Navigating the Coronavirus

To better understand the impact of the coronavirus, we separate its impact on the economy, the financial system and the capital markets. We do not expect an immediate rebound in economic activity until COVID-19 testing is easily accessible and there is a reliable way to control the spread of the virus, which could include a vaccine. Here is a summary of where we are this week:

The Economy

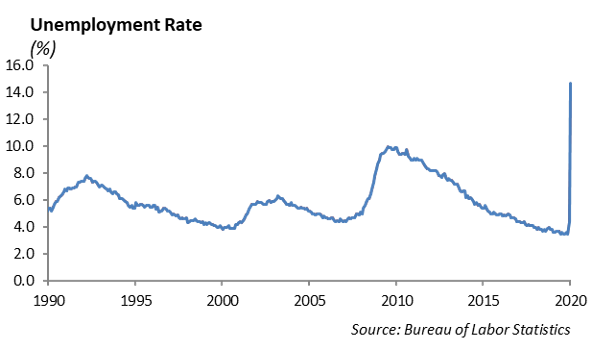

- The rate of unemployment spiked to 14.7% in the month of April as payrolls dropped by an historic 20.5 million workers due to the coronavirus pandemic. During the Financial Crisis, the economy lost eight million jobs and it took nearly eight years to recover. This is the worst monthly jobs report recorded since 1939.

- We expect an economic recovery to be relatively long and muted as the labor force rationalizes low paying transitional work force. Following the Financial Crisis, we experienced a spike in student loan debt as young workers went back to school. We are not yet convinced this is an option as universities have yet to describe plans for the fall semester to protect students and faculty.

- The staged reopening of local businesses does not lay a foundation for an acceleration in business activity. We are not expecting a significant bump in economic activity through the summer.

The Financial System

- With over 8% Tier one capital, the banking system came into this crisis in a much stronger position than during the Financial Crisis in 2008.

- Following the Financial Crisis, we came into this crisis on the tail-end of a significant experiment in monetary policy. This experiment included the initiative of the Federal Reserve to purchase over $4 trillion in bonds in the open market as a means to push interest rates lower across the yield curve and jump start economic growth.

- We are expanding this great experiment with the Federal Reserve initiating this week the purchase of corporate bonds. The hope is that the Fed purchase program will provide liquidity and support to orderly credit markets, helping reduce the risk of a liquidity squeeze or credit crunch in the bond market and jump start economic growth.

- The Federal Reserve moved quickly to push money into the system. The Fed’s measure for monetary aggregates, M2 (which includes all paper currency and coins, time deposits and money market funds) has grown by 35% over the past three months.

- The International Monetary Fund estimates that over 14 trillion dollars of stimulus will soon be in the global economy as a result of the coronavirus.

Seeds to the Next Financial Crisis are Being Planted

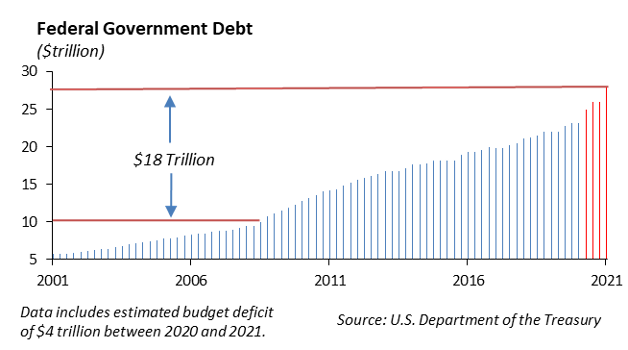

The government moved swiftly to help diminish the impact of the coronavirus on the economy. In all, the federal government has spent close to $4 trillion in program assistance, direct giveaways and loans. This is roughly the amount in today’s dollars that the United States spent on World War II. However, the spending programs have consequences and we expect the actions taken will have repercussions.

- Continued credit deterioration in investment grade and high yield issuers. The investment grade bond market has become a means for established companies to refinance and term out existing debt. With U.S. Treasury rates below one percent, gradations of spreads between credit quality become less meaningful for companies that are able to lower their cost of capital regardless of the rating.

- General Obligation and essential service revenue municipal bonds historically are some of the most secure for investors. However, other types of municipal bonds, including municipalities that support arena and convention center bonds, economic development bonds, and universities will be challenged during the recovery. Higher education may be forced to re-evaluate their model of charging high rates of tuition to support expensive infrastructure supported by student loans.

- The domestic labor market will likely be impaired for several years as positions for furloughed workers are permanently eliminated. We have moved from the best labor market in 50 years and ten years of job gains to a record 14.7% unemployment rate and the loss of over 20 million jobs in the month of April. We expect the travel and leisure sectors to take several years to fully recover.

- It is estimated that 30% of the domestic labor force lives paycheck-to-paycheck. This includes service sector workers which are the hardest hit in this downturn. Income inequality and our ability to provide support to lower income workers will be a growing challenge over the next decade.

- In order to fund the massive economic stimulus programs, we are running a budget deficit of nearly $4 trillion. That deficit is funded through the issuance of Federal debt. The level of federal debt is expected to increase by over $4 trillion over the next two years. While the growth in federal debt is not a sin, the large debt burden ultimately will hamstring the country when it comes to the next crisis that requires stimulus. We are emptying the tank.

- Our biggest concern for investors is Europe. The European Union is a cooperative of 27 member countries with each having their own political system, taxing authority, fiscal budget and debt issuance. However, they share a common currency, the euro. The problem the EU has is that the European buying of sovereign bonds is not proportional. In effect, the EU is subsidizing countries like Italy that have consistently run huge deficits to fund their government.

Last week, Germany’s high court Karlsruhe, Baden-Württemberg, quietly ruled that, by purchasing more than €2.2 trillion (£1.8 trillion) of government bonds since 2015, the European Central Bank has “manifestly” flouted European Union treaty. Germany wants the bond buying to be proportional and does not want to be in a position to fund the ECB’s purchase of the debt of weaker EU countries. French president Emmanuel Macron recently fired a warning shot saying that without making all EU countries mutually responsible for the debts of individual countries, the EU could collapse.

The EU does not have Euro denominated debt. However, the ECB has asked Eurozone finance ministers to consider a one-off joint debt issuance of “corona bonds” to assist with the coronavirus pandemic. This has been met with opposition by Germany and other northern European countries since they do not want to be responsible for the debts of other more spendthrift nations of the EU.

Equity

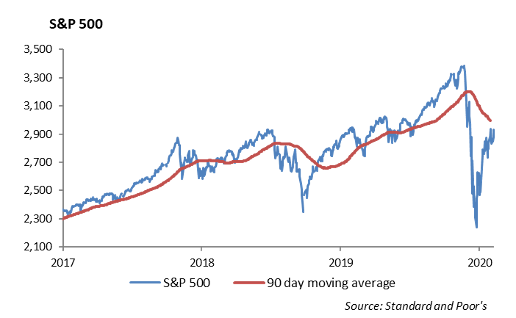

The S&P 500 increased another 3.5% last week, up to 2929. After the tumultuous ride in March and April, the S&P 500 is down -9% year to date and -14% off of all-time highs. Information Technology is the best performing sector, up 3.37% year to date. Energy is the worst performing sector, down -35%.

First Quarter Earnings

First quarter earnings are expected to decrease by about -12.7% year over year. However, revenue for the quarter is expected to increase by 0.20% from last year’s first quarter. Earnings season is halfway complete, as 278 companies in the S&P have reported data so far. 55% of these companies beat their earnings expectations, while 61% beat their sales estimates. The sectors with the most success so far this earnings season are Consumer Staples, Health Care and Info Tech, as over 80% of companies in these sectors beat expectations. The Information Technology sector has the highest earnings growth rate of any sector at 6.3%. Eight of the thirteen sub-industries in the sector are reporting higher earnings; Semiconductors and Systems Software have reported the highest growth.

Most recently, PayPal Holdings Inc (PYPL) reported astounding earnings results. Revenue growth was up 20% in April, despite the worldwide lockdown. In April, PayPal gained 7.4 million new accounts, and payment volume grew by 22%. Both Visa Inc (V) and MasterCard Inc (MA), on the other hand, saw declines of over -20%. On May 1st, the company saw its largest single day of transactions – even larger than Black Friday and Cyber Monday. The stock shot up 14% on earnings and is now up 34% year to date, highlighting another example of a thriving growth stock with a clear advantage in the midst of the coronavirus pandemic.

Model Portfolios

Core Series

In the Core Series models, we are reducing exposure in our international sleeves, including both developed and emerging markets. We do not see clear catalysts for growth in international stocks in the near future and are focusing our exposure to domestic large cap. We are also building up a defensive positon in our large cap domestic exposure by adding to the iShares Low Volatility ETF (USMV) and the Vanguard Value ETF (VTV). Value is currently down -19% year to date and heavily underperforming growth stocks. We are also reducing our exposure to Schwab U.S. Large-Cap Growth ETF (SCHG), which is up 1% year-to-date. This growth ETF has 37% of its assets in Info Tech and a heavy concentration at the top. The ETF has a top 10 concentration of 42% and a top three concentration of 25% of assets (MSFT, AAPL, AMZN).

Fixed Income

Credit Spreads Widened in the Face of Heavy New Issue Calendar

The U.S. Treasury Department announced last week that it plans to issue $3 trillion in debt through the second quarter of 2020. In an attempt to lock in low interest rates, the debt issuance will be skewed towards the long end of the curve, and for the first time since 1986, they will issue 20-year U.S. Treasuries. While the announcement initially led to an increase in rates across the curve, interest rates were little changed by the end of the week. We continue to believe the aggressive asset purchases from the Fed will serve as the natural buyer of any U.S. Treasury issuance, whose balance sheet now exceeds $6 trillion. While intuitively such heavy issuance should drive rates up, we believe the risk to rates is more to the downside as both the Fed and investors are seeking a safe, positive rate of return and seem to have an infinite appetite to buy.

Corporate debt issuers continue to test the limits of investors’ willingness and ability to buy as overall volatility has remained low. Last week, $90 billion of corporate debt was issued from an incredible wave of 50 different issuers. Apple and Chevron issued $8 billion deals each. Both deals were well oversubscribed and issued with very little concession to bonds trading in the secondary market.

The over-supply of new issues seemed to finally catch up to credit spreads last week. Despite equity market rallies and increasing rates, spreads on investment grade bonds generally widened through the week. The increase in issuance is expected to continue this week as well. We have become more conservative with drop levels in the primary market and believe the market is currently saturated by the nearly $1 trillion in issuance so far this year.

Not all issuers have found success in the primary markets, however. Last week, it was expected that United Airlines would tap the market for over $2 billion in secured debt, however, they dropped the offering as price expectations exceeded 11%. United has already received $5 billion in payroll protection funds, and they also have potential access to $4.5 billion in federal loans. United attempted to secure the debt with an aged fleet, but investors priced the debt at unsecured debt yields. United pulled the deal and stated they will attempt to secure better financing terms at a later date. Despite the reopening of the economy, we believe U.S. airlines will continue to experience profitability stress due to consumer hesitance, limited seating capacity, and increased costs to meet heightened cleanliness standards.

High Yield

Credit Spreads Tightening

High yield credit tightened 18 bps for the first full week of May. Quality continued to outperform across the different rating tiers this week prior – B’s tightened 25 bps, BB’s tightened 17 bps, and CCC’s tightened only 4 bps. CCC’s are absorbing the additional default risk in the COVID-19 climate. The High Yield Corporate Bond Index is now 400 bps wide of year-end 2019 levels. U.S. high yield fund inflows were strong again at $3.5 billion last week, making it the sixth consecutive week of inflows into high yield funds.

The primary market picked back up last week, pricing $10 billion of deals into the market. Deals last week included Avis Budget Group and Kraft Heinz Co. Avis issued in search for liquidity as the car rental industry has taken a large hit over the last few weeks. Kraft Heinz issued $3.5 billion to fund a tender for some of its short-term notes.

Energy

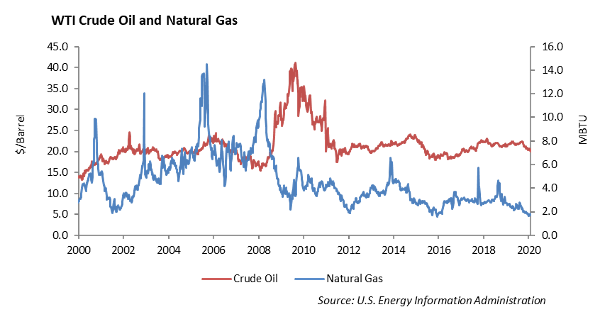

The energy markets saw a supply-related recovery last week. WTI Crude Oil rose 25%, Brent Crude Oil rose 17%, and natural gas fell -4%. WTI Crude Oil is now just under $25 a barrel. Last week was the second consecutive week of price recovery due to optimism from global supply reductions. U.S. rig count dropped below 300 for the first time since 2009. IHS Markit data estimated that global crude oil supply will drop by 14 million barrels per day from April to June, which would be the largest oil production drop in history. Despite the recent recovery, the current economic landscape still does not bode well for many American independent oil companies. Long term WTI prices at $25 a barrel could cause leverage for these companies to shoot up to high single digits.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.