Volatility Persists as Coronavirus Spreads

Last week, the global market continued to fluctuate as investors attempt to understand the impact that the coronavirus will have on the economy. The US jobs report for February was fairly strong, and unemployment ticked down to 3.5%; however, employment is a lagging indicator, so we expect the upcoming jobs number to reflect a slowdown. First Quarter US GDP growth are bound to be anemic, leaving analysts to evaluate how quickly the economy will be able to reaccelerate.

The global spread of the virus is unlike any market disruption we have seen for a long time. While it seems that China has contained the virus, the situation appears to be escalating in Europe and the US.

Monetary Policy

Can fiscal or monetary stimulus have any effect on the economy during times like this? The Fed announced an emergency 50bps rate cut last week, and futures are pricing in another 50-75bps for the coming March meeting. In addition, the Trump administration announced a $7.8 billion spending bill to combat the virus. While these measures will not affect the economy in the short-term, signals that policy makers will help prop up the economy at any costs should soften the blow.

Equities

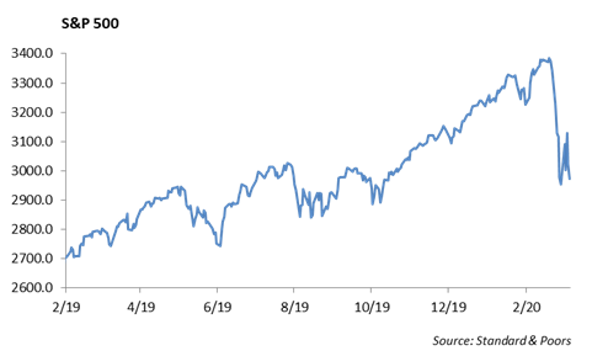

The S&P finished positive by 0.60% for the week after large upward moves on Monday and Wednesday. Year to date, the S&P is down 8%. Looking at one-month sector performance, every sector is negative, and the worst performing stocks are energy, down 23%, and financials, down 18%. The only sectors down single digits so far are defensive sectors, including utilities, real estate, staples and health care. The majority of stocks in every sector are trading below their 100 day moving averages.

The travel and leisure industries are facing significant pressure from the outbreak, and several stocks in have declined sharply in value over the last month. Royal Caribbean and Carnival cruise lines have lost almost half of their market value, and both of those names are down over 10% premarket right now. Airlines have lost 45% over the last month. Casinos and hotels like MGM, Penn, and Choice are off by double digits. After today, many energy names will join the list of market values being cut in half. Halliburton, Conoco, Occidental, and Marathon are all down over 30% premarket.

Outperformers include certain staples stocks, such as Costco, as bulk purchases trend upwards. Additionally, video game publishers and names such as Netflix have shown relatively stronger performance, as these stocks benefit from more users staying at home. Netflix is still up 14% YTD.

As equity markets have declined, we are incrementally adding to the large cap basis. At the end of last week, we moved to rebalance our equity exposure relative to fixed income by selling short term bonds and buying large cap equity. We still believe that large cap domestic stocks are favorable to small caps and international equity due to the risk of a global slowdown and heightened volatility. While uncertainty of the future may be uncomfortable, we believe in the adage “buy when prices are low and sell when prices are high.” We will continue to normalize equity exposure in portfolios and models if the equity markets decline further.

Energy – A Game of Chicken

The OPEC+ meeting last week was disastrous for energy investors and companies. Saudi Arabia and other members of OPEC sought a significant supply cut to support crude oil prices, which have been under pressure from the coronavirus’ impact on demand. Russia objected and broke the alliance, seeking to keep oil prices at $45/barrel. In retaliation, Saudi Arabia and OPEC have dropped prices, initiating a “game of chicken” with Russia and threatening to push prices down to very low levels. Saudi has committed to a supply of up to 12 million barrels per day, which would push crude oil prices to $31/barrel. US shale drillers will be significantly impacted by the price war as well – the breakeven point for US oil is typically $40/barrel. We can expect to see bankruptcies in US drillers similar to that in 2016. Although there will be a positive cost offset to consumers, the more glaring takeaway is that former OPEC countries now face an even greater pressure with declining prices and low demand.

The effects are already being reflected in the market. For example, Occidental Petroleum, an investment grade credit and larger exploration and production company, has 30-year debt that is trading below 70 cents on the dollar and over 7% yield.

Fixed Income

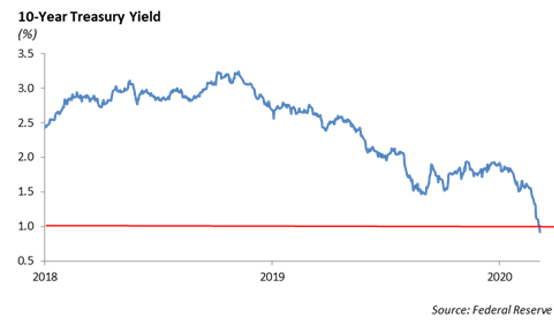

Interest rates fell hard throughout last week and continued to decline even on days that equity markets were positive. Rates continue to price in a serious economic decline. US rates across the curve hit all-time lows with the 10-year falling below 1% and the 30-year falling below 1.50%. Globally, rates are not moving nearly as much, which signals that the entire world sees US treasuries as a safe asset.

Despite the dramatic decline in rates, we still do not expect to see negative interest rates in the US, and we believe rates and markets will eventually normalize. We are evaluating current rates as more of a momentum phenomenon and less as a fundamental story. We have begun shortening the duration of fixed income portfolios, as the current condition is not the time to extend and reach for yield.

High Yield

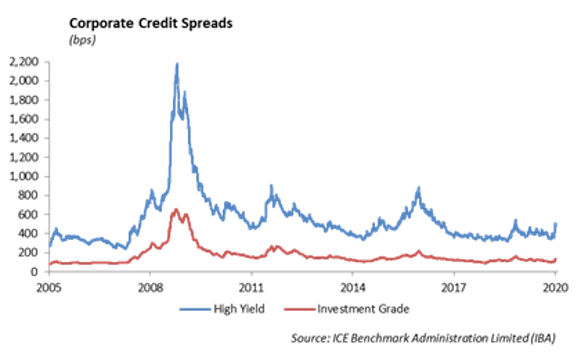

Spreads in high yield widened 60 bps last week. Outflows in ETFs last week were the fourth-largest on record with $5.1 billion leaving high yield funds. For new issues, Cleveland Cliffs was able to complete their deal last week, issuing out $725 million after scrapping their unsecured portion. Bausch Health pulled their offering, and it would be surprising to see the primary market active this week in either high yield or investment grade. Bid-ask spreads are widening and broker-dealers are not looking to take on risk. Fortunately, the recent up in quality moves we made in our Short Duration High Yield strategy should protect us, and we will take the opportunity to strategically add to beaten up BB debt.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.