios. We have been moving portfolios towards a defensive tilt by gradually reducing duration and increasing credit quality. A heavy new issuance calendar over the coming week should produce more trading opportunities as concessions should be higher given market volatility.

Municipal Bonds

Muni continue to underperform treasuries and the ratio of 30-year munis versus treasuries moved firmly above 100% over the past week. Outright yields have created a challenging environment for individual investors and we have seen fund outflows that have produced weakness in the sector. 10-year AAA muni’s are now yielding 1.26% which translates to roughly a 2.10% tax equivalent yield. Given the relative cheapness of muni’s, we are recommending investors move up in quality into municipal bonds in strong regions of the country. Municipals are generally less volatile that corporate credits during market dislocations.

High Yield

In a trading week summed up mostly by the word quiet, U.S. high yield credit did have solid performance. The index saw 16 basis points of option-adjusted spread tightening, paired with 0.52% of total return. Total return breakdown via risk tiers was relatively consistent with Bs slightly outperforming at 54 bps of total return and BBs the slight laggard at 50 bps of total return. No new issuance last week certainly helped keep spreads compressed. August issuance totaled $11.3 billion, which is the lightest month we have seen this year so far. We are looking for high yield new issuance to pick back up this week. We expect issuance to be relatively heavy going into the fall as with low rates we see ample opportunity for high yield credits to refinance to improve their credit profile. We would expect increased supply to loosen up spreads and make the secondary market start to look attractive.

High yield funds flows were positive as $689 million went into high yield mutual funds and ETFs last week. This is in contrast to the $1.5 billion outflow the week prior.

Energy markets were up across the board last week as WTI and Brent both rose 2% last week and natural gas raising a substantial 6% last week. The rise in energy prices was mostly due to Gulf of Mexico supply concerns with Hurricane Dorian.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.