The Economy

After the recent attacks on Saudi oil fields, the price of oil spiked last week as expectations for Saudi oil output were cut by 50%. However, by the end of last week, the price of oil experienced a sharp decline as Saudi energy officials confirmed that production could be back on line as early as one month. We don’t believe it. Fingers are being pointed at Iran as the perpetrator of the attack.

Last week, the United States took the lead in drawing up penalties for Iran, starting with blacklisting the Central Bank of Iran and two other state run financial institutions as well as preparing to outline a case to censure Iran in front of the United Nations this week in New York. This is less than one month after French President Emmanuel Macon invited Iran’s Foreign Minister to the G7 meeting in Biarritz France, creating confusion over policy for the Middle East. This morning, Iran released the British oil tanker, which it had seized in the Straits of Hormuz last July, in a potential sign of easing tensions.

In the face of slowing global economic growth, the Fed moved to lower short term interest rates last week, providing a catalyst for a rally in stock prices. However, the list of growing risks in the capital markets casts a shadow over the rally. The list includes slowing economic growth, a growing labor shortage, business formation that is concentrated in underfunded start-ups, increased protectionism acting as a barrier to globalization, and declining earnings growth.

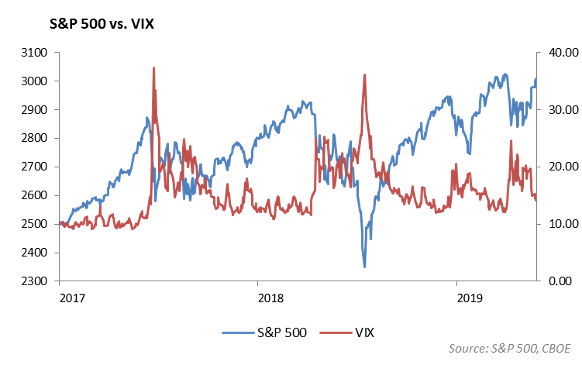

We expect the possibility of a volatility spike in the fourth quarter to increase. Volatility moves in the opposite direction of stock prices. While current volatility, measured by the VIX, is currently trading near 14, we would expect normalized volatility to range between 20 and 25. We continue to move to reduce risk across asset allocation strategies and Portfolio Models heading into the fourth quarter.

Monetary Policy

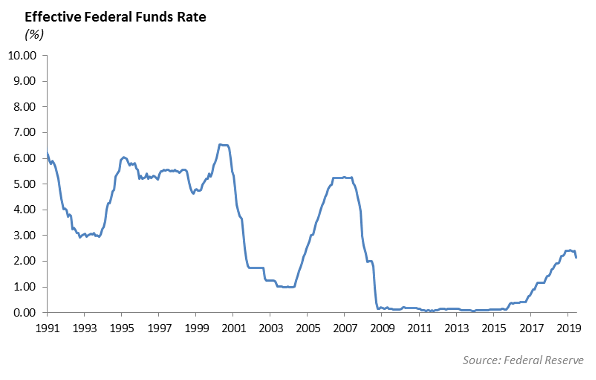

As expected, the Federal Reserve lowered short term interest rates by 25 basis points last week, leaving the targeted Fed Funds rate at 1.75% – 2.00%. The economy continues to show consistent job growth, and the consumer sector has shown resilience in the face of growing geo-political concerns. However, the Federal Reserve has signaled concern about the uncertainty of the current trade policy with China and the negative impact that is having on business investment.

At the same time, Chairman Powell has been under attack by President Trump for not moving more aggressively to cut rates in order to boost stock prices. Trump tweeted after the Fed announced its cut in targeted Fed Funds last week, “Jay Powell and the Federal Reserve fail again.” This past summer will mark a historic period in financial market history as the independence of the Federal Reserve was tested by a sitting President.

We hit another milestone in financial market history last week. Since the Financial Crisis, the Federal Reserve has not intervened directly in the market for repurchase agreements. Last week, the New York Fed provided $75 billion in direct loans to banks in order to support liquidity in the overnight funding markets. A combination of issues, including strong demand for overnight funds and a shortage of collateral, caused overnight repo rates to temporarily spike to 10% early last week. The Fed intervention has been successful at pushing overnight rates lower. However, the spike in repo rates may be pointing to underlying structural problems in the capital markets which are masking liquidity issues in credit and money markets.

Equities

The S&P was down 0.51% this week overall, ending on Friday at 2992.07. Year to date, it is up 19.36%. We are about 1% away from all-time highs. Given the recent rally, we turn a focus towards market valuation. Using a top-down forecasted growth rate of around 3.5% for the next 5 years and adjusted earnings at $154.54, the index is valued at just under 3100. However, we choose to use a more conservative growth rate of closer to 2.00%, therefore valuing the index at 2900. This indicates that we are currently at a premium of about 3% on the index.

FedEx Corp shares were down 13%, which is equivalent to almost $6 billion in market cap lost. There was lower revenue guidance for the Express unit for cargo by planes, specifically Europe. This is their largest unit by revenue, and it dropped by 3%. They also reported an 11% earnings decline and cut its profit and revenue forecast. Earnings are expected to fall by 29%, whereas expectations were closer to mid-single digit.

General Mills beat estimates by 2 cents a share, and revenue came short of estimates, down 2% at $4 Billion. They experienced poor demand in certain brands like Yoplait and Nature Valley granola bars. Comp sales fell 1% in the quarter. The company is facing pressure to sell foods perceived as healthier and fresher. US Cereal was up 1%, while stock was only down about 1%.

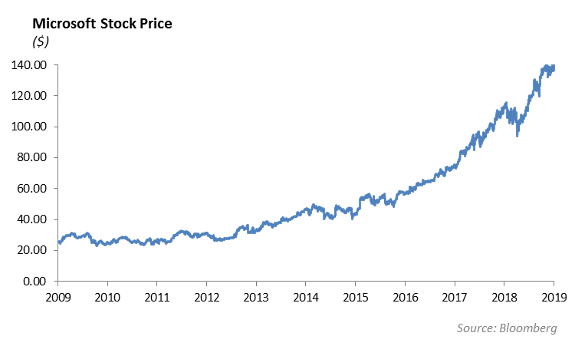

Microsoft (MSFT) announced last week that it will repurchase up to $40 billion of its stock and increase its dividend by 11%. This is the third time in the past six years that the company has authorized a substantial stock repurchase program. MSFT has been firing on all cylinders, and we are especially high on the growth prospects in their cloud business. Revenue is up 12%, and profits increased almost 50% from the prior year. The current market cap of MSFT places it as the largest publicly traded company today.

In scheduled earnings for the week, Nike will report Tuesday after the close, Conagra will be Thursday, and Micron will report Thursday after the close.

In IPO news, five health and tech companies went public this week, with all of them ending the week up over 20%. Data Dog was the biggest, with a market cap of $8.7 Billion. Airbnb announced it would look to IPO in 2020. The Renaissance IPO Index is up 31% YTD, with top holdings Spotify and Roku.

Fixed Income

Volatility in the rates market continued to remain high last week as the Fed, with little surprise, lowered the Fed Funds Rate by 25 bps. Rates fell over 10 bps across the curve, which generally flattened through the week. The 10-year treasury now stands at 1.76% and the curve remains barely positively, sloping at 4 bps.

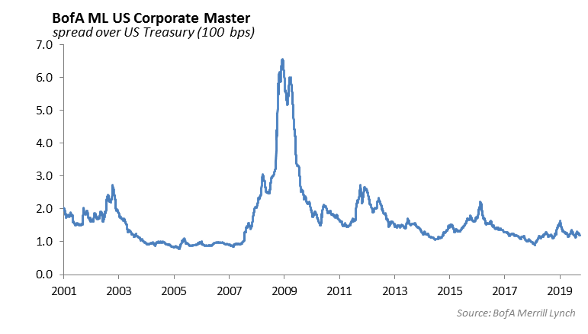

Investment grade spreads tightened during the week despite falling yields and a solid week of new issuance. New issuance came in at $23 billion, and books were generally 4x oversubscribed. Of significant note, the performance of the $140 billion in new issuance over the past 3 weeks has had a very concentrated theme. Paper issued with a maturity of 5 years or less has had extremely strong performance, but paper issued with a maturity of 10 years or greater has lagged. A specific example is Hospitality Partners, which issued both five and ten year debt. The 5-year bonds have tightened 15 bps from issue, while the 10-year bonds have widened 5 bps from issue. We believe this is largely driven by money managers’ reluctance to put on excess duration during a time of historically low interest rates.

A theme of unwillingness for investors to take on duration risk has been building over the past few years. According to Bank of America/Merrill Lynch, it is estimated that the duration gap for pension and insurance companies is close to 10-years as a whole. Therefore, these money managers are funding portfolios with a duration of 10 years shorter than the liabilities they are meant to offset. With the 10-year US Treasury tighter by 150 bps over the past year, this trend may create a serious problem. As interest rates continue to stand at historically low levels, this could create a pain trade that will force managers to buy up duration on any spread or rate weakness. We see this as an investment theme heading into 2020 that will continue to drive both rates and spreads tighter. Any sell-offs in the credit markets will be quickly bought up as institutional money managers are forced to bridge this gap any way they can.

High Yield

The U.S. high yield credit market saw a very modest spread tightening of 2 basis points last week, resulting in the fifth straight week of positive performance. The index is 152 basis points tight of year-end 2018 levels. For total return, the index as a whole returned a positive 28 basis points, led by Bs at 44 basis point and BBs at 30 basis points. Performance was dragged by the CCC risk tier, which saw a negative 38 basis points of total return. BBs are still the top performing high yield risk tier, seeing over 13% return year-to-date, while Bs are about 12% return and CCCs about 7% return.

High yield fund flows were positive once again at $3.29 billion versus the previous week’s lesser inflow of $1.86 billion. Year-to-date inflows now total $15.4 billion as we’ve seen the back and forth nature of inflows and outflows transpire over the last three quarters.

The new issue market remained active last week to a tune of $5.5 billion dollars of volume pricing. Year-to-date volume is now just over $190 billion, marking a 29% increase over the prior year period. Notable issuers included Charter Communications, which issued B-rated senior notes to fund buybacks and take out upcoming maturities, and NextEra Energy, which issued $500 million of 144a, Ba1/BB, 7 year notes that were 5 times oversubscribed and priced at a tight 3.875%.

With a move back to rallying rates, and Bs being the outperformer in the past couple of weeks, we continue to stress the up in quality trade. We’re exploring the idea of allocating high yield dollars to BBB names in order to provide added protection in the event of market credit deterioration.

Looking at the aftermath of the attacks on Saudi Aramco facilities, WTI rose by 6% or $3.24/bbl, Brent rose by 7% or $4.42/bbl, and natural gas actually fell by 3% or $0.08/mcf. On a weekly basis this is the largest gain in about eight months, but gains softened considerably from the originally 10% and 11% rises seen. Prices declined after news that Saudi Aramco is well equipped to bring production and capacity back in a timely manner. It would be surprising to see crude oil prices decline to their previous levels, as conflict risk most likely introduces a new premium on long-term oil prices.

Portfolio Models

With stocks near record levels and interest rates sharply lower, we are taking several steps to reduce risk in our asset allocation and Portfolio Models heading into the fourth quarter. Domestic equity remains the largest exposure to the equity basis. We are shifting a portion of the broad market equity strategies into low volatility and adding large cap value.

International stocks, measured by the MSCI, have lagged domestic equity, measured by the S&P 500 through this year. Within the international equity allocation, we expect to maintain the current allocation; however, if valuations warrant, we will increase exposure to international equity heading into the end of the year.

While we have not included global fixed income allocation in our models, we are exploring the potential allocation to the global fixed income sector in an effort to diversify away from U.S. interest rates. However, the barriers of high fees and increased volatility remain.

We are increasing exposure to liquid alternatives in our Tactical Allocation Models. We are evaluating a potential increase in exposure to global macro and multi-strategy funds. The challenge is finding funds with good performance, high sharpe ratios, and low fees.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.