Equities – What Just Happened!?

Jobless Claims Underscore Slow Economic Recovery

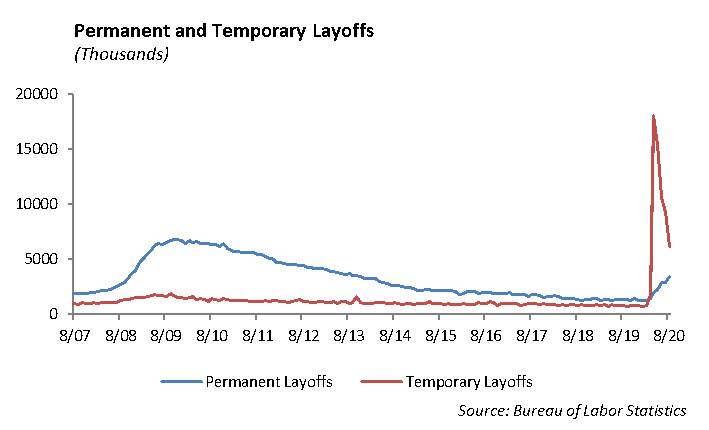

Since the pandemic began to choke the economy over six months ago, layoffs remain widespread and the job market remains weak. Last week, 833,000 workers filed claims for unemployment benefits. This figure is not seasonally adjusted and represents an increase from the prior week. The initial momentum to put people back to work has slowed. During the March and April period, over 22 million jobs were lost, and roughly nine million have been regained. The rate of unemployment has declined from 10.2% to 8.4%.

However, the number of companies announcing layoffs is rapidly increasing as companies take steps to protect profit margins and control expenses. Last week, Salesforce announced that it was laying off 1,000 workers as it reported solid quarterly earnings. At the same time, MGM Resorts announced the company was laying off 18,000 workers, and Coca-Cola announced separation packages for 4,000 employees. We expect layoff announcements to continue into the fourth quarter, which will slow progress in employment.

Sustained Economic Growth Will Not Be Achieved without Fiscal Stimulus

The domestic economy needs government support to help mute the negative impact of the coronavirus on business and consumption. We still expect another fiscal stimulus package before the election in order to limit the damage of the coronavirus on the economy. However, Republicans and Democrats have not been able to agree on the size of the package and where stimulus should be applied in the economy. Time is running out. The $600 extra weekly government assistance for unemployed workers expired in late July. The Paycheck Protection Program has largely run its course. The longer it takes to get assistance to unemployed workers unable to make rent payments and small businesses fighting for survival, the more damage that will be done to the economic recovery effort.

Problems are beginning to fester. We see it in the increased number of homes listed for sale through foreclosure, the number of people skipping their August and September rent payments, and the increased number of companies that are announcing layoffs.

Even Federal Reserve officials are weighing in. Last week, Cleveland Federal Reserve President Charles Evans said the economy needs continued support and the government is spending too much time fighting and unable to deliver.

Update to Equity Strategies

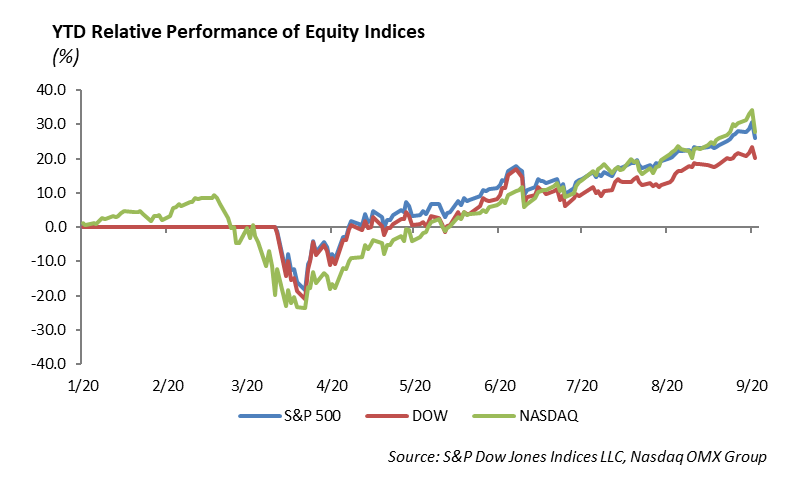

The S&P 500 Index closed the month of August with a gain of 7%, making it the fifth straight month of gains for the Index. The NASDAQ was up 11%, and the DOW was up almost 8%. The top performing sectors for the month were Technology, Consumer Discretionary, Industrials, and Communication Services, all returning more than 8%. Year to date, Technology still leads all sectors, returning 29%.

On Thursday, the S&P fell -3.5% and the Nasdaq fell -5%. After the huge run Technology has had all year, it ended the week with a 6.2% selloff. This was not a case of trade tensions, virus numbers or any other headline. From both a technical and fundamental perspective, the Technology sector was expensive. Pullbacks within this sector should be expected after a 70% rally in five months. Additionally, in a new market environment in which volatility spikes send markets moving much quicker in either direction, pullbacks are intensified. The performance of the S&P over the last month has not been Technology-dominated. It has been broad, with Industrials leading the pack. Technology is the sixth- best performing sector. The sector rotation started slowly, and took a more aggressive turn last week.

Update to Fixed Income Strategies

Fixed income continues to be the sleeping giant ignored by many investors. Despite the euphoria equity investors feel, bonds indicate that inflation is not upon us, and growth will be challenged for the foreseeable future. US Treasuries fell again this past week, with the 10-year falling -8bps to 0.71%. The Federal Reserve is resolved to keep rates low for quite some time, and the likelihood of negative-yielding, short-term debt grows as current rates fail to instigate target inflation.

Despite falling yields and increased volatility in equity markets, investment-grade credit fared well over the week. A lack of primary issuance supported spreads, with investors eager to find any safe haven from equities and cash. Even high yield spreads remained subdued, wider by only 5bps through the volatile week. We are not overly surprised by the muted volatility in credit due to the active hand of the Fed in the corporate bond market. It seems their initiative to stabilize the bond market is working for now.

With US Treasury yields at historically low rates and credit spreads tight, idea generation has been difficult. Over the past week, we added 30-year Apple, Amazon, and Google to our fixed income portfolio. These securities played two parts across our strategy. One, as rates spiked higher after last week’s Fed minutes, we were tactically extending duration. Secondly, we see these securities as upgrade candidates to the rare AAA rating only held currently by Microsoft and J&J. As the market cap of these companies have risen significantly, their debt to equity ratios have essentially been cut in half. Frankly speaking these companies cannot issue debt fast enough to maintain leverage ratio. Google and Apple have 50% more cash on their balance sheet than they have debt. We believe these cash flow machines are not the tech of 1999 and will eventually be upgraded, leading to meaningful spread tightening.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2020 Winthrop Capital Management