First Quarter Credit Review 2020

We expect global growth to slow and credit conditions to deteriorate in 2020 in the face of the spreading coronavirus and continued trade policy uncertainty. While the resolution of the phase one agreement between China and the United States, signed January 15th, was expected to provide a boost to economic growth, the spreading coronavirus has had the opposite effect. Leading up to the outbreak of the coronavirus, economic growth in China was already slowing from 8% to 6%. However, we expect economic growth in China to come in near 2% for the first half of the year as the country deals with the outbreak and repercussions from the trade war with the United States. Additionally, the spreading virus is causing global growth to slow, and the downside risk for 1Q 2020 economic growth is now significant as the virus spreads to India, South Korea, and Italy.

Leading up to the spreading of this dangerous virus, we believe we are in the midst of a downturn in credit quality for U.S. companies. One of the biggest factors contributing to the deterioration in credit quality is the low level of interest rates and tight credit spread environment. These combined factors allow corporations to borrow money at an absurdly low cost, which then allows the company to repurchase its stock and contribute to the increased balance sheet leverage. We have seen an increase in the number of companies that are rated BBB and a decline of those rated A over the past 25 years as low interest rates facilitate the increased use of debt.

The increase in the level of debt does not mean a company will default; however, it is a measure of the probability of default. Similarly, high leverage doesn’t lead to the demise in a company’s stock price, however, it will impede financial flexibility when a company’s cash flow declines.

So far this year, S&P has downgraded six securities to below investment grade ratings, representing nearly $42 billion. Last week, S&P downgraded the debt of Kraft Heinz and Macy’s to BB from BBB. At the same time, credit quality is deteriorating, Moody’s Investors Service’s Default Report has the U.S.’ trailing 12-month high-yield default rate dipping from January 2020’s actual 4.2% to a baseline estimate of 3.8% for January 2021.

The fear of the spread of the coronavirus have impacted the travel industry and oil prices significantly as governments implement methods to contain the outbreak. In addition, several sectors of the credit market are showing signs of credit deterioration. These include retail, energy, cable/media, leisure & travel, and manufacturing.

Leisure & Travel

Normally, the leisure and travel industry moves with the global economy. As businesses and consumers tighten their wallets, travel declines, which in turn, negatively impacts airlines, hotels and restaurants. The coronavirus has negatively impacted tourism this quarter. The second largest concentrated outbreak of the coronavirus was on the Princess cruise ship, which was eventually forced to dock in Japan. In order to control the spread of the virus, the Chinese government has restricted the ability for its citizens to leave the country. As a result, Chinese tourism has declined considerably, which impacts the tourism industry in the United States and Europe.

After affirming Carnival PLC A3 rating last September, rating agencies have been forced to reevaluate its credit. Royal Caribbean Cruise Ltd. is also being reevaluated as cruises are increasingly cancelled to limit the spread of the coronavirus.

Energy

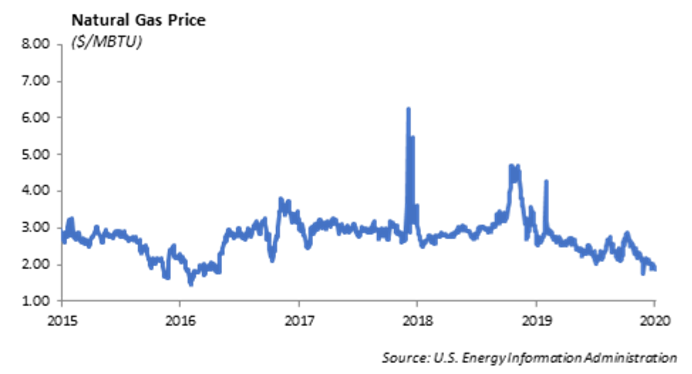

Oil prices have plummeted over 15% since the beginning of the year, reflecting both oversupply concerns and continued weakness from China. In addition, U.S. natural gas prices plunged this month to their lowest close in twenty years. The energy sector is facing serious challenges to refinance over $85 billion in debt coming due over the next four years. Many of the issuers are high yield credits and include: Antero Resources, EQT, and Chesapeake Energy.

We expect to see energy companies take steps to preserve liquidity and pay down debt in order to maintain financial flexibility. In January, after issuing $500 million in 10-year maturity debt, Range Resources (B1/B+) tendered for debt coming due in 2021 and 2022 and suspended its dividend. The company indicated that it was prioritizing its cash flow to pay down debt. We expect to see more companies in the energy sector take steps to shore up their liquidity and maintain financial flexibility.

Retail

Traditional “brick and mortar” retail has been in decline over the past ten years as consumers have increased on-line purchases at the expense of going to shopping malls. The shopping mall experience is transitioning away from retail and towards more restaurants and entertainment. As retail companies struggle to survive, asset sales are being used to restructure balance sheets.

Cable/Media

The cord cutting in the cable industry will continue at a rapid pace in 2020. Traditional cable companies are transitioning into internet providers. However, Dish TV, which has experienced a rapid decline in its subscriber base, does not have a robust internet solution.

Manufacturing

Auto Industry

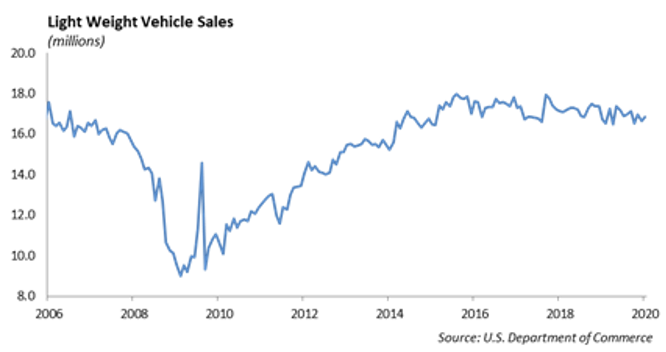

The domestic auto industry has remained at around 17 million light weight vehicle sales for the past five years. Last year, Volkswagen, Nissan, and Ford announced lay-offs in order to cut costs. The credit trends in the auto industry will remain negative in 2020. In September, 2019 Moody’s downgraded the senior unsecured rating of Ford Motor Company from Baa3 to Ba1. Earlier in the year, General Motors weathered the strike with the UAW and has been able to maintain its Baa3/BBB- ratings.

Boeing

The production halt of the 737 MAX has an obvious negative impact on Boeing’s credit profile. We expect Boeing to take on an additional $15 million of debt this year to its current $10 million of long term debt and Boeings long term credit ratings to be downgraded to Baa1/BBB+ from A2/A.

The downstream impact of the 737 MAX Shut down will hurt the credit profile of Spirit Aerospace. We do not expect a decline in the credit ratings of General Electric which makes the engines for the 737 MAX.

Equities

For the shortened week, the DOW was down 1.4%, the S&P was down 1.3%, and the Nasdaq fell 1.6%, with most losses coming on Friday. Year to date, the S&P is still at a gain of about 3.3%. We’ve had a nice rebound after the initial virus fears, but it seems cases outside of China are now causing concern. Over the weekend, South Korea reported over 750 cases of coronavirus, and Italy reported 130 cases and 3 deaths. Many companies, including Apple, have already cautioned that their March quarter could be impacted by slower sales and supply chain disruptions. Apple said they don’t expect to meet their second quarter forecast, with supply shortages and a slower return to normal conditions in China.

There has been a lot of disparity in the market, while stocks are still near all-time highs, the rise of gold suggests increased fear. With stocks at highs, we don’t believe the risk of a worsening outbreak has been priced into the market.

437 companies in the S&P have announced 4th quarter earnings, with 71% exceeding expectations. The rise in 4Q EPS is now expected to be 3.2%, improving again from last week and doing much better than the 0.3% decline expected at the start of the quarter.

Walmart: Earnings and revenue missed expectations. Earnings of $1.38 missed by 5 cents, while Revenue of $141.67 billion was up 2% but missed the $142.49 billion expectation. Weakness in retail continues after Target released its report as well, specifically WMT blamed weakness in toys, apparel, and video games. Same store sales were up 1.9% vs. the growth of 2.3% expected. Sales at Sam’s Club were up just 0.8% on weak tobacco sales. On the bright side, E-commerce sales were up 35% with strength in grocery. The stock was up with all of this news, most likely given the low expectations after the response to Target Macy’s and Kohl’s earlier this year. Year to date, Walmart is down about 1%. Trailing 12 months, the stock is up 18%, and still just off of all-time highs.

Fixed Income

Rates seemed to continue their momentum towards zero as economic data began to weaken. The 30-year treasury hit all-time lows, falling below 1.90% before ending the week at 1.91%. Global rates lagged the decline in US rates. While the US 30-year usually trades 2% higher than the German 30-year, it currently has a premium of 1.86%.

With rates on the decline, spreads have widened, but corporate credits have performed fairly well with index spreads still below 100bps. New issuance has remained heavy; however, once issued, they have not performed well. 70% of new issues over the week were trading wider than issue by week’s end. We continue to like credit as spreads have widened, particularly in higher quality credit. Over the past two weeks we have increased our credit exposure and increased duration in anticipation of continued lower interest rates. As the global economy continues to show cracks, we see little reason for rates to move meaningfully to the upside.

In fixed income markets, we continue to see hidden risks in the indexes which money managers are investing to. Duration of the Aggregate and Corporate index have continued to extend over the past several years with rates and coupons declining. The Agg now has a duration of roughly 6 years and the Corporate index is above 8 years. Further we have seen the average price of bonds within indexes increase substantially. The average price of corporate bonds 10 years and out is now above $117. These factors lead to a further asymmetry of return possibilities, where upside is limited and downside can be substantial. Investors into passive ETF’s generally take indexes at face value and are unaware of these structural changes.

High Yield

Just as investors began to think that coronavirus concerns had mostly died down, news of infection in Japan, South Korea, Singapore, and Italy reinvigorated those fears, resulting in a real effect on credit markets. The high yield index saw 10 bps of widening, absorbing all of the spread widening from the rally in treasury yields. We would expect spreads to be even wider, but due to yields being so low, investors are unwilling to let go of the current yield that they do have. This is evidenced by the resiliency shown by CCC’s. They were the “outperformer” in high yield despite widening out 5 bps on the week. The total index is a modest 7 bps wide of year end levels. Primary markets were slower last week and are expected to be this week as well, which should at least support spreads in the short term.

In energy markets, prices bounced back well. Crude oil was up 3% and natural gas was up 4% as indications that OPEC is considering additional supply cuts in response to coronavirus and outages in the Libya and Venezuela. This morning it looks like all of those gains are going to be erased as coronavirus concerns have picked right back up. There are also concerns that Saudi Arabia and Russia are considering breaking their supply cut alliance, which would be a strong negative to energy prices.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.