Fear of Coronavirus Grips Capital Markets

The global economy is slowing as a result of the coronavirus spreading from China. While China is the epicenter of the virus, it has spread quickly around the globe and cases are confirmed in countries including South Korea, Africa, Iran, Italy and the United States.

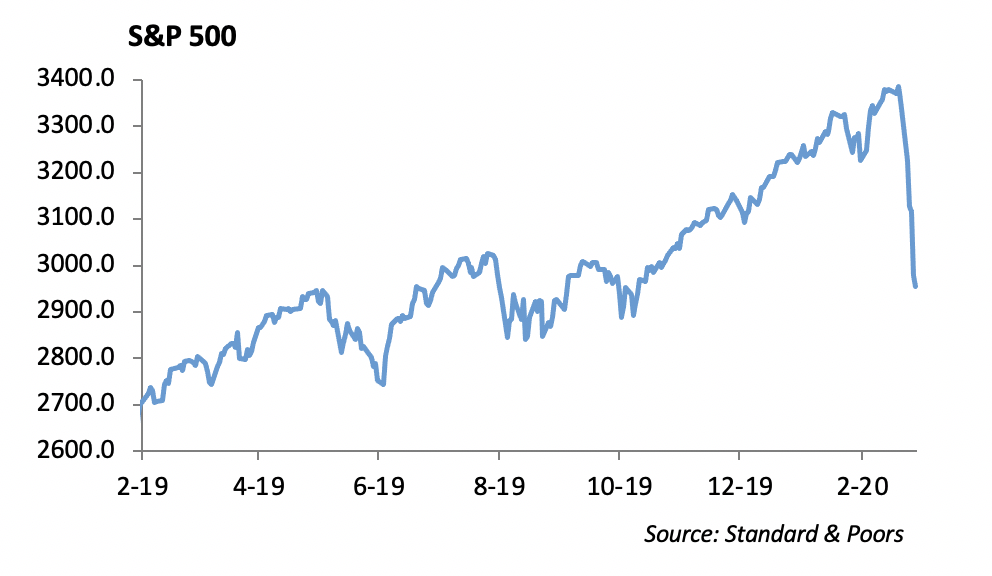

The response from the capital markets was historic by any measure. Stocks sold off hard this past week, and the S&P 500 was down 11.49%. Over 90% of stocks in the broad market index are now down over 10% from their peak. Bond yields declined to historic low levels.

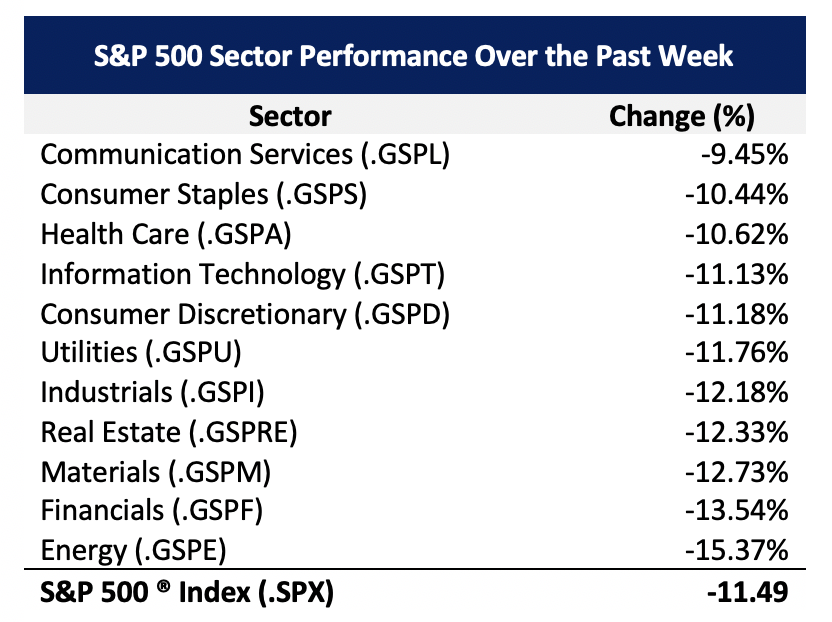

Energy and Financials were the worst performing sectors in the S&P 500, declining by -15% and -13% last week. The best performing sectors were Communication Services, Consumer Staples and Healthcare, which only declined -9.45%, -10.44%, and -10.62% respectively. At the same time, volatility, measured by the VIX, which normally reads below 20, spiked to over 40.

We believe:

- This is an event that has the potential to negatively impact global economic growth. Our goal is not to try to predict the severity of the coronavirus as it spreads. Rather, we aim to assess the potential impact on the valuation of individual securities and the capital markets.

- The equity market has the potential to rebound quickly once there is more clarity in information surrounding the virus and its economic impact. In post-Financial Crisis markets, the rebound has come quickly as it did in 2016 and 2018.

- The impact of the virus will begin to be revealed in February data. For many companies, first quarter earnings will be negatively impacted.

- The Federal Reserve lowering interest rates will not prevent the spread of the virus. The best that the Fed can do is provide liquidity to the market in order to keep the economy moving. However, lowering rates may actually cause more damage than good given the amount of liquidity already in the system.

- The fear of the unknown is gripping the capital markets. As more is discovered about the virus, prices of financial assets will normalize.

- This is an opportunity to reposition portfolios.

What we are doing:

In our Portfolio Models, we are adding to domestic equity as the market sells off. We don’t pretend to try to pick the high or the low. We believe that as the market sells off, we will capture the broad market equity basis through SPY or SCHX, in incremental steps. Our buying budget is roughly 3.0% to 6.0% in equities depending on the Portfolio Model.

- We added to the S&P 500 basis throughout the week. However, given the severity of the downturn, we are still underweight the equity basis.

- With the yield on the ten year U.S. Treasury at a historic low level of 1.04%, we are shortening durations of Core and Intermediate portfolios.

- With the spike in volatility, we are reducing exposure to low volatility strategies and moving back into broad market growth equity strategies.

- We are not adding to international or emerging market exposure at this time.

Monetary Policy

One of our themes this year is that the White House Administration will challenge the independence of the Federal Reserve leading up to the election. Our expectation is that the Federal Reserve will participate in a coordinated global response from the major central banks to provide liquidity to the capital markets.

Equities

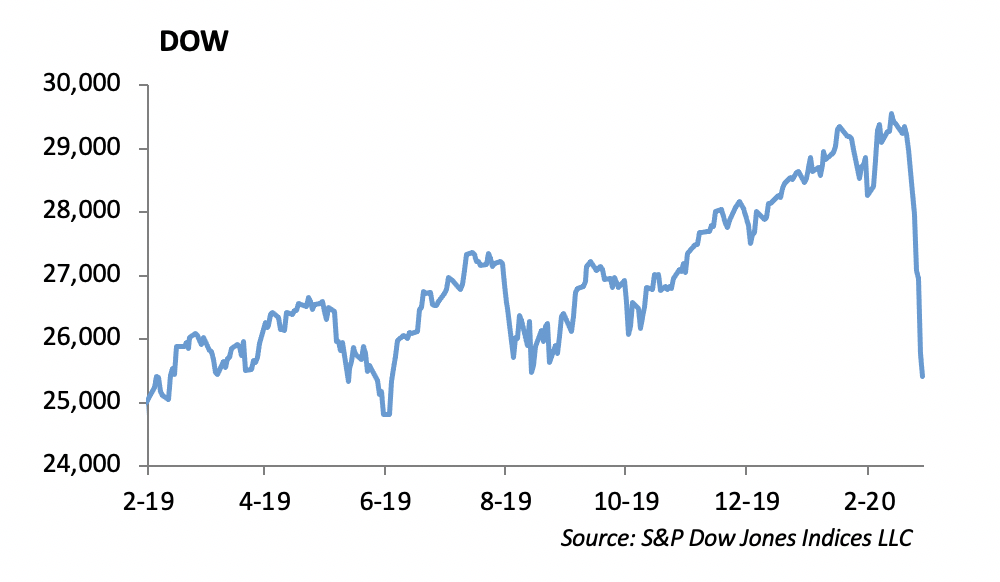

Stocks had the worst week since the financial crisis, with the S&P falling 11.5%, the DOW falling 12.4%, and the NASDAQ falling 10.5%. Year to date, the S&P is down 8.56% to 2954. Every sector has been hit hard, specifically tech and energy. Energy is down 25% YTD and Tech is now down 4% YTD after a quick 10% rise to start the year. All 11 sectors were down double digits last week.

First quarter profits, initially predicted at around 10% growth for the year, now seem very unlikely to hit that mark as supply chains face challenges with the virus. In the event that the coronavirus is quickly contained, it is possible that industries could increase production to make up for first quarter shortfalls; however, several industries, such as consumer and leisure businesses, cannot recover from lost days of attendance.

A Historic Market Correction

We have had 26 corrections of 5% or more since 2009, but the velocity of last week’s correction marks history as the fewest number of days taken for the market to lose 10%. The DOW lost over 3000 points, falling close to or over 1000 points on 3 different occasions.

We believe this is will be a 1 to 2 quarter event, and dollar cost averaging over time is the best approach to reducing the impact of volatility. With an increase in selling pressure, it’s hard to predict exactly when the turnaround will begin. In our WCM Tactical series we have added 3 times to our Large Cap ETF, SCHX, on the large drops, and are looking to continue adding and average into our position if the market keeps falling.

Fixed Income

The Coronavirus pushed yields in the US further into All-time lows. The short end of the curve has fallen to 0.75%, and the 10-year treasury is quickly approaching 1% after falling 40bps over the week to 1.04%. US bonds have outperformed the rest of the world. The Barclays Aggregate is up 4% and long treasuries are up are up 14% so far in 2020 versus negative returns from equity markets.

The risk off trade has led to a widening of credit spreads by 20bps; however, this widening is relatively tame when compared to the drop in equity markets. We were buyers of credit in the consumer sector, as we believe the beaten down sector will be the first to recover once we see a noticeable shift in the spread of the coronavirus.

High Yield

The high yield index widened out almost 140 bps last week as fears on global growth have investors in a risk off sentiment. The index is about 140 bps wide of year end levels now. The damage done to the quality tiers is as one would expect. CCCs were down almost 4.5%, Bs almost 3%, while BBs were the technical winners down 2.25%. BBs have also performed the best YTD at down 1%. Funds had the 7th largest outflow recorded at $4.2 billion. With the weakness, we purchased AMC Networks 2024, Tenet Healthcare 2024, Penske Automotive 2026, and T-Mobile 2026. Each issue was about 2 points off of recent highs, and we believe each company has a strong ability to weather volatility.

The virus fears led the primary market to a halt. The lone high yield new issuer last week, Cleveland Cliffs, attempted to issue debt to fund their AK Steel acquisition. They raised yields and struggled to attract investors. They even pondered throwing out the unsecured portion of the deal to attract investors. Sooner or later a lack of supply in both high yield and investment grade debt should support spreads, but that effect may not be seen until virus fears have passed.

Energy

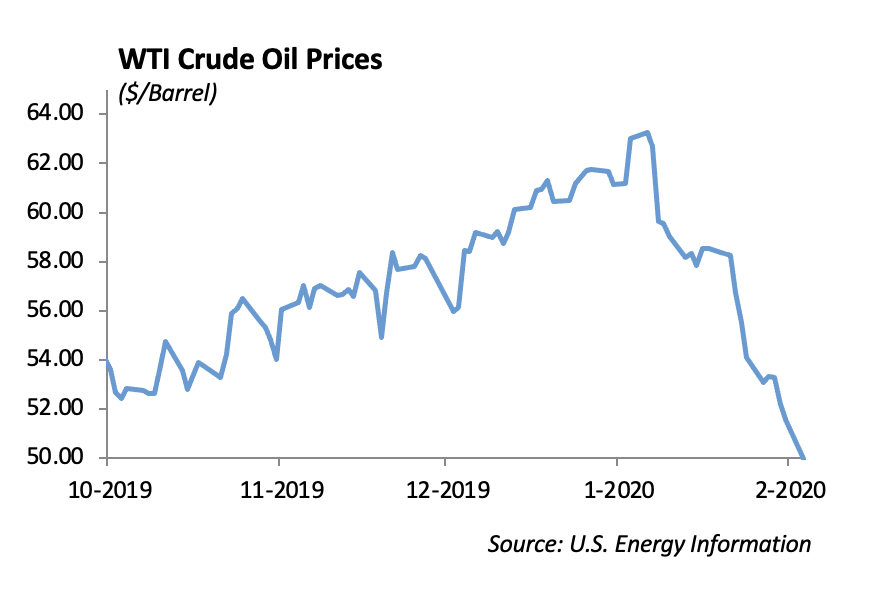

Energy markets also fell victim to the virus. WTI crude oil fell a significant $8.62/bbl or 16%, while natural gas fell $0.22/mcf of 12%. These were the largest weekly declines since 2008. In the height of the SARS outbreak in 2003, oil demand fell by 260 thousand barrels a day, and it looks like energy could fall even more with the coronavirus outbreak. Oil prices at around $45/bbl puts significant pressure on energy companies, so it is no shock that the sector has been the worst performer in investment grade, high yield, and equities. All eyes now point to the OPEC+ meeting over March 5-6, as potential conflict may arise over whether or not to cut supply supporting crude oil prices. A disagreement over the supply cut would out additional negative pressure on prices, leading more to the downside risk than the upside with a uniformly accepted supply cut.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.