Investment Themes For 2020

As we look to next year, we have begun to lay out our major investment themes. These themes provide a back drop for our portfolio structure and, in many cases, will impact valuations.

The Economy

We expect economic growth to be muted next year as the Consumer sector slows and manufacturing stabilizes. Bright spots exist in defense and technology. However, growth in the auto and housing sectors will likely remain slow.

Lack of Political Will to Address the Huge Federal Budget Deficit

This fiscal year’s budget deficit is near an astounding $950 billion. During an economic expansion, to run a deficit of that magnitude is reckless. We would expect the economy to slow at some point over the next two years, and the size of the deficit will likely grow. There is no political will to address the entitlement programs which have become a disproportionate size of the budget.

Global Trade and the Impact on Global Economic Growth

We expect a Phase One deal between the U.S. and China which will lead to lowering tariffs on goods coming from China and the purchase of U.S. agricultural products by China. However, we do not expect any progress beyond Phase One heading into the election. We expect a revival in global growth; however, growth will be muted compared to historic measures.

The Independence of the Federal Reserve and its Impact on Monetary Policy

After a three year push to tighten monetary policy by increasing the Fed Funds rate, we expect the Federal Reserve to pause its tightening program during the first part of 2020. A revival in global growth will be enough for the Fed to pause. However, leading up to the election, the President will likely be vocal about the Fed easing policy and lowering rates. In an effort to not be viewed as biased ahead of the election, the Fed will not make major policy moves unless warranted by the data. The independence of the Federal Reserve will be a theme next year.

The Elections Next November

Given the agendas on both sides of the aisle, the elections in November will have an impact on the capital markets. Democrats have political agendas that will impact corporate profits, and Republicans have an agenda that is heavy on U.S. fairness in global trade. In addition, maintaining a majority in the Senate will be a huge focus for the Republican Party.

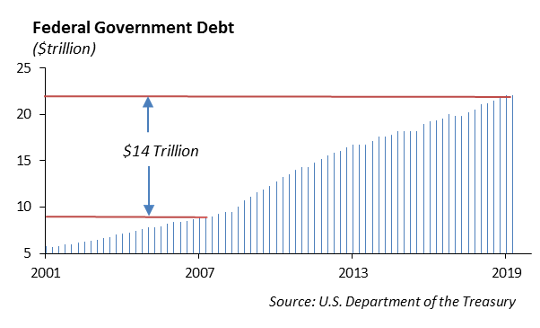

The Growing Debt Supporting Economic Growth

The chronic budget deficits since the Financial Crisis in 2008 have been financed through large debt issuance by the U.S. Treasury. We expect the debt issuance to continue to grow. As the average maturity of Treasury issuance increases, the durations of ETFs that are based on debt outstanding will also increase. Exposure to interest rate risk for investors increases as the U.S. Treasury and corporations term out their debt.

The Consumer Sector

The consumer represents nearly 70% of economic output in the U.S. economy. As a result, the health of the consumer will be important to sustained economic growth next year. While wage growth and disposable income numbers appear favorable, the growth in consumer debt is a concern.

Income Inequality

There has been a significant dispersion in income levels in the U.S., and we expect this will affect tax policy and corporate governance. Increasing taxes for the ultra-wealthy will likely be an issue heading into the election.

The Healthcare System and Rising Healthcare Costs

The U.S. healthcare system is one of the most complex in the world. The chorus calling to address the hidden costs and preference payments imbedded in the healthcare system will increase over the next year.

The Shape of Capitalism.

Our country was founded on principles of democracy and capitalism. Capitalism, solely for the benefit of shareholders, will be challenged over the next few years. We expect more conversation around what role capitalism plays in our society and what role, if any, government will play in a capitalist society.

“Zombie Companies”

Zombie companies are indebted businesses that haven’t made a profit and require additional capital to fund their operations. Roughly 25% of the companies in the Russel 2000 are not producing positive cash flow. The bull market in stocks has been tolerant of private companies that have launched into the public markets having never turned a profit. This includes Uber, Lyft, Pinterest, and Peloton.

Lower expected returns on financial assets

With the rally in domestic stocks, valuations are near the high end. Our outlook for returns for domestic equity are mid-single digits. This will have a major impact on the return assumptions for pension funds over the next several years. It will also have an impact on individuals saving for retirement.

Monetary Policy

The Federal Reserve Chairman Jerome Powell testified before Congress last week and confirmed that the economy is growing and the need for further monetary stimulus may not be warranted in the current environment. Powell was upbeat about the state of the economy; however, he gave mention to global risks, including trade issues with China and Brexit that could upend the economic growth path. We expect the Fed to remain on hold at its December meeting.

In President Nixon’s administration, Fed Chairman Arthur Burns often sat in on his cabinet meetings. Afterwards, Congress made a push for an independent Federal Reserve that would not be influenced by a sitting President. President Trump is essentially calling for more input into Fed policy through his Twitter account. While we do not expect the issue of an independent Federal Reserve to change, we do expect the independence of the Federal Reserve to be an issue next year.

Fixed Income

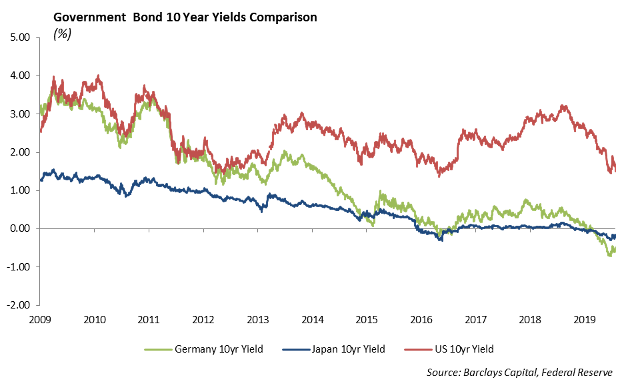

Fixed income markets continue to be driven by the back and forth in the US-China trade deal. This past week, a slight increase in pessimism meant that rates continued their move downward. The 10-year US treasury declined 10bps to end the week at 1.83%. Treasury curves generally steepened towards the widest levels of the year. Global rates continue to be in negative territory, but relative to US treasury, they have become significantly cheaper over the past several weeks. Over the past 5 years, the US 10-year has had a median spread over the equivalent German Bund of 200bps. After reaching a wide of 270bps in 2018, they now trade with a 210bps differential, nearing fair value on a relative basis. We still believe low rates, heightened rate volatility, and a tendency of money managers to lock in year-end gains will continue to drive performance in US treasuries over other asset classes going into year end.

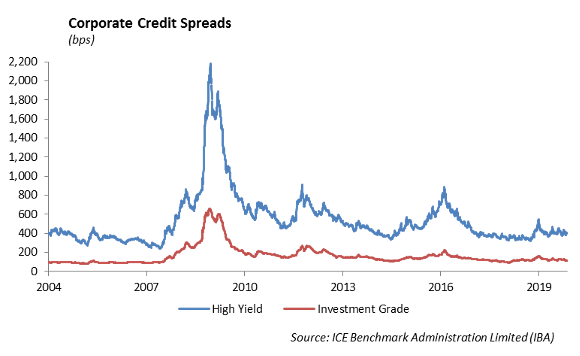

Corporate spreads continue to perform well, and with the corporate index trading at a 106 OAS, spreads are now at twelve-month tights. As spreads generally tighten and overall volatility has declined, investment grade spreads have uncharacteristically outperformed high yield and the levered loan market. Year to date, the investment grade credit index is up 12.75% versus 11.81% for the high yield index and 8.55% for levered loans. We believe this outperformance is driven by investors need for yield with a reluctance to take on substantial credit risk as we see signs of a late stage of this credit cycle. We continue to play defense by positioning portfolios with a neutral credit exposure relative to their benchmark.

High Yield

U.S. high yield saw a week of spread widening due in part to increased new issuance. The index widened out 6 bps and saw negative total return performance of -0.07%. The negative performance was carried wholly by the CCC tier, which saw almost 1% drop in total return. Single and double Bs were modestly higher on a total return basis throughout the week. The disparity in returns may be caused by investors de-risking their portfolio as we head into the end of the year, while still keeping the added yield that higher quality junk credit provides.

There was very little activity in HY fund flows last week. $254 million dollars came out of high yield ETFs and mutual funds, adding to the belief that investors are slowing down their trading activity as we approach year end. Expect flows to remain relatively subdued, probably favoring outflows in the next coming weeks.

About $10.5 billion dollars of new deals came to the high yield primary market last year. Single-B credits mostly dominated the space, with notable issuers as Hertz and Restaurant Brands seeing a healthy 3-4x oversubscription. This week should see higher quality issuers come to market, as crossover credit Centene announced a $7 billion offering to fund their Wellcare acquisition. The Israeli-American pharmaceutical company Teva is also planning an offering this week with expected size of $1.5 billion.

Even with the recent widening in high yield, spreads in the space remain unattractive to enter on a broad basis. There is a recognized need for yield for credit investors in this low interest rate environment, but investors should pick their spots. If investors must get in the space, new issuance is probably the best bet. Pricing has offered little concession to existing companies’ credit curves, but demand has remained high and spreads have generally tightened off the break. Investors could also look at companies that have recently fallen from the investment grade status. An example is Newell Brands, their downgrade by S&P caused forced selling from investment grade investors that has kept spreads out farther than their credit metrics suggest.

In 2020, keep an eye on how successful deleveraging programs are. At this point, a lot of high yield companies have begun prioritizing debt reduction with varying degrees of success. Energy is struggling the most predominately, with lowering demand and a higher amount of maintenance capex. Newell Brands was the victim of an unsuccessful debt reduction initiative, as the main reason for S&P’s downgrade was the failure to divest assets, which would allow them to deleverage the balance sheet.

To touch quickly on energy markets, crude oil was up roughly 1% while natural gas fell 4%. Prices fluctuated throughout the week on updates of a U.S.-China trade deal. There is an upcoming OPEC meeting on December 5th, where announcements should be made on whether cuts will continue through 2020. To the downside, U.S. crude inventories were higher than expected.

Equities

Stocks rose on Friday for the 6th straight day of gains, maintaining their momentum in the 4th quarter. The DOW, the NASDAQ, and the S&P all ended at record highs. Year to date gains are now 20.1% for the DOW, 28.7% for the NASDAQ, and 24.5% for the S&P 500. We are looking for more record today, with the stock futures suggesting gains of .2% at the open.

461 S&P Companies have reported 3Q results, and earnings for the quarter are expected at a 0.4% decline. 74% have beat earnings expectations. For 2019 as a whole, the estimate stands at 1.3% earnings growth. Per sector, Healthcare has the highest growth at a reported 9.4% growth. 85% of companies have beat EPS estimates, and the magnitude of the beats has been 6.7% on average. However, the standout sector YTD is still Technology, which is up 40% and outpacing all other sectors by at least 10%. The sector had the strongest aggregate beats of any sector at 7.5%.

Strong retail sales for the month were reported on Friday, posting a .3% rise versus a .2% rise. Further optimism for the consumer continues to help the rally. Walmart’s 3Q results were better than expected. Walmart reported earnings of $1.16, a beat by 7 cents, and comp sales in the U.S. increased by 3.2% in the third quarter. Transactions rose 1.3%, with ticket price up 1.9%. Total sales rose 2.5% to $128 Billion, which were in line with expectations. Sam’s club sales were up 0.6%. E-commerce was up 41% during the quarter, with help from the grocery business. They slightly increased FY20 adjusted EPS. The stock is up 30% YTD.

Upcoming earnings for this week are mostly Discretionary, with Home Depot, Kohl’s, TJX, Lowe’s, Target, Macy’s, Nordstrom, and Gap reporting.

Year to date developed international is up over 15%, and emerging markets are up almost 10%, a significant laggard to the S&P 500. These markets have rightfully lagged due to negative earnings growth and a lack of revenue growth. Over the past month, fund flows have increased into emerging market funds. One of the primary drives of these flows is the recent weakness in the dollar. With the dollar off 2.5%, the cost of servicing debt for emerging markets has begun to cheapen, which should drive performance. If we get any meaningful resolution to the trade deal, we should see a further increase of capital flows into emerging markets, leading to outperformance.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.