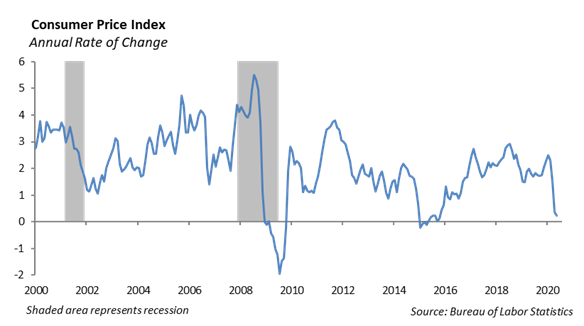

The Fed Redefines its Inflation Target.

The Federal Reserve made history this past week by indicating that they would allow inflation to run above the 2% target. As the central bank to the United States, the Federal Reserve has a “dual mandate” to promote maximum employment while maintaining price stability. In other words, the Fed promotes monetary policies that are designed to support the labor market through job growth while maintaining the rate of inflation at targeted levels the Fed deems appropriate.

Fed Chairman Powell indicated that Federal Reserve has revised its statement to allow for average rate of inflation to be 2% instead of the target level. The belief is that households have come to expect the average rate of inflation to be below the 2% level since, even in periods of economic growth, inflation has struggled to hit 2%.

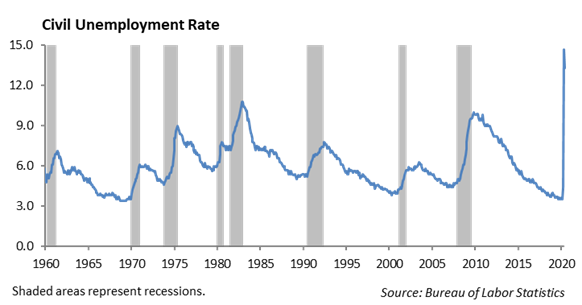

Currently, over 15 million people are out of work and the rate of unemployment rests near 10.2%. By making a strong labor market the focus and allowing inflation to accelerate past the 2 % target, the Fed is laying a path for sustained levels of low interest rates over a long time horizon.

The Economy – Whistling Past the Graveyard

Over the past several weeks, we have warned that the economy is at a crossroads, and investors are underestimating the risks in the economy and capital markets. The stimulus money that has helped support small business and consumers has run out. Congress has been unable to reach a deal for additional stimulus. Now, as 15 million workers remain unemployed with little income, the bills are going unpaid. In the absence of additional stimulus, economic growth will decline. Layoff announcements are increasing and furloughed workers remain sidelined. As tax collections decline sharply, the financial position of state and local governments is quietly deteriorating this year. In addition, the commercial real estate market around the country is under stress as renters seek forbearance from monthly rent obligations. We currently do not have sustained economic growth and the economy needs a comprehensive fiscal stimulus plan to support it through the pandemic.

Five Stocks to Weather the Storm – Revisited

In early April this year, we put together a five stock portfolio that we thought would help investors to weather the storm of the COVID-19 pandemic. At that point, we didn’t know how long businesses would be locked down, the severity of the pandemic on businesses or its impact on the financial markets. Here is an update to the five stocks we recommended.

Amazon.com (AMZN)

The price of Amazon.com (AMZN) has increased from 1847 at the beginning of the year to 3401, providing investors with a return of 84.10%. The company has executed on both the on-line retail business and its cloud services business.

AMZN has gross margins of 40% and operating margins near 5%. With Debt/Total Assets of 34.5% the company has a fairly conservative balance sheet. With a market value that has now grown to $1.7 trillion, the debt to equity ratio has declined significantly. We expect the company’s earnings to be between $30 and $32 per share. The company has been firing on all cylinders, with double digit growth in both cloud services, only shopping, and whole foods. At the current price of $3401 per share, AMZN stock trades at a P/E of 55x earnings and 5x sales per share. The stock is trading relatively expensive but we believe over the next 2 years the company will continue to grow into their current valuation. The company has been aggressive at building out its logistics infrastructure including investment in transportation and warehouses across the country. We believe this company is well positioned for an economic downturn and recovery and continues to be one way to build defense into an equity portfolio.

Johnson & Johnson, Inc (JNJ)

The price of Johnson & Johnson (JNJ) has increased from 146 at the beginning of the year to 153, providing investors with a return of 4.4%.The company has been impacted by the coronavirus and many segments have not hit expectations due to a shift in healthcare in order to focus on patients with COVID-19.

Earlier this month, the company announced that its Janssen Pharmaceutical Companies subsidiary had entered into an agreement with the U.S. government for the large scale domestic manufacturing and delivery in the U.S. of 100 million doses of Janssen’s SARS-CoV-2 investigational vaccine, Ad26.COV2.S, for use in the United States following approval or Emergency Use Authorization by the U.S. Food and Drug Administration (FDA). JNJ continues to be a global leader in the fight to control COVID-19 and the development of a vaccine.

Additionally, JNJ has acquired Momenta, an autoimmune disease drug maker for $6.5 billion. The acquisition was immediately accretive and we believe is a good addition to a fast growing biopharma segment. JNJ remains relatively cheap to the S&P 500 at 16x earnings and 22x free cash flow per share for 2020. A breakthrough vaccine for the Covid-19 would be an obvious boost to earnings and valuations, but regardless we believe the company will generate $15 billion in earnings and $17.5 billion in free cash flow to support future growth while remaining less volatile than the overall market. With a 2.7% dividend and diverse portfolio, the stock adds a lower volatility to an equity allocation. JNJ continues to release positive pre-clinical data from its SARS-Cov-2 vaccine candidates as of July 31, 2020.

Microsoft (MSFT)

Microsoft (MSFT) suite of products have been the backbone on the enormous size and scale move to a “work from home” environment. MSFT is up 46.31% year-to-date, outperforming the S&P 500 by over 35% and the technology sector as a whole by 10%. Revenues are on pace to grow by 15% and margin expansions through 2020 have led to earnings growth of 25%. The acquisition and integration of Microsoft Teams in 2018 has proven to be an extremely well timed addition to the suite. Daily active users have grown from 13 million in July of 2019 to 75 million as of the end of April 2020. We believe the shift to working from home is becoming more solidified as most industry reports show that productivity since the shift has increased meaningfully. While MSFT is trading at a lofty 30x next year’s earnings, we believe earnings will continue to outpace consensus estimates as the reliance on 365 and the accelerated shift to the cloud will be a tailwind for the next five years.

Lockheed Martin Corporation (LMT)

Lockheed Martin (LMT) has lagged the overall market, returning 2.89% in 2020. As the US deficit continues to increase and with election season on the horizon, there is some concern that defense budgets would be cut. Despite this concern, Lockheed won a $62 billion contract for F-16 fighter jet production for several foreign countries spanning over the next 6 years. We also believe there is a high likelihood that as the UAE and Israel have signed a peace agreement, an F-35 contract could come for the UAE. LMT looks cheap relative to the market. We believe 2020 earnings will come in at $7 billion leading to a forward P/E ratio of 14.5. Additionally, at a ratio of 10x free cash flow per share is one of the cheapest stocks in the S&P 500.

Alphabet, Inc. (GOOG)

Alphabet (GOOGL), continues its steady growth trajectory as cloud has grown 42% and Play has grown 35% so far this year. An increase in people staying at home has also driven double digit returns in YouTube ad revenue. GOOGL continues to invest some of their $121 billion cash hoard toward acquiring FitBit and a stake in ADT’s home automation through this year. Alphabet is up 22.40% in 2020 and like the majority of the S&P 500 leaders, has experienced a P/E ratio expansion to 25x next year’s earnings. We believe low interest rates and the expected consistent growth in both revenue and earnings justifies the multiple expansion. In addition, we believe GOOGL is well positioned to be a leader in the home automation space.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.