Fear Grips the Capital Markets over the Spread of the Coronavirus

The country is taking dramatic steps designed to impede the spread of the coronavirus by primarily limiting social interaction across society. “Social Distancing” is strongly encouraged, and in many cases mandated, in a war to slow the spread of the virus. As a result, almost all major events have been cancelled or postponed, including Broadway shows, NCAA Basketball, and concerts. In addition, smaller activities and events such as school, church services and weddings have been cancelled, postponed, or moved online.

All of this has resulted in a social disorder that is creating a profound impact on the economy. During this period, restaurant and entertainment spending will decline sharply, lay-offs will likely increase as companies protect profit margins, and demand for credit to expand business will be down. We will not see the full impact of the efforts to control the spread of the virus until the second quarter of 2020.

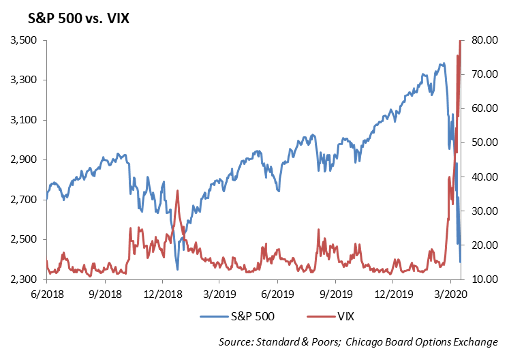

The response from the capital markets was historic by any measure. Yesterday was the worst one day sell-off in stock prices since October 1987. Stocks sold off hard this past week, and the S&P 500 is down 26% year to date. The Federal Reserve lowered the Fed Funds rate to zero and reinstituted its bond purchase program. As a result, bond yields declined to historic low levels.

At the same time volatility measured by the VIX, which normally reads below 20, spiked to over 70.

We believe:

- This is an event that has the potential to negatively impact global economic growth. Our goal is not to try to predict the severity of the coronavirus as it spreads. Rather, we seek to assess its potential impact on the valuation of individual securities and the capital markets.

- Through the turmoil of the capital markets, valuation matters. Identifying the revenue and profit impact on company earnings is difficult. We expect that certain industries, such as the energy pipeline and mall REITs will be challenged during this period. In addition, certain business models that require personal interaction, such as food service, will also be challenged.

- We expect the residential housing market to slow over the near term as consumers shift priorities toward increasing savings.

- The Federal Reserve is concerned with keeping capital market functions working smoothly. Lowering interest rates will help to grease the economic machine and provide liquidity to the market in order to keep the economy moving. With several major banks borrowing at the discount window on Monday, this function is critical to allow the banks to operate.

- The Airline industry will require a federal bailout. With restrictions on business and personal travel, airline traffic is down considerably. We would expect that the federal government offer some assistance similar to the TARP program offered to banks during the Financial Crisis.

- We are in unchartered waters with respect to dealing with the spread of this virus, and the fear of the unknown is gripping capital markets. As more information is discovered about the virus, prices of financial assets will normalize.

- This is an opportunity to reposition and rebalance portfolios.

Here is what we are doing:

In our Portfolio Models, we are adding to domestic equity as the market sells off. Again, we don’t pretend to try to pick the high or the low. We believe that as the market sells off, we will capture the broad market equity basis through ETF’s, such as SPY or SCHX, in incremental steps. Our buying budget is roughly 3.0% to 6.0% in equities depending on the Portfolio Model.

- We added to the S&P 500 basis throughout the week. However, given the severity of the downturn, we are still underweight the equity basis.

- With the yield on the ten year U.S. Treasury at a historic low level of 0.77%, we are shortening durations of Core and Intermediate portfolios.

- With the spike in volatility, we are reducing exposure to low volatility strategies and moving back into broad market growth equity strategies.

- We are not adding to international or emerging market exposure at this time.

- Where appropriate, we are taking losses in taxable accounts while staying fully invested.

Monetary Policy

The Federal Reserve, in a coordinated global response from the major central banks to provide liquidity to the capital markets, lowered Fed Funds rate to zero this past week and announced that it would be increasing the level of bond purchases in its portfolio. By lowering the Fed Funds rate to zero, the Federal Reserve is ultimately supporting the banks. This move lowers the cost of bank funds and provides relief to those accessing credit. The major banks indicated that they borrowed at the discount window on Monday.

In order to support a sustained level of economic activity, there needs to be meaningful fiscal stimulus. We expect fiscal initiatives in the range of $200 – $450 billion will be needed to help sustain economic activity. That represents roughly one to two percent of GDP.

Equities

Year to date, the S&P is down 26.14% to 2386. The DOW is down 29.26% YTD to just above 20000. The downwards move took about 3-4 weeks, and we are now in a bear market. We have been continuously adding to the domestic large cap ETF, SCHX, with each decline to average into our price.

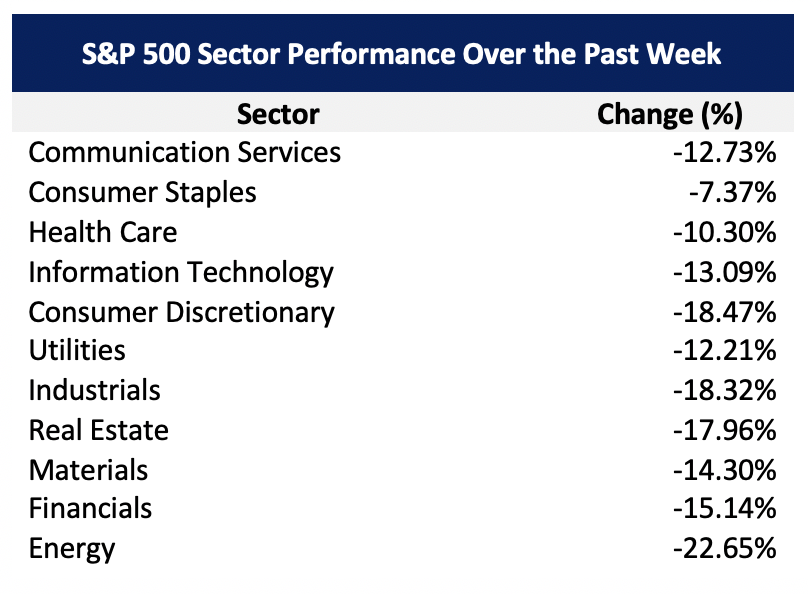

Energy is down 55% YTD and Financials are down 35% YTD. The top performing sectors are Consumer Staples and Health Care down 16%, and 20% respectively. Stocks that are outperforming include Costco, Amazon, and Eli Lilly:

- Costco: Currently down about 3% YTD, Costco has outperformed as bulk buying significantly increased last week. Consumer staples are doing fairly well in general as people stock up on essentials.

- Amazon: Down 8% YTD, Amazon is outperforming tech by over 15%.

- Eli Lilly: In general, healthcare names are outperforming, but Lilly has held flat for the year. Any healthcare company that is currently associated with the possibility of a corona vaccine right now is almost guaranteed to outperform.

All stocks are trading at an unprecedented discount, and in times like these, fundamentals seem to be thrown out the window. A couple of interesting laggards:

- JPMorgan: Down 37% YTD and trading at 8x earnings.

- Nike: Down 34% YTD and trading at 23x earnings.

- Salesforce: Down 24% YTD.

- Starbucks: Down 34% YTD and trading at 19x earnings.

- Boeing: Down 60% YTD at a P/E ratio of 8 and trading at $129.

Fixed Income

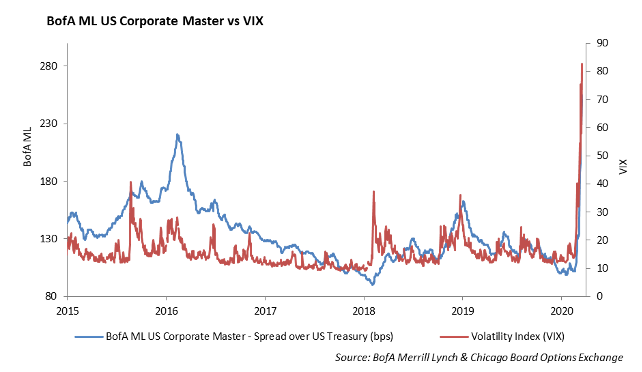

As the Fed cut rates to zero, the treasury curve followed suit by declining back towards all-time lows that were set the prior week. Interest rate volatility has remained significantly high over the past few weeks. While many investors are focused on the VIX index, investors should also pay attention to the BofA MOVE Index, which measures volatility across the treasury curve. The VIX is at historic highs of 75%, but the MOVE index is at an unfathomable level of 125%. As global investors continue to use treasuries as the risk on or risk off pool to grab from, volatility will remain high. We are also monitoring liquidity in the treasury market. While the US Treasury market is largely known as the most liquid market in the world, the recent market has added stress to its liquidity. Bid/Asks that are normally only a few 1/32 of a point apart have been trading between 1/2 and a full point apart.

Spreads across all credit sectors continue to widen significantly. Corporates, municipals, mortgage/asset backed and CLO’s are all wider between 100-200bps, depending on the rating. While it may seem that everything is currently on sale, we remain very selective with credit exposure. We continue to buy debt of large, high quality companies with idiosyncratic issues that we think will be weathered beyond the virus. Last week, we were buyers of long end Exxon at 215bps and Boeing at 315bps spread over their benchmark treasury. While there certainly are negative stories behind the two issuers, we believe the widening is an overreaction to short term credit events that can be overcome.

High Yield

The coronavirus and monetary policy has only resulted in increased turmoil in the high yield market. Last week, the high yield index widened another 170 bps, including a one day move as wide as 104 bps. On top of that, yesterday’s market moved out about another 100 bps. The total index is down more than 9% on a year to date basis. The up in quality trade has “worked,” as BBs have returned -7.25% and BBBs almost -4%. The turmoil has locked up primary market issue, resulting in an incredibly sloppy secondary market as bid-ask spreads on high yield names have been as wide as 5 points.

In our models last week, we added a sleeve of short term high yield bonds, ticker SHYG, as the ETF has not been insulated from the market. The recent velocity in sell offs with fixed income has resulted in many of passive funds trading at a significant discount to NAV. Currently, SHYG is trading at a half percent discount to NAV, and it was at a 1.45% discount when we added the sleeve last week. This example isn’t even the most pronounced. The ultra-common investment grade ETF, LQD, was trading at a 5% discount to NAV on March 12th.

Energy

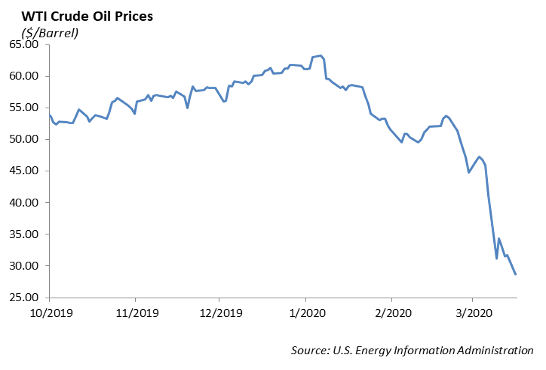

Energy markets are possibly the most bludgeoned of asset classes this year. Crude oil is down more than 50% year-to-date with last week’s prices falling 23%. Yesterday, crude oil dropped 9.5% to end at $28.70/Bbl. Not only is price under pressure from the virus and the OPEC+ collapse, but travel bans are now taking real effect on prices as well. President Trump’s plan to buy oil reserves to fill the Strategic Petroleum Reserve did provide some price relief on Friday, but clearly this was short lived. It’s important to note that some American energy companies cannot survive sustained periods with oil priced under $40, much less $30. Therefore, debt on really well established but highly levered energy names, like Occidental, is trading at 75 cents on the dollar for 5-year debt. Even Exxon was downgraded from AA+ to AA by S&P yesterday despite its strong balance sheet.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.