Economic Update

As economic growth is subdued and large parts of the economy remain shut down in the face of a spreading coronavirus, the Federal Reserve contributed its narrative to this economic tragedy. At the regularly scheduled Federal Open Market Committee meeting last week, Chairman Powell announced a change in the Fed’s policy statement, making it clear that the Fed would maintain a low level of interest rates and capital market support until 2024. This means that the average level of short-term interest rates would average 2%, and the rate of unemployment would fall to 4%.

In a zero interest rate environment, traditional tools have limits to altering the flow of credit and impacting the level of interest rates. However, the most powerful tool the Fed may have to alter investors’ behavior is its voice. Since the Financial Crisis, the Fed has struggled to get inflation to 2%. Once inflation finally drifted higher, the Fed moved to increase interest rates in attempt to curb an acceleration in inflation, which curtailed economic growth. Now, it appears the Fed is prepared to allow the rate of inflation to run hot by allowing it to drift above 2% for a sustained period.

We will not have sustained economic growth until there is a reliable way to limit the spread of the coronavirus and allowing other parts of the economy, including travel, hospitality, leisure and restaurants, to completely reopen. The key to the economic recovery is still employment. The good news is that the number of workers receiving unemployment benefits decreased last week by 916,000. The bad news, however, is that the total number of unemployed still sits at close to 12.6 million people. The increase in the rate of retail sales rose 0.6% in August. While consumers are spending, it is at a slower pace than previous months, which raises concern that the consumer led recovery is beginning to decelerate.

In addition, the major airlines last week made another push to the Administration for additional bailout funds.

Portfolio Models

Over the past several years, our allocation to International Equities has been below historic targets in our Portfolio Models. Our outlook for global growth has been subdued since the Financial Crisis. In addition, our weightings between developed countries and emerging market economies has consistently favored developed countries as the economic outlook for emerging market economies has been much lower. The capital flows have also declined, and emerging market economies require capital for business investment.

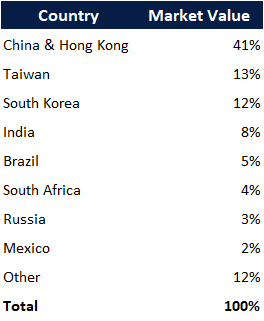

In the 1990’s, emerging market indexes represented a diversified representation of the fast-growing economies. The largest were Brazil, Russia, India, China and South Africa – known as “BRICS”. Today, the emerging market landscape has changed significantly. The composition of the MSCI – Emerging Market Index is currently represented by 41% in China and Hong Kong, 13% in Taiwan and 12% in South Korea.

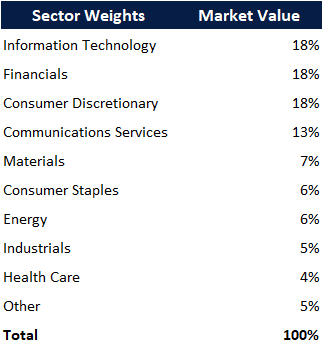

The Information Technology, Financials and Consumer Discretionary sectors are the largest in the index at 18%.

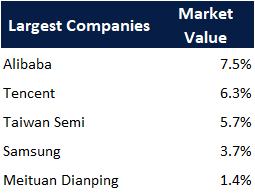

The largest holdings are Alibaba (BABA), Tencent (TCEHY) and Taiwan Semiconductor (TCM), which combined represent nearly 20% of the market value of the Index. The market cap of Alibaba is at $750 billion, which is roughly the size of the GDP of Turkey. The dominance of China and large technology companies in the index creates a level of idiosyncratic risk that may be inconsistent with the objective of a diversified market index.

Our long-time readers may know that we view China’s form of state-controlled capitalism as a different model to our democratic version of capitalism. Our initiative heading into the end of the year is to restructure our International exposure and treat China as a separate sleeve within the internal allocation.

Equity

The S&P ended the week down -0.64% to end at 3319, making it the third consecutive week of declines. The index is still up 2.75% year-to-date. The NASDAQ was down 0.56% last week and is still up 20.29% year-to-date. As technology led the index to a remarkable comeback, it has also led the way in the recent decline. Valuations have been quite elevated within the Technology sector, but earnings outlooks remain positive. For 2020, earnings for the sector are expected to rise 5%. For 2021, earnings are expected to rise 14%.

Looking at international markets, the Schwab International Equity ETF is down -4.61%, while the Schwab Emerging Markets ETF is down -1%. International stocks have underperformed domestic equities over a 1-year, 3-year, and 5-year horizon. With uncertainty in economic growth and rising geopolitical tensions, it has been difficult to find opportunities overseas. One place to look in the near term is China. China’s explosive e-commerce growth, booming middle class and strong recovery within their manufacturing sector makes Chinese equities attractive. China’s e-commerce market is growing over 30% this year as companies become more productive and the middle class continues to grow. With continued tax cutting strategies, the middle class population is expected to make up over two-thirds of the population. Currently, that number is under 50%. The continued rise in productivity in China’s manufacturing sector and growing middle class will continue to drive consumption. A company that currently dominates the Chinese consumer market is Alibaba.

Alibaba Holdings Group (BABA)

Alibaba is expected to produce another quarter of enormous revenue growth, boding well for their fintech arm, Ant Group. Ant Group’s revenue is projected to double to close to $120 billion. This does not account for the slower first half of the year and the fact that Singles’ Day is in November. The Alipay platform operated by Ant Group is the largest online insurance services platform in China. With 1 billion annual active users, Alipay is the largest online consumer credit provider. It is also the largest online services platform in China by AUM. With China’s economy shifting towards domestic consumption, consumer needs for financial services have expanded, and the demand for credit, investment, and insurance products will increase substantially. Unlike the US, the average consumer in China does not have access to a banks where they can secure loans. Ant Group can use its data and reach, giving its platform tons of growth potential.

Fixed Income

Interest rates drifted slightly higher over the week, despite continued equity volatility. The yield on the 30-year US Treasury ended the week at 1.45%, up 4bps through the week. This is still a very low yield by historic measures, however. Germany, France, Sweden, and Japan all have 10-year bonds with negative yielding rates. In the aggregate, global bonds with negative yields are currently $15 trillion. With so much low or negative yielding debt, where should investors invest to achieve income and returns in the fixed income market?

Despite low yields and heightened volatility, the Bloomberg Barclays US Aggregate Bond index is up 6.84% in 2020. Performance has been driven by declining interest rates and tightening credit spreads. The average price of bonds in the index have risen above $115, coupons have declined sharply, and the duration of the index is now above 6 years. Without much runway for rates to decline and spreads to tighten much further, the outlook for returns are slim. The Euro Aggregate Index has lagged with a return of only 2.55%, but this is not much of a surprise given the extreme lows in European interest rates. Emerging market bonds, despite their higher yields, are only up less than 1% this year. Outside of the US, the best performing bond market in 2020 has been Chinese government bonds, which are up 4%.

The local Chinese 10-year trades at 3.12%, and while that outright yield seems low, it is fairly wide relative to US Treasuries. Over the past 5 years, the average difference between the US 10-year and the Chinese 10-year has been 115bps. Currently the difference is 242bps. On a relative value basis, this makes Chinese debt look attractive. As a sovereign issuer of debt, China has challenges for U.S. investors, However, China bonds are potentially going to be added to the FTSE Global Bond index this year. If Chinese bonds are added to the index, and trade issues are settled, global acts of aggression are tamed, and China is able to take steps to integrate into global financial markets, there is potential for outperformance in this market.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2020 Winthrop Capital Management