The Economy is Virtually Shut Down

We are living through an historic period that will forever be marked in time as a result of this global coronavirus pandemic. The dangerous virus spreading around the globe doesn’t discriminate between sex, age, race or nationality. Efforts to control the spread of the virus include shutting down businesses, encouraging people to quarantine in their homes, and implementing social distancing – a new vocabulary word to describe staying six feet apart from the person next to you. All of these efforts have had a significant impact on the economy and outlook for growth. In addition, the strains in the economy and capital markets put stress on the financial system, which has forced banks to pull lines of credit, and the Federal Reserve to provide backstops for commercial paper and repurchase agreements.

In order to understand the overall impact these events have on investment strategies, we have separated our analysis into three areas: the economy, the financial system, and the capital markets.

The Economy

The economic impact we are experiencing as a result of efforts to slow the spread of the COVID-19 virus has been severe.

- We expect there to be a long recovery period, but still shorter than the recovery from the Financial Crisis. The Federal Reserve’s response has been swift and effective already. The fiscal response, with the $2 trillion CARE Act passed by Congress last week, will help provide support for consumers and businesses. The fiscal response came much quicker than in 2008-2009, and it includes payroll assistance to some businesses in an effort to support job retention. The faster response will increase the impact it has on stabilizing the economy.

- Whenever aggressive monetary policy and fiscal policy are aligned, prices on financial assets are higher six months later.

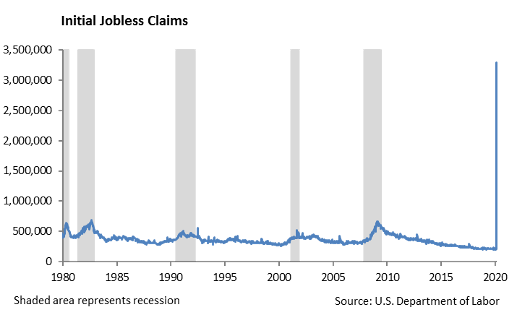

- Over 3 million people filed for unemployment last week – a number with no historic precedent. Even during the Financial Crisis, weekly unemployment was never higher than 600,000 claims. The labor department will release employment figures this Friday. We don’t expect the March figures to show the complete extent of job loss which occurred over the last two weeks. April will likely be more severe as the federal guidelines for social distancing remains in place and businesses close.

- This will not be a “V”-shaped recovery; however, we will see economic growth come back by Q4. Many of the service businesses, which have been the hardest hit by the social distancing guidelines, will be slower to comeback. This will impact commercial real estate, including CDO’s, CMBS, and REITS.

- There will be an opportunity to reset global trade in a manner that is collaborative and stimulates global growth.

The Financial System

- The financial system is much stronger today with bank capital levels in excess of 8% compared to 4% during the financial crisis. However, the financial system is under severe stress with increased delinquencies in consumer and corporate loans.

- The Fed has implemented several lending programs that are designed to provide support to the financial system, including a backstop for commercial paper lending and repurchase agreements. We expect the Federal Reserve to begin direct lending programs to support businesses, cities, and municipalities.

- Credit quality of the underlying collateral is deteriorating and leverage is being forced lower in certain areas, including mortgage REITs by banks. The Fed is buying agency MBS in its current asset purchase program. Forced selling in non-agency MBS is negatively impacting the stocks of mortgage REITs.

- The banks are taking the steps we would expect in order to preserve capital and credit quality. They are living the 2020 stress test, which has been mandated by the Federal Reserve following the Financial Crisis.

- We expect the banks to come out unscathed. Once volatility subsides and credit spreads tighten, watch for heavy issuance of subordinate debt by smaller banks to help prop up capital positions.

The Capital Markets

- Over the next few weeks, the equity market will likely take its cues from news around the coronavirus. We expect volatility to begin to trade lower over the coming weeks, and the focus will shift to earnings.

- On the equity side, the winners are technology and cloud computing. Employees working remote forces a spike in laptops and webcams. Cloud business should be strong.

- On the bond side, it has been treacherous for credit. We are in the classic phase of a liquidity squeeze where there is forced selling of bonds and no natural buyer. We saw heavy bid lists for CMBS last week and bonds trading at yields between 8 and 10%.

- New issue corporates have been very heavy at spreads that, one month ago, would be laughable. However, companies are issuing debt regardless of the cost in order to build a cash war chest. The increase in debt issuance may be to weather the uncertainty during this time. However, we propose that this could be used as heavy ammunition to buy back stock once the coast is clear. Debt issuers include 3M, Pfizer, Nike, Archer Daniels Midland, McDonalds, Autozone, Weyerhauser, CVS, CSX, Target and Home Depot. With stock prices down over 40% year-to-date, banks have been heavy issuers as well, including Goldman Sachs, Morgan Stanley, and JP Morgan. Watch for a pick-up in stock repurchase programs in the summer.

- Spreads in municipal bonds have slammed back in at the end of last week. There is no fundamental problem with credit quality in the muni market. We believe municipal bonds are still cheap.

- Preferred stocks were hit hard over the past three weeks. We like the preferred stocks of the banks, including JP Morgan, Truist, Morgan Stanley and Bank of America, where investors can earn 5.5 to 6.0%.

- With the Fed in buying mode, spreads in the credit markets will adjust quickly. The Fed has implemented several programs that are designed to backstop repurchase agreements and commercial paper, which in turn supports the money market funds. We want to be on the side of the Fed as they are buying and believe that, like QE following the financial crisis, it will be good for financial assets.

Democracy and Capitalism

The long-term issue we are wrestling with is how the evolution of our form of democracy and capitalism impacts investment strategies. Clearly, this economic recovery will be heavily subsidized by the U.S. government. The $2 trillion rescue package will be financed by debt. This year’s budget deficit will likely exceed $1 trillion. We continue to spend money to support the economic expansion. The next step will likely be a downgrade in the credit rating of the U.S. government.

Equity

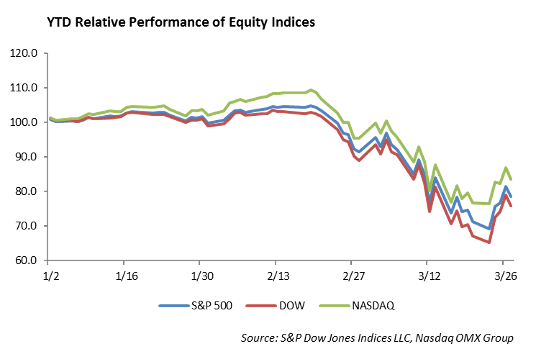

The domestic equity markets posted a strong rebound last week, with the S&P 500 rising 10% over the week even after Friday’s rough close. The DJIA posted its largest weekly gain since 1938. Every sector was green, with Utilities and Industrials the outperformers, up over 15%. Utilities, Information Technology, and Consumer Staples are still the strongest sectors on a year-to-date basis, down about -15% each. Year to date, that brings the S&P 500 down -21%, the DJIA down -24%, and the NASDAQ down -16%. Markets were still fairly volatile, with over 3% moves on 4 of the 5 trading days. However, volatility is lower from the 5% swings we were seeing two weeks prior. On Thursday, the equity markets moved higher despite the record-breaking unemployment numbers, highlighting that most of the negative news surrounding the coronavirus may already be priced into the market at current levels. Jobless claims came in at 3.3 million vs. 282,000 the prior week.

Cloud computing and working from home are now the norm, and stocks in this space should see outperformance over the near term. Amazon, Microsoft and Google continue to be our top picks in this area and are well positioned to weather this storm. These are some of our largest holdings in our Large Cap Blend and our Focused Growth equity strategies. Right now, we are reevaluating these holdings every day as we anticipate how long these effects will take place. The S&P 500 is still -55% off of February highs.

Fixed Income

Interest rates moved sharply lower over the past week, with the entire curve tighter by over 20bps. The 10 Year U.S. Treasury rate is approaching 0.50% once again, and the amount of global debt trading at negative yields spiked by $2 trillion week over week. The Fed continued to support liquidity by buying U.S. Treasuries and mortgage-backed securities, bringing their balance sheet to over $5 trillion

Spreads on corporate and municipal bonds rallied sharply over the week, as the market digested the Fed’s ability to buy corporate bonds and exchange traded funds. While spreads on the US Corporate Index tightened 50 bps last week, it is still at wide levels not seen since the 2008 Financial Crisis at 300 bps. As equities rallied, new issuance picked up significantly, with $11 billion coming to the market at generous concessions. Overall, new deals were well received, oversubscribed, and generally outperformed the credit market.

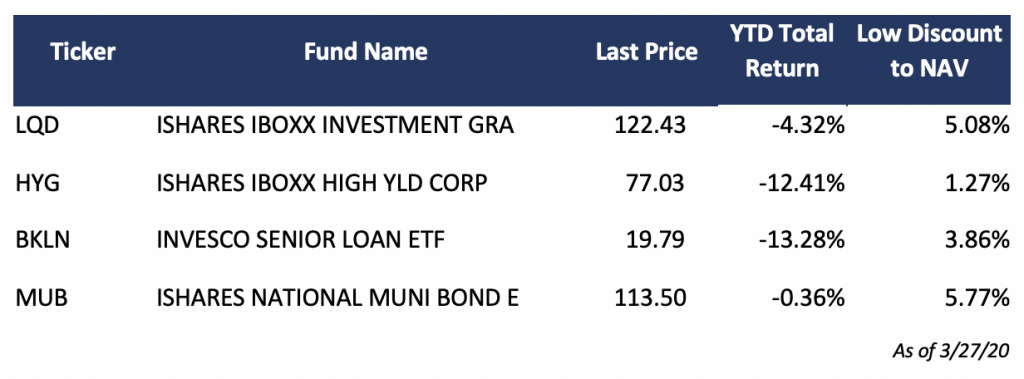

Fixed income funds continued to see outflows last week, but unlike weeks prior where investors simply wanted out of any risk product, this week was more technical as many large firms processed rebalancing portfolios. In these large rebalances, the outperforming asset, fixed income, was sold to purchase equity funds. So far this year, investment grade funds have seen a record outflow of $44 billion. In addition, there has been a continued outflow from leveraged loans in the amount of $8.4 billion, which is roughly 15% of total AUM. These outflows have resulted in substantial dislocations in the discount that a bond ETF trades relative to its net asset value. While we see continued volatility in equities based on underlying company fundamentals, we believe the dislocations in fixed income markets is more technical, and therefore, presents a significant buying opportunity. As an example, below are a few metrics from four large fixed income ETF’s that typically trade with very little deviation from their net asset value, including the year-to-date return so far in 2020 and their largest deviation from net asset value over the past year.

High Yield

The Fed’s announcement that it would be buying corporate debt was effective in restoring some liquidity to the high yield market last week. While Investment grade credit spreads tightened by 60 bps, spreads in the high yield area tightened by 110 bps, with some individual names tightening significantly more. In investment grade fixed income, the higher quality segment outperformed last week with AAA’s returning 9.3%. Longer duration outperformed short term debt by 3%. Similarly in high yield, the higher quality was also the outperformer, returning over 5.5%. This was the first positive week of performance for high yield since mid-February.

It was a historic week for investment grade new issues as over $110 billion of new issuance priced last week. The primary market was met with high demand, and each issue was typically oversubscribed by 6 times. The offerings performed extremely well, tightening by 30-60 bps immediately. In contrast, the high yield primary market has been closed off, with no deals pricing since March 4th. Cincinnati Bell is the only prospective high yield issuer as it looks to support its buyout.

Despite the increased demand for new issue investment grade corporate debt, fund flows were negative for the second week in a row as $38 billion was taken out of ETF’s and mutual funds. This data is reported in the middle of the week so it does not capture flow activity which occurred late in the week. High yield funds were also negative as $2 billion came out of ETF’s and mutual funds.

We remain cautious in adding high yield. When looking at high yield bond returns after past major event-driven sell-offs, returns of high yield bonds were all over 20% in the next two years. These events include Black Monday, the 1990 recession, 9/11, and the Financial Crisis of 2008, which all had an initial drawdown of -7% or more. This does not attempt to predict the outcome of the coronavirus on high yield bonds, but it provides an interesting context for navigating this storm.

Energy

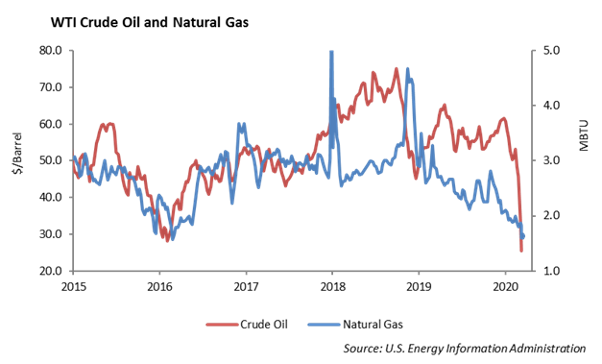

WTI Crude oil fell 4%, while natural gas rose 2% last week. Oil prices, which are trading at $20 per barrel, have dropped for five straight weeks as demand continues to fall due to the lack of travel caused by coronavirus. Oil prices are trading at levels not seen since 2002. Supply continues to be fed by the OPEC+ falling out. There appears to be no headway in the Saudi-Russian disagreement, as Saudi Arabia appears to have had no communication with Russia. Russia states that current pricing levels are not necessarily catastrophic to its economy. The U.S. energy companies, however, have had a decline in the oil rig count as it’s declined by a significant 40 rigs – the largest decline since April 2015.

Energy companies operating in the shale region have been hit hard and we expect to see an increase in bankruptcy filings. Cal Resources was the latest to indicate that bankruptcy may be its next step. The integrated oil companies, including Exxon and Chevron, are better equipped to weather this storm; however, we expect that some will be forced to re-evaluate their dividends given lower cash flow.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.