Looking Past the Immediate Economic Impact

As the world deals with the spreading coronavirus, governments of almost every country are spending money to help sustain their economy and prevent an economic disaster. Berlin is providing up to €5000 to self-employed people and small businesses. Italy is proving roughly €600 for self-employed workers, and France is offering more than €1400 to its self-employed people. The United States Congress passed the CARE Act which will provide $1200 for everyone earning less than $75,000 per year. The programs around the globe are unprecedented and significant in the aid that they are providing to help keep the economy moving.

In the United States, the financial assistance is funded through printing money since our tax collections are not enough to cover the payments. The money comes from issuing securities through the U.S. Treasury. The spending flows through the annual budget as a deficit. The cumulative deficit is added to the gross debt outstanding. That model is consistent with every other developed nation.

However, because of the significant cost, some countries are planting the seeds for their next financial crisis as they try to provide economic assistance to their people and businesses through this crisis. With the United Kingdom leaving the European Union, Germany carries a greater burden to help finance the Union. Given the persistent economic challenges for countries such as Italy and Spain, we expect this crisis to weigh on the sustainability of the European Union in its current form. Growing debt levels relative to the size of their economy will be a concern following the coronavirus pandemic.

The Economy

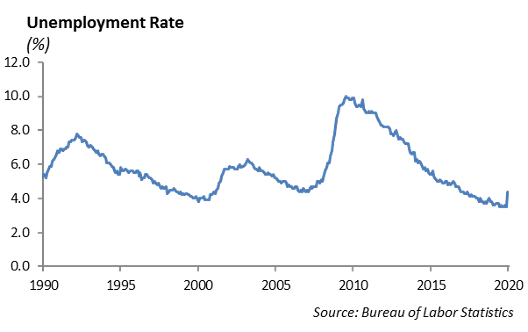

The impact of the efforts to control the spread of the coronavirus are decimating parts of the domestic economy. From restaurants, nail salons, and barbershops, to retail stores all over the country, in person commerce has been completely shut down in a matter of two weeks. Never before has there been this swift and dramatic of action that resulted in this severe of an impact to the global economy. The recent employment numbers from the Labor Department underscore the severity of the hit to the economy.

Employers laid-off and reduced more workers in March than in any month following the Financial Crisis in 2008. Job losses covered more aspects of the economy, which will make the recovery more difficult. The Unemployment rate for March increased to 4.4% from a low of 3.5% in February. We expect that the unemployment numbers are understated due to timing issues and would anticipate further increases in April.

Europe

The European Union had just finished long and difficult negotiations with the United Kingdom, which would set the stage for the next phase of Brexit when the news of the coronavirus began spreading around the world near the end of 2019. At the same time, Italy’s government had struggled to put together a coalition to govern after the most recent Five Star movement was losing steam. Over the last five years, Italy has been unable to achieve economic growth above 2%, and the economy showed signs of contracting in 2019. Meanwhile, Germany’s heavy manufacturing based economy showed signs of contracting, and its leaders continued to stand firm on running a budget deficit in spite of the signs of a slowing economy.

All of that changed when the COVID-19 virus spread. The amount of fiscal stimulus that developed countries have poured into their economies to help spur consumption and growth is unprecedented in the size and speed it was brought to bear. As it relates to Europe, how much fiscal stimulus is allowed and how its paid for will have profound impact on the European Union over the next several years.

Five Stocks to Weather the Storm

Amazon.com (AMZN)

Amazon.com (AMZN) Amazon.com, Inc. operates in two broad business segments: online retail shopping services (which includes North America and International) and Amazon Web Services (AWS). Up 3% year to date, Amazon is very well positioned in multiple facets. First, Whole Foods Prime Delivery has seen increased usage since the spread of the virus, which will cause a positive long-term effect as new consumers may have never used the service are now experiencing its benefits. While the overally economic shock of the virus to consumers will have a net negative effect on spending, the 90% of consumer spending that typically takes place in a brick and mortar store is completely shut down. The secular shift toward online shopping during this period could further accelerate consumer behavior in the future. Finally, AWS is also positioned for increased demands as the needs for cloud computing are accelerated with more and more firms forced to support an efficient work-from-home infrastructure.

AMZN has gross margins of 40% and operating margins near 5%. With Debt/Total Assets of 34.5% the company has a fairly conservative balance sheet. We expect the company’s earnings to be between $25 and $28 per share. At the current price of $1900 per share, AMZN stock trades at a P/E of 68x when we exclude extraordinary items and Price/Cash Flow of 24x. The company does not pay a dividend. We believe this company is well positioned for an economic downturn and is one way to build defense into an equity portfolio.

Johnson & Johnson, Inc (JNJ)

Johnson & Johnson is the world’s largest medical conglomerate, operating in over 60 countries with 250 subsidiaries. All of their products are widely known, with 26 of them generating over $1 billion in sales a year. The 3 main sections of JNJ include sanitation and healthcare, pharmaceuticals, and medical devices – all of which are businesses that could experience higher demand due to the coronavirus. We expect JNJ to be a leader in developing a treatment for COVID-19, as well as supplying hospitals with the necessary inventory to help rebuild.

Overall, this company is very stable and safe. It is a AAA rated company, the only one other than MSFT, and it has a dividend yield of 3%. A lot of companies may cut their dividends during times with unsustainable payout ratios, excessive debt, or just declining operating fundamentals. For 2019, Johnson & Johnson, generated just under $20 billion in free cash flow, against the $9.92 billion in dividends paid. The free cash flow payout ratio was 49.8%, which is a very safe ratio.

It currently trades at 15x earnings, which is well below its average of close to 20x. JNJ checks all the boxes for a safe investment and is in a sector which should capitalize from the coronavirus. We think this is a good stock to own.

Microsoft (MSFT)

Shares of MSFT have not been hit as hard, as they have a few segments that are benefiting from the recent shift to working from home. The biggest momentum Microsoft is seeing is from Microsoft Teams. Although we’ve seen more news of momentum from companies like Zoom and Slack, these companies only offer one primary service. Meanwhile, Microsoft Teams is just a portion of the Tech giant, so its growth may be more difficult to notice. However, Teams is actually the leader in this market. In November, Teams had just reached 20 million daily active users. By March 11, they had 32 million users, and last week, that number hit 44 million daily active users. Using the $5 fee per user, 12 million new users over the last month adds about $720 million in revenues, not including add-on services offered, which could put the number closer to a billion in newly generated revenues. Although many may consider this a short term spike, it is possible that companies will transition to more flexible work schedules if they see that productivity holds up.

Microsoft is currently trading at $153 per share. The company has a return on invested capital of 23%, a market capitalization of $1.1 trillion and debt to asset ratio of 30%. With MSFT trading at $153, its valuation is pretty full. With earnings for 2020 near $5.74 and revenue growth of 13%, the stock trades near a 26.5x P/E multiple and 22.4x Price/Cash Flow multiple. The 52-week high was back in February when shares were $190. Shares are down 3% YTD, but down over 20% from its highs just 2 months ago. With its strong balance sheet and ability to perform in many environments, we like Microsoft as another stock pick.

Lockheed Martin Corporation (LMT)

Lockheed Martin is a global security and aerospace company. It operates through four main business segments: Aeronautics, Missiles and Fire Control (MFC), Rotary and Mission Systems (RMS) and Space. LMT is a leader in defense and space, which are more in demand today than ever before.

The F-35 fighter jet represents roughly 25% of LMT sales, and sales are expected to improve in the years ahead. The U.S. government has a current inventory objective of 2,456 aircraft for the military, and Lockheed has commitments from eight international partners and overseas customers. Lockheed has a resilient customer base. The majority of its revenues are from US government departments and agencies, and we have been seeing soft bailouts. This company is essential, and the US will make sure it stays in good shape.

LMT has gross margins at 15.8% and net profit margins of 13.6%. The company has a return on invested capital of 42%, a market capitalization of $99 billion and debt to asset ratio of 28.9%. With earnings estimates for 2020 near $25.00 and revenue growth of 9.7%, the stock trades near a 15.7x Price-to-Earnings multiple and 15.2x Price/Cash Flow multiple. The stock has a dividend yield of 2.75% and a payout ratio 44%. The company increased their dividend 10% in 2018 and has done so for 10 straight years. The balance sheet was just 1.1x levered in 2019. They rarely buy other companies, and they don’t lever up big to do buybacks. So at 1.1x leverage they can sustain an impaired business environment better than most. We expect the business to hold up well in the event of a downturn in the economy or domestic government spending.

Alphabet, Inc. (GOOG)

Alphabet, Inc. (GOOG) is a holding company that engages in the business of acquisition and operation of different companies. It operates through the Google and Other Bets segments. The Google segment includes its main Internet products such as Ads, Android, Chrome, Commerce, Google Cloud, Google Maps, Google Play, Hardware, Search, and YouTube. The Other Bets segment, which is a significantly smaller part of the company, includes businesses such as Access, Calico, CapitalG, Nest, Verily, and Waymo.

Revenue growth is running at roughly 19% with gross margins near 56% and profit margins near 24.5%. The company has virtually no debt with a Debt/Total Assets under 6%. At a price of $1,092, the stock trades at a 22.5x P/E ratio when adjusted for extraordinary items. We believe earnings have the potential to grow from $47 to $55 next year. GOOG does not pay a dividend and has a return on invested capital over 18%. With a conservative balance sheet and strong cash flow, the company is well positioned to begin paying a dividend to shareholders and continue stock repurchases. The company has repurchased over $19 billion in 2019, and we believe that it could repurchase in excess of $25 billion in stock in 2020.

Model Changes

We have sold our low volatility fund (USMV) across our models and swapped it for the large cap domestic ETF. USMV was the risk off tactical strategy throughout our Portfolio Models, ranging between a 5-8% allocation depending on the strategy. Its outperformance YTD gave us an opportunity to swap back into large cap. We expect to adjust the Core Sector Model allocation this week given the change in valuations.

Fixed Income

In what felt like a period of stabilization in the markets and liquidity, interest rates remained fairly unchanged throughout last week. The MOVE Index has returned to fairly normal levels of 65 from its peak of 164 at the beginning of March. Global yields remain suppressed, and once again, the entire German Bund curve is at negative yields.

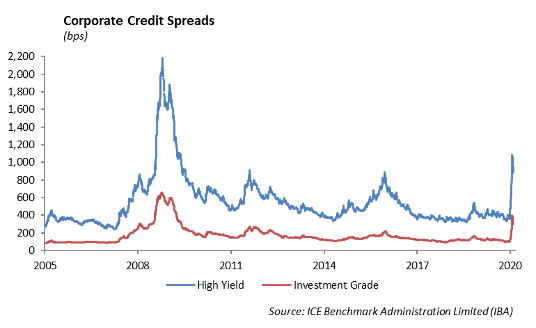

Investment grade credit markets were largely driven by the new issue markets, as 49 different issuers raised a new record of $117.2 billion in debt last week. New issue concessions continue to average around 20 – 30 bps. Despite the heavy issuance and concessions, overall credit spreads continue to tighten from their peak of 360 bps to 283 bps. Although liquidity is returning to the market, we are still seeing dislocated liquidity. As a result, short-term corporate bond credits and commercial mortgage-backed security (CMBS) markets have had dislocated prices due to forced selling. Inverted credit curves have allowed us to buy 1-2 year paper above 5%. A lack of buyers for CMBS has given us the opportunity to buy strong A-rated tranches at 8%+. Despite the improving market, we still favor the up in quality trade as the market still has a significant amount of economic data to digest over the coming weeks from the effects of the virus.

High Yield

High Yield widened 44 bps last week after back to back weeks of 100 bps moves. The primary market finally saw some activity last week after an extended period without new issuers. There was $2.9 billion of new issuance, including Tenet Healthcare, TransDigm, and Restaurant Brands, which each issued out secured debt to take preemptive liquidity measures. In the secondary market, CCCs and Bs had a negative total return, while BBs ended the week at 0.05% total return. Liquidity in high yield reveals that short end sellers are still seeing bids much wider than a fundamental analysis would suggest.

Energy

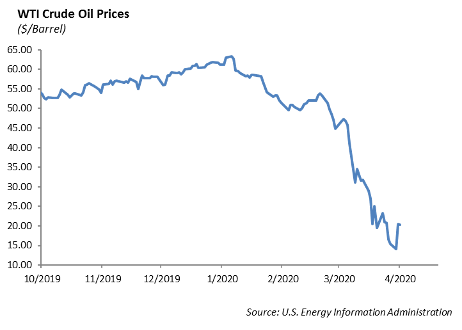

Energy markets had a huge week last week, and it was welcome to both equity and fixed income investors in the energy space. Oil had its best week ever, rising 32% to finish the week at $28.34/bbl. This occurred after President Trump gave very bullish remarks of his belief that supply will be cut by 10-15 million barrels per day on a Saudi/Russian deal. Russia downplayed Trump’s statements, however, and no agreement has been met as of now. We believe that a supply cut by the United States means that domestic oil companies will have some sort of relationship with OPEC+ in the future.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.