Economy

“It was the best of times, it was the worst of times.” – A Tale of Two Cities

In spite of a solid employee report last week, the manufacturing and service sectors showed signs of slowing last month. As the global economy slows, the domestic economy is showing signs of slowing as well.

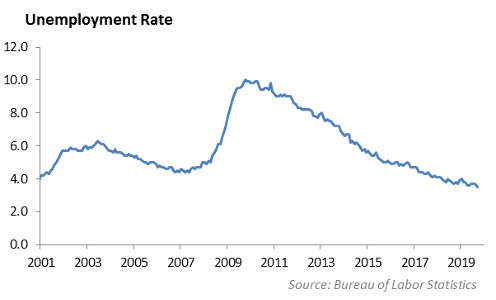

According to the Labor Department, the economy added 136,000 jobs in September. The U.S. consumer is generally able to find work, which in turn, supports wage growth. The unemployment rate shifted into a 50-year low of 3.5% in September from 3.7% in August. At the same time, wage pressure is still low. Job gains combined with low unemployment buffers the U.S. economy from weakness and supports wage growth, all of which helps to spur consumer spending.

We are reluctant to think that this rate of job growth and unemployment will hold up next year given the pressure on corporate earnings and the growing list of companies announcing restructurings and lay-offs. Last week, HP announced a plan to reduce headcount by 7,000 to 9,000 employees.

The Institute for Supply Management (ISM) tracks both manufacturing and U.S. services sector activity each month. A reading above 50 shows growth, while a reading below 50 indicates a contraction in activity. The ISM manufacturing index dipped to 47.8 in September, its lowest level since June of 2008. This is a clear sign that the trade war with China and slowdown in Europe are having an impact on manufacturing in the U.S. We expect trade flows with China will grow at their slowest pace since the Financial Crisis.

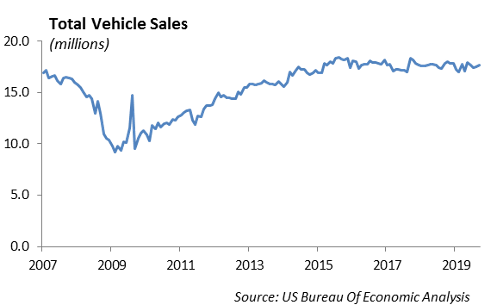

At the same time, auto sales are still tracking near 17 million units. We expect to see this figure begin to dip as general slowdown grips the domestic economy and the UAW strike at GM impacts production.

Monetary Policy

As the central banks of developed countries lower short term rates, we expect the Federal Reserve will continue to provide pre-emptive relief to the capital markets by providing liquidity. The central banks of Australia and the United Kingdom lowered short term rates over the recent weeks.

The repo market continues to show signs of dysfunction as the Federal Reserve in New York has intervened to suppress rates on short term loans known as repurchase agreements. Repo rates unexpectedly increased in mid-September despite a number of contradicting factors: tax payments hit, large deposits transferred from the banks to the government, bank reserves declined as the Fed shrinks its balance sheet, and a large amount of new issuance hit the bond market.

In effect, banks would rather have kept cash on their balance sheet than earn up to 10% in the overnight repo market. As we learn more about why this happening, it points to structural problems in the capital markets.

Equities

The S&P ended the week down only 0.33% after a 1.42% rally on Friday. Currently the S&P is up 17.76% YTD.

For September, value ETF’s were a great performer, returning 5%. YTD tells a different story as large and mid-cap growth ETFs are outperforming value ETFs. Small cap is underperforming value on a year to date basis. Healthcare was the only sector negative for September and is still the worst performing sector YTD, with energy not too far behind at a 6% decline in the third quarter.

Interestingly, the top performing sectors YTD are Utilities and Technology, highlighting the confusion in the market right now. Tech is up 31% and Utilities, a defensive sector, is up 25%.

In earnings news, Pepsi reported Earnings of $1.56 vs. $1.50 expected. Revenue was reported at $17.19 billion, up 4.3% year-over-year. Frito Lay North America was up 5.5%. Pepsi’s healthier brands, such as Bare, and beverage business saw growth with Gatorade Zero. The stock was up 3% on its report.

Constellation Brands reported earnings of $2.91, and revenue that was in line; however, the stock fell 5%. The company had equity losses of just under $500 million from its $4 billion investment in Canopy Growth. They reported strong beer sales again at 5.3%. Wine sales continue to struggle with a 10% drop this quarter. Constellation’s next move is into hard seltzer, which has seen immense growth in popularity over the last year. They plan to launch a Corona hard Seltzer drink next spring.

There is a fairly light earnings calendar this week, and it will pick up again next week with over 50 companies set to report.

The IPO market continues to face challenges. 6 companies were scheduled to price IPOs last week, but only 4 entered the public market. All 4 priced below the midpoint.

The We Company officially withdrew its IPO on Monday, while AirBNB has chosen Morgan Stanley and Goldman to lead a direct listing in 2020.

Fixed Income

Interest rates have reignited to the down side as the 30-year treasury ended the week at 2.00%. Rates have declined 40bps since mid-September as economic data has become more and more negative. We believe the economy is beginning to crack and see rates continuing to decline through 2019.

Credit spreads widened 3-5bps through the week as a result of declining interest rates. As we enter October, we are emphasizing the general trend that bond market liquidity begins to decline after the thanksgiving holiday. Wall Street is reluctant to take on risk, and money managers will want to lock in their performance and ride into the new year. We see this as a negative for spreads through the remainder of the year, and we believe now is the time to move spread duration out of portfolios. Last week, we sold long end Citi, Starbucks, and hospitality properties and moved into treasuries. We plan to continue to sell down credit through the remainder of the year.

Municipals

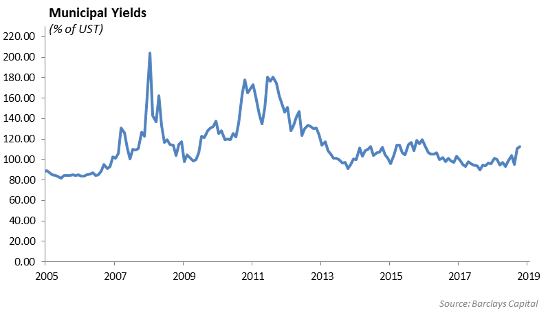

Municipals continue to look attractive after recent underperformance. The 10-year municipal to treasury ratio widened 5bps last week and is quickly approaching parity. We continue to favor municipal new issues, which are providing an average of 10bps of concession over the secondary market. As market volatility increases, we prefer the safe haven of low volatility, high quality municipals at current yields.

High Yield

U.S. high yield credit had a tough week, widening out almost 40 basis points due to global growth concerns and weaker oil prices. The index now sits less than 100 bps tight to year end 2018 levels; however, that number varies widely between the different ratings. BBs and Bs are still 100+ basis points tight, but CCCs are actually 4 basis points wider than year-end levels. It is important to note that those are spread levels, but when talking about outright yield, all risk tiers are still substantially tighter. In regards to total return, the high yield index lost 46 basis points, with the underperformers following the risk tiers. CCCs lost almost 0.9%, Bs lost about 0.7%, while BBs only lost under 0.2%. High yield still has double digit total return in year-to-date basis, but within the past two months, those returns are starting to slip.

Despite poor performance from the asset class as a whole, we did still see slight inflows in high yield mutual funds and ETFs. $198 million went into high yield funds, slightly offsetting the outflows of $258 million from two weeks ago. We continue to see a reversal in flows that seemingly occur every 1 to 2 weeks.

In the new issue market, high credit remained relatively active despite the uptick in volatility. $4 billion worth of high yield credit priced last week. Year-to-date volumes have now crossed the $200 billion mark, up almost 30% from the year prior. Two of the notable transactions were low quality issuers, CCC issuers NFP Corp and Alliant Holdings both priced their 6 year and 8 year notes at the high end of price talk.

Autos such as General Motors and Ford have been rightfully beaten up the past couple of weeks, and Ford received a high yield rating. With this weakness, we added 1% of a GM 2024 bond yielding over 3%. We see this move as a slight up in quality trade compared to the rest of high yield. Additionally, we added an Allegheny Technologies 2021 bond. This short bond carries a single B rating, but we believe the 3.5% yield compensates for the risk to the highly specialized engineered product maker that is entering a deleveraging program.

Europe

Brexit is one of the most significant capital market events of the past 50 years, yet it seems that the capital markets are dismissing the risk as if it will all magically work out fine. However, the instability of the U.K.’s government, combined with a lack of direction and strategy, make it difficult to predict the next turn in the drama. Brexit is scheduled for October 31st, but the U.K. parliament passed a law requiring the government to ask the European Union for a third delay in Brexit if a deal isn’t agreed to by October 19, 2019. Prime Minister Boris Johnson indicated that he refuses to follow the law – this came after he attempted to suspend Parliament for two weeks in October.

The European and U.K. economies are weakening, and Germany is on the brink of a recession. Regardless, it will come to head in October. After three years of wrangling between the U.K. and the E.U., the solution hasn’t presented itself, and it will not magically arrive in a package acceptable to both the U.K. citizens and the government.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.