Over the past several weeks, there has been movement on both Brexit and the resolution of U.S. – China trade dispute. These have been two major structural impediments to global growth. We are changing our base case outlook to consider the resolution of trade issues in the 1Q 2020 as well as Brexit. This is not meant as endorsement on a positive outcome for either. But, rather the belief that resolving these barriers will lead to fixed investment, consumption and economic growth.

- We are expecting domestic economic growth between 1.8% and 2.0% for 2019. However, massive global central bank stimulus, lower interest rates along with progress on Brexit and U.S. – China Trade issues are enough for us to revise our outlook upward for global growth in 2020. While the current slow growth environment will help keep interest rates low, we may begin to see rates bottom as expectations for growth increase.

- Global central banks have shifted to a more accommodative tone during the past year. This year’s shift toward monetary stimulus is in contrast to 2018 in which the Federal Reserve was pushing interest rates higher and the ECB had ended its Quantitative Easing program. A more stimulate monetary policy will serve as a catalyst for global growth.

- Corporate earnings are coming in stronger than we expected; however, earnings growth will remain under pressure as revenue growth slows and profit margins are pressured over the near term. We still expect labor costs to be scrutinized in the fourth quarter and expecting an increase in lay-offs to support operating margins. The rosy employment market, which has been the strength in the recovery, will likely deteriorate by the end of the year.

- The trade war with China has contributed to the slowing domestic economic growth rate. We expect that Trump wants a trade deal nailed down with China heading into his re-election campaign in 2020. Recently, President Trump and Chinese President Xi Jinping agreed to renewed trade talks, however, it is not clear how substantive these talks are. Discussions include lowering U.S. hostile initiatives toward Huawei and a commitment from China to buy large amounts of American agriculture products. Our base case is that a resolution to U.S. – China trade dispute will result in increased fixed investment and provide stimulus to global economic growth.

- Boris Johnson has a deal with the European Union for the United Kingdom to exit the E.U. The next step is to get it through the U.K. parliament. The deal includes Northern Ireland remaining part of the U.K. customs union which would allow seamless trading to remain with Ireland. As Lloyd Christmas once said, “so, you’re saying there’s a chance.”

- Liquidity in the credit markets has been difficult at times over the past year. After a surge in new issues, we expect new issue volume to decline significantly heading into the year end. At this point, we do not see a significant shift in the credit cycle; however, the seeds are planted for some deterioration in credit. Leveraged loans and commercial real estate are both drawing significant capital, and valuations appear excessive.

Monetary Policy

The Fed has hinted its concern that weaker business activity and investment could lead to slower hiring and consumer spending. The Fed has been on an accommodative push to lower rates in an effort to mitigate the impact of slowing global growth on the domestic economy. The Fed has signaled that it expects the economy to continue on a path of steady growth with the help of recent interest rate cuts. However, there is growing concern among Fed members around the impact of the trade war and the threat of a drastic Brexit from the European Unions on the global economy. Also, do not ignore the impact of the protests in Hong Kong on China and the region.

As the Fed reduced the size of its balance sheet over the past two years, the reduction in the bond portfolio resulted in a reduction in reserves held at the Fed. The reduction in spare reserves that are used to support inter-bank lending resulted in the instability in repo rates last month. This week, the Fed announced an increase in monthly bond purchases of up to $60 billion per month in an effort to stabilize the short term lending market known as repurchase agreements. By growing the balance sheet, it will only by buying short term Treasury Bills and will not be providing any additional monetary accommodation. The additional liquidity is an effort to provide a backstop to allow the Fed to support repo rates and to maintain interest rates where the Fed intends.

Equity

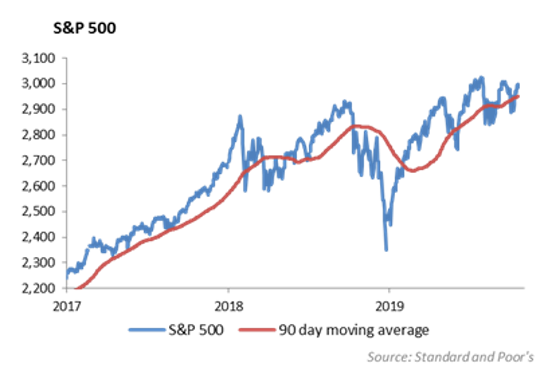

The S&P rose 0.54% over the last week, ending at 2986. YTD it is up 19.12%. The index is above its 20, 50, and 200 day moving average and its October low is the highest low over the last 4 months. For the month, sector performance has been somewhat divided, with Energy, Utilities and Materials as the biggest losers, and Tech and Communications as the winners. Small Cap is up 15.5% YTD and Mid Cap is up 17.8% YTD. They are underperforming large cap by 4% and 1.5% respectively. International is up 14.11%, which is lagging the S&P by 5%, and emerging markets are only up 10% YTD and lagging the S&P by 9%.

Third quarter earnings season so far is mostly positive, with healthcare and financials earnings helping performance early on in the week. 84% S&P companies that have reported thus far have beaten consensus.

- NFLX – Earnings of $1.47 vs $1.04 expected, revenue of $5.24 Billion which was in line. Domestic paid subscriber additions missed by about 300k. International paid subscriber additions beat by 200k. NFLX had 6.8 million net subscriber adds total, but for the year NFLX is set to add 26.7 million new members, which is less than the 28.6 million last year. US Subscriber growth has slowed with just 2.1 million American subs vs 4.1 million last year. There have been large amounts of cancellations with the price hike to $13, making their ability to raise prices limited, which is not good for growth. Initially the stock jumped 10% but it did give back most of those gains over the next few days.

- IBM -EPS of $2.68 vs 2.67 expected, revenue of 18.03 B was down 4% and missed by 200 million. That is a revenue decline for 5 straight quarters now. Global Tech Services, their biggest segment, was down 5.6%. Cloud Unit including Red Hat was up 6.4% but missed expectations. Red Hat revenue grew 19% in the quarter, which was up from 15%. IBM lowered their FY earnings estimate. The stock is down 5%, but it has had a nice year so far, rising 25%.

For the upcoming week, key earnings are Lockheed, McDonalds, UPS, Chipotle, and Texas Instruments on Tuesday. AT&T, Lilly, Ford, Microsoft report on Wednesday. Heavy week in general with over 100 earnings scheduled for the week.

Fixed Income

Rate markets were little changed over the week as investors were digesting an early stage trade deal, an upcoming Brexit vote, and an overall general lack of economic data releases. The 10-year yield was down 1bp to end the week at 1.74%. The first real sign of cracks in the consumer were shown with weak retail sales data on Thursday which pull rates down from the week’s high. We continue to believe the Fed will cut short term rates one more time this year as a control against a weak stock market.

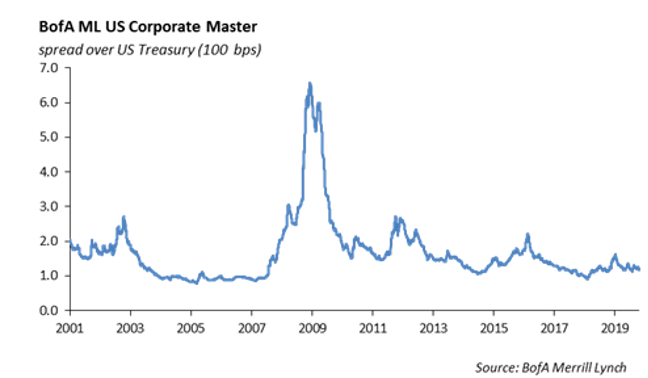

Earnings were plentiful and new issuance was non-exist over the past week. Bank earnings looked particularly strong against low expectation. We continued to see spreads tighten and the Corporate Index OAS is now at 120bps. We used this tightening as an opportunity to continue our reduction of credit going into year end. We sold 10-year Walmart, HSBC, Netflix, and Hospitality Properties over the week and purchases duration neutral treasuries on the other side. We do still like credit on the short end of the curve and are effectively running portfolios with a credit barbell, owning BBB credit inside of 3 years and high quality on the long end of the curve.

Municipal Bonds

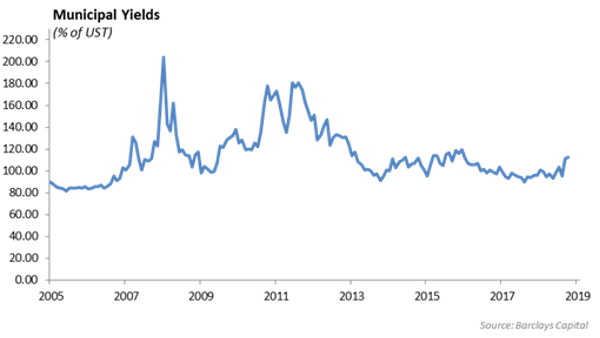

Municipal issuance has been strong the past two weeks and we expect this to continue going into November as rates remain relatively low. Muni’s have performed well in October after trading in parity with treasuries. The 30-year muni/treasury yield ratio now stands at 95% which is fair value. We still like the long end of the muni curve given the 100bps of steepness from 2’s to 10’s.

High Yield

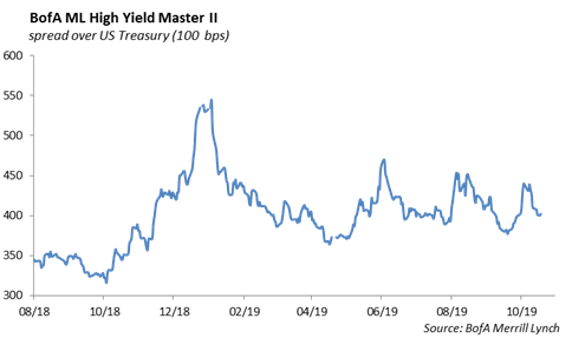

U.S. high yield marked the second week of spread tightening as the index fell 8 bps to an overall option adjusted spread of 402 bps. A good start to the earnings season and preliminary deal on Brexit were enough to encourage investment in high yield and shrug off global growth concerns. The index is 134 bps tight of year end 2018 levels. Spread tightening followed the risk tiers as CCCs led the way with 17 bps of compression, Bs had 9 bps, and BBs held up the rear at 7 bps of tightening. BBs still lead the way of year-to-date total return, making 13.18% in 2019. High yield performance has been an encouraging deviation from a year ago, as October 2018 saw the beginning of massive spread widening in high yield that ended up around 200 basis points for the whole fourth quarter 2018. As liquidity dries up in November and December, it will be interesting to see how the market compares to a year ago.

Fund flows have now had their fourth consecutive week of reversals. This reversal was sharp as $1.8 billion came in, in contrast to the $1.5 billion that flew out the week prior.

The high yield primary market kept consistent with $3 billion pricing. Notable issues were TMT companies as Charter followed their investment grade offering with a high yield tap of their senior unsecured 2030 notes, and VodafoneZiggo refinanced existing debt with $500 million of secured 10 year notes. It seems there is a potential offering coming from Netflix this week or next, this will be something to watch for as Netflix offerings are usually quite well attended, and will be a good barometer of high yield new issuance demand.

In energy markets, WTI and Brent crude oil both fell 2% while natural gas rose 5%. Oil prices falling were due to weak demand data out of China, weak U.S. manufacturing data, and a very large inventory build that toppled expectations by over 3.5 times. Inventories are now 4% year over year and 2% above the five-year average.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.