The Economy

Today is the 90th birthday of “Black Monday” where the Dow Jones Industrial Average declined by 12.8%, followed by another decline of 11.7% the very next day. This sharp decline was the start of the Market Crash of 1929 which lead to the Great Depression in the 1930’s.

Business activity has continued to slow around the world in October, and last week was no exception. Concerns around trade tariffs and Brexit have contributed to a slowdown in business investment and trade as businesses choose to wait out the uncertainty over trade until there is more clarity.

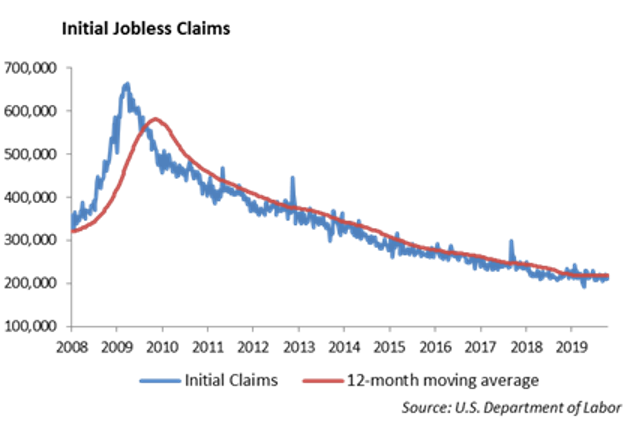

Investors’ attention will be focused on the Federal Reserve’s Open Market Committee this week, in which we expect the Fed to lower the Fed Funds Rate by 25 bps. At the same time, this is a fairly important week for economic data, including a jobs report and ISM data later in the week. We are expecting the economic data to confirm a slowing economy, which will give the Fed cover to lower rates. Non-farm payroll is expected to be below 100,000 this week and likely skewed by the General Motors strike. Still, the twelve month moving average is showing the trend in jobs gains slowing.

While the GM strike and Boeing’s issues with the 737 MAX have been a negative contributor to manufacturing output over the past month, we expect the ISM number to improve slightly from last month. The U.S. Commerce Department reported a decline in durable goods orders last week. At the same time, business activity in Japan and the Eurozone are in stagnation.

Monetary Policy

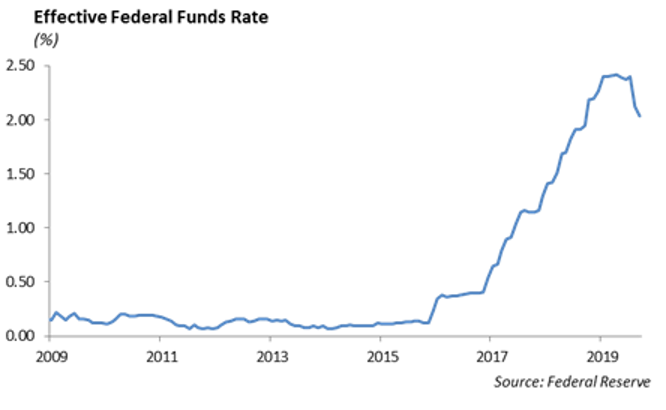

The Fed meets this week, and we expect they will lower the Fed Funds rate another 25 basis points. This will be their third time lowering rates this year, as the Fed attempts to balance monetary policy with a slowing global economic growth. However, unless there is a significant deterioration in the economy heading into the end of the year, we expect the Fed to take a pause in December and shift to language around “data dependent” with respect to future rate moves.

Since mid-September, the Fed has moved aggressively, using its balance sheet to purchase U.S. Treasury Bills to stabilize short term repo rates. The Fed announced last week that it would purchase up to $60 billion a month in U.S. Treasury Bills and credit banks with equal amounts in order to maintain the reserves required for adequate liquidity. The Fed is targeting reserves of roughly $1.5 trillion and needs to purchase roughly $300 billion of short term bills. At that pace, the Fed will own over 10% of the outstanding U.S. T-Bill market.

Equities

The focus was on earnings last week, and as we expected, it was a mixed bag. We expected to see a slowing economy come through earnings and company guidance. Caterpillar, John Deere, Fed Ex, 3M and Ford all missed earnings and guided lower. However, several companies, including Paypal, Microsoft and Honeywell, hit the mark, confirming that they could deliver value to shareholder despite macro-forces impacting revenue and profits. Of the 199 companies that have announced third quarter earnings, 78% have reported above consensus. These better-than-expected results have improved the overall forecast for the quarter to -2% from a -3.2% projection at the start of the earnings season.

- Honeywell International‘s (NYSE:HON) posted solid third quarter earnings and managed to raise its full-year earnings forecast, despite lowering full-year organic sales guidance. HON adjusted EPS came in at $2.08 compared to guidance of $2.00. The company even indicated that they have a backlog in all their major markets, and the results showed Honeywell doing what management said it would do.

- Procter & Gamble Co (NYSE: PG) topped earnings expectations and raised its 2020 guidance. PG shares are up more than 34% so far in 2019 after the company delivered strong first-quarter last week that were well above Wall Street’s expectations. (PG fiscal year end is June 30). P&G’s first-quarter revenue rose 7% year-over-year to $17.8 billion, besting analysts’ estimates for revenue of $17.4 billion. Most encouraging was the strong organic growth the company posted across most of its major business segments. On a companywide basis, P&G’s organic sales rose an impressive 7%, including a 4% rise in volume. Higher prices and favorable product mix contributed to the remainder of the gains.

- Microsoft (MSFT) reported earnings of $1.38 vs $1.25, and revenue of $33.06 billion, which beat the $32.23 billion expected. Revenue increased 14%. Azure cloud business showed 59% growth, which is actually down from the 64% growth last quarter. Personal computing represented $11.13 billion in revenue, which beat estimates. Revenue from Windows commercial products was up 26%, which is up from 12% growth. Microsoft Productivity, which includes Office products, had revenue of $11.08 billion, beating estimates at a 9.5% increase in Office 365 subscribers. The stock ended the day up 2%.

- Amazon (AMZN) fell 9% after earnings. They gave 4th quarter revenue guidance of $80-86 Billion, while the average estimate was $87.5 Billion. Earnings of $4.23 missed by 40 cents, and revenue of $70 billion beat by $1B and grew by 24%. They spent over $800 million in the second quarter to expand its free one-day delivery program, and this will continue for the foreseeable future. Operating income dropped 15% from last year, forecasted to fall between $1.2-2.9 Billion, which missed the $4.2 Billion estimate. Cloud business also missed expectations. Bezos defended the one-day transition, saying it’s the right long-term decision.

- PayPal (PYPL) reported earnings of 61 cents and beat by 9 cents, on revenue of $4.38 Billion, which also beat. Total payment volume was up 25% YoY, beating by $1 Billion at $178.7 Billion. There was a 16% rise in active PayPal accounts, bringing the total to 295 million. Venmo processed $27 Billion. They raised full year revenue outlook. Before the report, the stock had fallen about 20% since last quarter’s earnings. The concerns were implementation delays and the EBAY contract expiration. Expectations for the revenue from eBay now seems to have shrunk, with eBay representing only 8% of their total overall volume. The stock was up 8% on earnings.

One observation from earnings is the success of the healthcare sector. It is the second worst performing sector year to date and lags the market by about 14%. A lot of the underperformance can be attributed to the potential negative earnings growth consequences from Medicare for All and other regulatory propositions, such as drug price disclosures in advertisements. It’s clear that Medicare for All is not widely accepted, and the probability of anything being enacted is extremely low. The political risk within this sector appears to be very overblown. Healthcare is one of 2 sectors with earnings expectations being revised higher over the last few months with attractive valuations. Only one healthcare company out of 23 reports missed expectations, and some major sector constituents increased forward guidance on their earnings calls. We are currently overweight the sector.

Top Movers: Biogen was up 26% after filing a marketing application for its Alzheimer’s drug. Tesla was up 14.4% after posting an unexpected profit for the quarter. Twitter fell 20% on earnings after revenue missed due to advertising problems. Nokia was down 25% after slashing guidance and pausing dividends.

International Equities

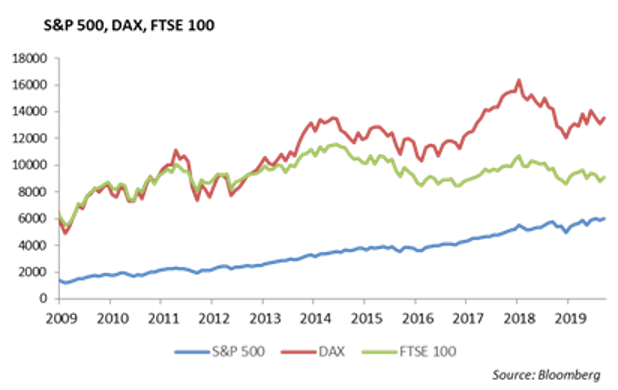

With domestic equity markets up over 20%, it is easy to become complacent in simply owning the S&P 500. Frankly, this strategy would have worked well for investors over the past several years. As we see the US economy slowing and returns challenged in the near term, it is important to look for more opportunities across the globe. This year, developed international is up 16.50% and emerging markets are up only 9.5%. When we look for global opportunities, it ultimately comes down to valuation. While many European indexes have lagged the S&P 500, their valuations have not necessarily become cheap due to an earnings recession across the continent. The German Dax for example trades at a P/E of 22.5 which is a 7 year high. The Euro Stoxx trades at at P/E of 19, which is also not historically cheap. Japan on the other hand trades 16x earnings, which is a 10 year low. The MSCI Emerging Market index currently trades a 14x earnings, which is notably cheaper since 2016 highs but also is not historically cheap. So what’s the point? While international markets have lagged domestic equities, we would love to find an entry point. However, these markets have lagged for a reason, and we do not believe simply in mean reversion. Until valuations compensate us for the risks taken, we will continue to wait for the right opportunity add to international equities.

Fixed Income

Rates were largely unchanged over the week, and traders have now priced a 90% probability of a 25 bps rate cut at the upcoming FOMC meeting. Global rates continue to remain in negative territory; however, the amount outstanding has decreased from $17 billion to $13 billion over the past two months. The global aggregate index has returned 6.5% this year, but now has a yield to worst of 1.40% with a very long duration of 7.18 years. Emerging market bonds have had a very strong year, returning 11.17%, and they currently have a yield to worst of 4.97% with a 6.14 year duration. Despite their outperformance this year, emerging market bonds trade at 209bps wide of the US Corporate index, which is the wide level since 2015. In a world of ever tighten yields, we are looking at adding emerging market bond exposure as a way to pick up incremental yield as they look relatively cheap to US bonds.

Municipal Bonds

Chicago announced a $11.65 billion budget that, on paper, balances the budget and bridges the $838 million funding gap. New revenue is coming from a real estate transfer tax, higher parking taxes, and a cannibas tax matched with a large refinance. There will be no increase to property taxes.

Muni ratio remained attractive as the rate on 30-year munis are near parity to treasuries. We believe the remainder of 2019 Fed cuts have been priced in, and we think munis are attractive at current levels. With munis trading at 2.18%, they currently offer a 3.7% tax equivalent yield to investors hungry for yield in this current environment.

High Yield

U.S. high yield had another good week as the index tightened in 13 basis points. This marks the third consecutive week of spread tightening as investors have continued to shrug off global growth concerns in favor of reaching for more yield. The index is currently 144 basis points tight of year end 2018 levels. For total return, the index saw 28 bps of performance as we got back to the backwards return we saw earlier in the summer. Quality in high yield was the outperformer as BBs and Bs returned over 30 bps, while CCCs trailed at 8 bps of total return.

High yield funds were positive for a second consecutive week, snapping the back and forth pattern we have seen for the past couple of months. $1.2 billion went into high yield funds compared to the $1.8 billion we saw the week prior.

The primary market continues to have strong activity. $7 billion priced, making this year’s issuance 30% greater than the respective period in 2018. Netflix was the notable issuer last week, launching both U.S. dollar and euro denominated 10-year debt to fund new content acquisitions and other general corporate purposes. The deal saw high levels of demand. The USD notes priced at 4.875% inside of initial price talk and immediately tightened over 10 bps on the break to sit on top of prior existing 10-year notes. For lower quality issuers, there were examples of investor pushback on pricing as FXI holding priced at 12.625%, outside of initial price talks.

Energy markets took a reversal as crude oil prices rose 5% while natural gas fell 1%. Oil price rise was due much in part to supply information as there was a surprise draw in U.S. inventories and a decline in U.S. rig count. This news is not all good for energy companies and investors as rig count had their sharpest drop since April, signaling possible trouble in the market.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.