The Economy

“I don’t pretend to know

The challenges you’re facing

The worlds you keep erasing and creating in your mind”

–Lin Manuel Miranda

We ask ourselves, will it be enough?

- Are the apparent small steps toward resolving the U.S. – China trade dispute enough to diminish the uncertainties that are holding back global economic growth?

- Are the last minute steps by the U.K. parliament and the European Union enough to resolve the complex Brexit process and remove the uncertainties impeding fixed investment in the U.K. and Europe?

- Is the Fed’s initiative to lower short term interest rates over the past six months enough to spur domestic economic growth, sustain a vibrant employment market, and push stock prices higher in 2020?

- Is the initiative by the major global central banks to keep global bond yields at negative levels enough to spur global growth?

With domestic stock prices trading near record high levels and bond yields near historic low levels, the capital markets have appeared to discount optimistic resolutions to tremendously complex issues. In spite of an optimistic announcement last week, we expect progress to be slow on U.S. – China trade issues; and, whatever the resolution, normalized trade between the two largest economies will take several years. At the same time, U.S. – European trade issues remain unresolved.

Last week, Prime Minister Boris Johnson and his Irish counterpart Leo Varadkar released a joint statement that they had “detailed and constructive discussions” and “can see a pathway to a possible deal.” While this appears to address a lynchpin issue around a hard border on Ireland post Brexit, there is still a significant amount of detail for an orderly Brexit.

Given the global economic slowdown and impediments to investment, the risk to financial asset prices is to the downside. Corporate earnings growth is slowing and we expect a challenging third quarter earnings season.

Monetary Policy

The Fed has hinted its concern that weaker business activity and investment could lead to slower hiring and consumer spending. The Fed has been on an accommodative push to lower rates in an effort to mitigate the impact of slowing global growth on the domestic economy. The Fed has signaled that it expects the economy to continue on a path of steady growth with the help of recent interest rate cuts. However, there is growing concern among Fed members around the impact of the trade war and the threat of a drastic Brexit from the European Unions on the global economy. Also, do not ignore the impact of the protests in Hong Kong on China and the region.

As the Fed reduced the size of its balance sheet over the past two years, the reduction in the bond portfolio resulted in a reduction in reserves held at the Fed. The reduction in spare reserves that are used to support inter-bank lending resulted in the instability in repo rates last month. This week, the Fed announced an increase in monthly bond purchases of up to $60 billion per month in an effort to stabilize the short term lending market known as repurchase agreements. By growing the balance sheet, it will only by buying short term Treasury Bills and will not be providing any additional monetary accommodation. The additional liquidity is an effort to provide a backstop to allow the Fed to support repo rates and to maintain interest rates where the Fed intends.

Equities

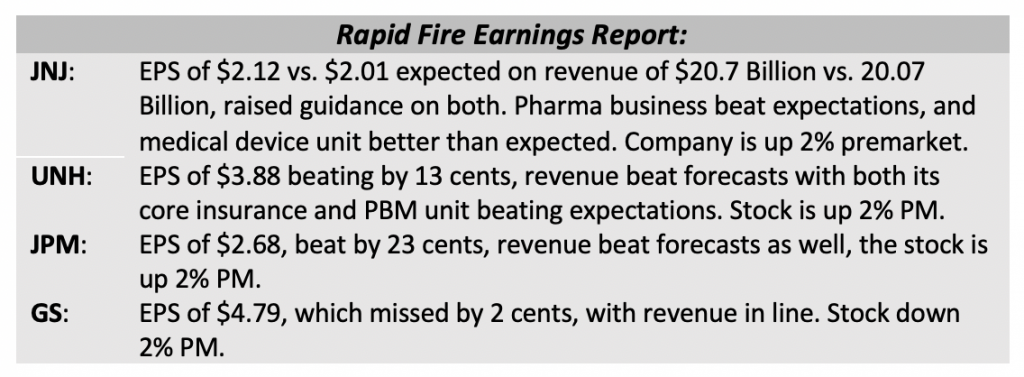

The S&P traded up 1.09% on Friday, and down 0.14% yesterday ending at 2966. It is up 18.3% YTD and 1.9% off of all-time highs. Earnings season gets busy this week with over 50 companies reporting. The Street consensus is expecting 3.6% revenue growth and -2.7% EPS growth in Q3.

Today: Citi, Schwab, Goldman, JNJ, JPM, Morgan Stanley, UNH, Wells Fargo

Tomorrow: BAC, BlackRock, PNC, USB, CSX, IBM, NFLX, PYPL

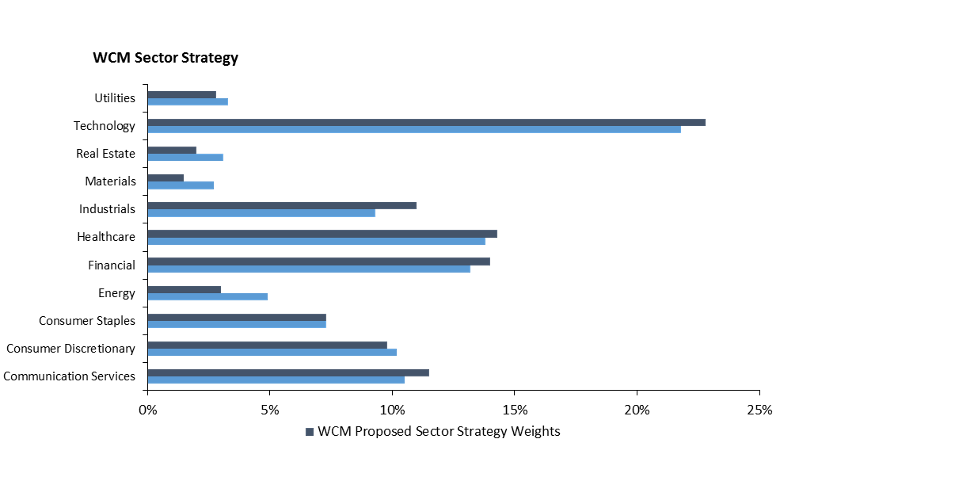

Sector Strategies

Heading into the end of the year, we wanted to highlight some of our sector strategies. These strategies are implemented into our Core Sector series, Large Cap blend model, and Dividend Growth model.

Overweight: Communication Services, Financials, Healthcare, Industrials, Tech

- Financials & Healthcare: We think Financials and Healthcare are very cheap. Using 5 Year averages of price to earnings, Healthcare is trading at a 14% discount, and Financials are trading at a 20% discount. Performance wise, Healthcare is up 3% this year and Financials is up 13% this year vs. the S&P gain of 18%.

- Industrials: There are sleeves that we don’t like, but the sector fund is heavily weighted towards aerospace and defense names, which we believe in, therefore we are OW the sector.

- Tech: We are in the early stages of cloud growth, and we believe 5G is a growth driver for technology as a whole moving forward. With MSFT making up a large percentage of the sector (20%), as our favorite and top holding, we continue to like Tech.

- Communication Services: There are many large names in this space that have seen pullbacks which we like. Facebook, Disney, and Google are all names we are buyers of. Just looking at this sector short term, only 18% of the S&P stocks in this sector are trading above their 20 day moving averages and only 29% are trading above their 50 day moving averages, which puts it at the bottom of every sector.

Neutral: Consumer Discretionary, Consumer Staples

- Consumer Discretionary & Staples: Staples and discretionary sectors have been driven by the strong consumer over the past 2 years. While economic data continues to show strong consumer behavior, we believe this is a lagging indicator. We believe the weak manufacturing data and mass layoffs will lead to less consumer spending over the coming quarters.

Underweight: Energy, Materials, Real Estate and Utilities

- Energy: As the global economy slows, so does the demand for oil. We see no catalysts for energy to outperform in the near term in this environment.

- Uilities & Real Estate: Both utilities and real estate have been strong performers in 2019 as interest rates have declined sharply. This has led to an overvaluation in each sector. Utilities are trading at a higher P/E than tech and communications.

Fixed Income

Risk on was the name of the game across most asset classes last week which resulted in an exodus from the safe haven of US Treasuries. This drove rates higher by over 20bps during the week. The 10-year treasury now trades at 1.72%, but we believe rates will continue their downward momentum unless a more meaningful trade deal is inked. The Fed also announced their intent to begin growing their balance sheet once again as a defense against illiquidity in the repo markets. We see this as a short-term fix that’s primary effect will be to steepen the curve. Ultimately, we believe the fed steps in with a more permanent measure of acting as agent in the repo market over investment banks.

Investment grade spreads tightened as investors were eager to capture credit risk in a higher interest rate environment. Spreads were generally tighter by 5-10bps depending on the sector, in which high beta TMT was the best performing sector. While energy finally saw some tightening, the sector was noticeably lagging the general market.

We took advantage of tighter spreads, and continued to sell down credit in total return portfolios. During the week we sold 30-year Qualcom and Charter and 10-year McDonalds and Coca-Cola. Going into the end of the year, we prefer to be light on credit as we see liquidity declining and volatility increasing.

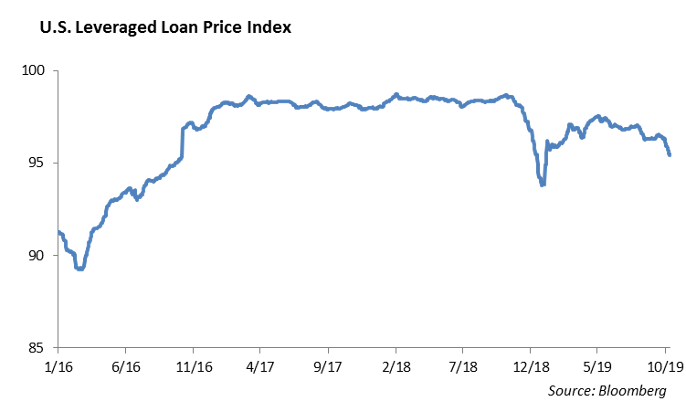

Levered Loans

The levered loan market has continued to show cracks as the S&P Levered Loan index price hit a 10-month low last week and levered loan funds saw their biggest outflow in 7 weeks. CLO’s have also experienced weakness and BBB CLO’s are trading roughly 100bps wider today than this time last year. Issuance remains heavy in levered loans, while covenants continue to decline. Additionally, ratings downgrades are outpacing rating upgrades 3 to 1 in the levered loan market. The floating rate nature of this asset class means it should be outperforming in a rising rate environment. However, a stretch for yield, low covenants, and deteriorating credit are all symptoms of the late stages of the credit cycle. We would caution investors from chasing yield in this sector until covenants and credit quality meaningfully improve.

High Yield

U.S. high yield markets reversed their three weeks straight of spread widening by tightening 28 basis points on improved trade sentiment. Tightening was relatively spread out evenly across the different ratings with BBs tightening 27 bps, Bs 29 bps, and CCCs 23 bps. Year to Date, Bs are now the winner when it comes to spread compression, while BBs maintain their lead when considering total return. BBs are back to year-to-date total return over 13% while Bs have seen almost 11% total return and CCCs trailing at 5.5%.

ETF and mutual funds reversed course once again with $1.5 billion of outflows leaving high yield funds. Wealth managers and individual investors most likely are comfortable de-risking and taking their double digits gains for the year, leaving the street long these securities.

The high yield primary market remained active last week with $3.4 billion pricing. Notable deals included Terraform the BB-/B1 software company pricing 10 year senior notes at good levels of oversubscription, OCI the BB rated chemical company pricing 5 year notes at the low end of price talk, while low quality issuer TruckPro had to shorten their offering while increasing the interest they will have to pay out.

Energy prices rose 4% last week, driven by the U.S./China partial trade agreement and reports of a missile strike on an Iranian oil tanker. Geopolitical risk in the Middle East still seem to be the major driver of short term spikes in crude oil prices. Prices gave back some of their gains yesterday as investors cooled on the optimism on U.S./China trade. Schlumberger reports earnings before the market opens on Friday. While not a high yield name, their earning may provide valuable insight into how the volatile oilfield services industry will have performed in the third quarter.

China

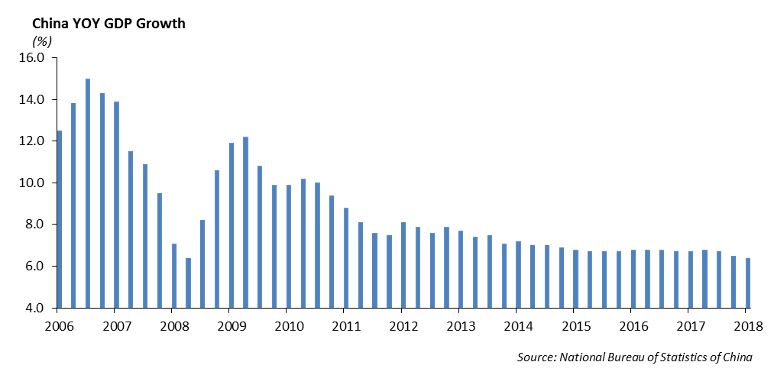

Earlier this month, Xi Jinping, General Secretary of the Communist Party in China, presided over the 70th anniversary celebration of the Communist Party’s rule. In the background the protests in Hong Kong continue to grow and become more violent. First, let’s talk about China’s economy.

In the face of proposed tariffs by the United States and reduced demand, China’s economy is slowing sharply. We expect the government will take a wait-and-see attitude before stepping in to stimulate growth. So far, China’s central bank has remained on the sidelines as other global central banks have lowered interest rates. China has other problems in its economy including rising debt levels and a growing services sector which is putting pressure on its manufacturing base.

We maintain that China has more to lose in the trade war with the United States in terms of economic growth. Over the past five years, China has been intentionally shifting the structure of its economy away from manufacturing, property and investment toward technology and consumption. While the leadership has pledged to not stimulate the property market this year, the central bank did lower the level on a new reference lending rate for businesses. The move toward moderation appears to be an attempt by policy makers to control asset bubbles.

So, why do the protests in Hong Kong matter to China’s economy? Hong Kong rule was transferred from Great Britain over to China in 1997 under a “one country, two systems” political regime. China committed for 50 years it would not alter the political or economic systems of Hong Kong and allow it to operate independently. However, the protests bring attention to China’s growing reach into Hong Kong. At the same time, Hong Kong is an important link between China and the global economy. It is estimated that over $1 trillion in money flows out of China through Hong Kong into the global economy.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.