The World

The internet? Is that thing still around? –Homer Simpson

The year 1969 held many major accomplishments for society. The Beatles released the White Album, Neil Armstrong walked on the moon, the Scooby Doo series premiered, and the Boeing 747 flew for the first time. Fifty years ago last week, the world’s first electronic message was sent and received, laying the foundation for the internet. An early packet-switching network known as ARPANET was the first network to implement the TCP/IP protocol suite, which is still used today. Both technologies became part of the foundation of the Internet. The first electronic message ran between two computers and was sent by University of California, Los Angeles (UCLA) Professor Leonard Kleinrock from the campus to Bill Duvall, a computer programmer sitting in the Stanford Research Institute. The message was supposed to contain the word “login,” but the system crashed after “lo.”

Fifty years later, the internet has profoundly impacted society. With elections coming up this week, political advertising on social media is a debate on center stage; Twitter announced last week that they will prohibit political advertising altogether.

Corporate earnings, Fed policy, and the economy are the key factors driving the financial markets. Although expectations were lower, corporate earnings continue to come in stronger than we expected. According to Factset, roughly 75% of the 342 companies in the S&P 500 that posted results through last Thursday morning have beat expectations.

October 31st was the deadline for Brexit, and it sort of feels like Y2K. Prime Minister Boris Johnson’s promise to have the UK leave the European Union by October 31st was a major issue for his election. However, his pledge to leave by October 31st with or without a deal was blocked by Parliament, forcing him to seek an extension until January 31, 2020. Last week, the U.K. Parliament passed legislation, calling for an early general election on December 12th. This will prove to be a test for Johnson’s Conservative Party and its ability to put a coalition together that is effective enough to get Brexit accomplished.

The Economy

The U.S. economy continued to grow, albeit at a much slower pace, in the third quarter. Gross Domestic Product grew by 1.9% for the quarter, according to the Commerce Department, compared with 2.0% growth in the prior quarter. Our expectation for domestic economic growth is modestly higher for 2020, assuming we get past the trade wars and Brexit.

The report from the Commerce Department showed that consumer spending increased by 2.9% annual rate, which is significantly lower than the 4.6% increase from the prior quarter. The consumer, which represents roughly 70% of the economy, continued to spend on big ticket items, such as cars and appliances during the quarter.

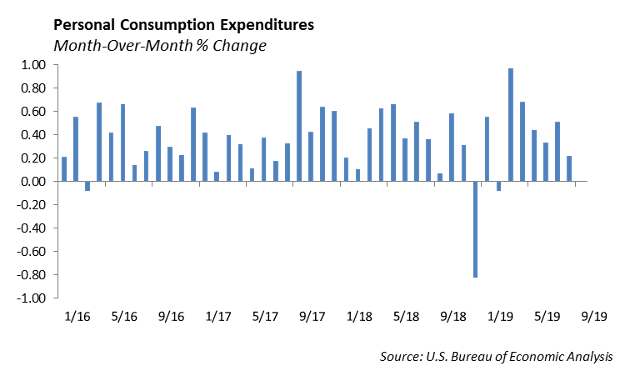

The household sector remains healthy with the unemployment rate at 3.6%, which is near fifty year lows, and wage growth is picking up as well. Employment grew by 128,000 jobs in October, which was higher than we expected given the GM Strike and reduction in the federal workforce. Consumer sentiment has remained strong in recent months. Personal consumption expenditures increased 0.2% in September on a seasonally adjusted basis. This further confirms that consumers are helping to lift the economy, in the face of slowing in the manufacturing sector.

At the same time, business investment fell by 3.0% in the quarter. The U.S. – China trade war has had a muting impact on business investment.

Monetary Policy

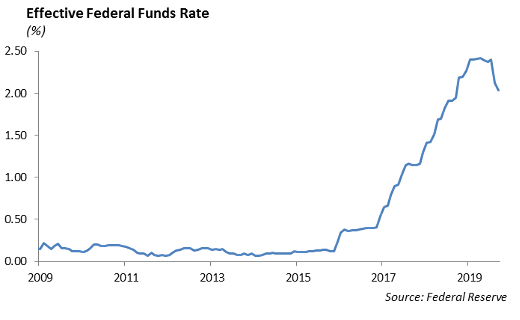

The Federal Reserve lowered short term interest rates again by 25 bps, the third move since July. As a result of this move, the Fed lowered the target range for the Federal Funds Rate to 1-1/2 to 1-3/4 percent. The Fed acknowledged that a sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective are the most likely outcomes, but uncertainties about trade and the global economic slowdown remain.

Unless economic growth slows significantly, we expect the Fed will most likely pause its recent lowering of short term rates and review future policy changes relative to changes in economic data.

Equities

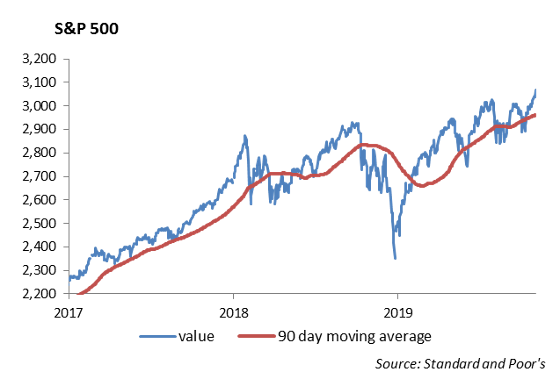

For the week, the S&P rose another 1.5%, ending Friday at all-time highs of 3067. A lot of the gains came on Friday as the S&P rose over 1% on a strong jobs reports. Earnings have been dominating the news flow and have continued to report much better than expected. Of the 356 S&P companies that have announced 3Q earnings so far, 76% have come in above consensus. The 3Q forecast has improved from -3.2% at the start of the earnings season to -0.8%. Of the stocks that have been reported, the average stock has gained 0.64% on its earnings reaction day, which is improved from negative one-day price reactions from the last 2 earnings seasons.

On a sector basis, the worst sectors are materials with earnings down 32%, and energy, with earnings down 11%.

For tech, the share weighted change in earnings is a decline of 6.5%. Software earnings are positive, but not enough to offset negative earnings from semiconductors. The market cap weighted change for tech in earnings is actually at a 5% gain, highlighting that large cap companies are navigating the trade war better than small and mid-cap. Every other sector is higher with Staples up 6%, Health care up 7.5%, and Communications up 9.5%.

- Facebook (FB): beat on earnings and revenue. Daily active users of 1.62 billion beat expectations, while monthly active users met expectations. Revenue was up 29%. Mobile ad revenue accounts for 94% of total ad sales, up from 92%, and average revenue per user increased 19% to $7.26. They warned of slower revenue growth in the fourth quarter, but the stock still rose 4%. FB is up 47% YTD. It is at $194, which is not too far off all-time highs of $208.

- Apple (AAPL) beat expectations on earnings and revenue. Revenue was $64 billion which beat by $1 billion. EPS was 3.03 which beat by 19 cents. There was 18% growth in Apple’s services businesses, and 54% growth in wearables including AirPods. The iPhone business beat expectations but was down 9% YoY, but they said they expected a big holiday quarter. This is also an improvement from the 15% drop in iPhone revenue over previous quarters. Guidance remained in line for the quarter, which would give the beat growth over last year’s holiday quarter and post a record in revenue that it reached in 2017. Apple is currently at all-time highs trading at $256/share.

International Equity

While data out of the US looked stronger than expected last week, the global economy is still weakening. Euro manufacturing confidence levels continue to show a contraction, and the Japanese industrial production levels came in lower than expected. Not surprisingly, when we look at the data out of the UK, all indicators point to a real economic contraction. For example, the earnings season in Europe is showing a much worse picture than the earnings declaration in the US. Earnings growth is -4.9% and sales growth is flat year over year. Furthermore, the number of earnings surprises is at -2.1%. All of these indicators point us to the same conclusion – it is still too soon to add to international equities.

Fixed Income

Unsurprisingly, the Fed lowered short term rates by another 25 bps this past week, placing the Fed funds rate in a range of 1.50% to 1.75%. Rates generally declined through the week, despite strong economic data, and the 10-year ended the week at 1.71%.

Credit markets continued to grind tighter over the week, and the index moved towards its lows of 110 OAS. Much of this tightening can be attributed to strong economic data, matched with stronger than expected corporate earnings domestically. While we have been generally reducing credit in fixed income strategies, we’ve also been very active in the new issue calendar. As companies are increasingly refinancing their debt with interest rates remaining relatively low, new issue concessions have been meaningful at 5-10 bps.

Municipal Bonds

Municipals followed the lead of corporate bonds over the past week, outperforming treasuries by 3 bps. The muni curve has steepened over the past month as new issuance has begun to pick up. Municipals tend to perform well going into year-end as investors position their portfolio for the upcoming tax season. The issuance calendar is expected to remain heavy going into the holiday season, and we believe this is where value can be found in the municipal market as concessions have been 10-20 bps over secondary offerings.

High Yield

Junk credit had a tough week last week, with spreads widening out about 20 bps. This breaks the streak of three straight weeks of spread compression on improved investor sentiment. Total return was also negative across the ratings, with the riskier tiers leading the way. CCCs lost over 50 bps of total return, Bs lost under 20 bps, and BBs lost a muted 4 bps. Year-to-date, total return for the high-yield credit index dipped under 12%, which also trails investment grade credit total return of 13.45%. Outperformance in the investment grade credit index can be attributed to the longer duration that IG credits have in a lowering interest rate environment.

Despite the negative performance, fund flows were positive for a third consecutive week. $940 million came into high yield ETFs and mutual funds. Inflows have been slowing down from the past two weeks prior. Funds flows should further slowdown as we get closer to the holiday season and year end.

Although it doesn’t really seem like it, high yield actually experienced a considerable new issuance slowdown in October. $19 billion of new volume pricing on 31 deals marks the 4th slowest month of the year. The issuance that in October was dominated by well-known, high quality BB issuers, which made the primary market seem more active than it really was. BBs accounted for 43% of issuance. Issuance last week was pretty quiet with volatility and the Fed meeting. The lone notable issuer was Transdigm. The highly specialized aerospace manufacturing company issued B- rated senior subordinated debt. Pricing came in line with initial price talks, but was upsized by $500 million, showing reasonably healthy demand for high yield new issuance.

In the energy markets, much of the week was characterized by weaker prices. The softening market was due in part to skepticism by Chinese officials on the viability of a long term U.S. deal and an unexpected crude build in the United States. There was a dramatic reversal on Friday, where much of the week’s losses were offset on declining U.S. rig count and bullish Chinese manufacturing data.

In other energy news, Saudi Aramco announced that it will go forward with the IPO process. The prospectus is expected to be filed on November 9th. Reports show that the Kingdom would accept a $1.6-1.8 trillion valuation.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.