Continuing to Navigate the Coronavirus

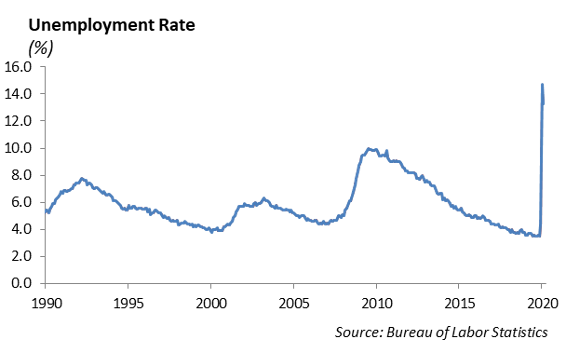

After hitting an historic rate of 14.7% in April, unemployment retreated to 13.3% in May, which was a significant surprise in an economy decimated by the coronavirus. Economic demand will be a function of the movement of the COVID-19 virus. Even though the number of coronavirus cases is declining, we are concerned that the risk of a spike is high over the summer as people emerge from social distancing and seek normality in their lives.

The employment report from the Labor Department indicated that after two months of massive reductions in labor, employers added over 2.5 million jobs in the month of May. It is amazing how quickly we moved from some of the best labor conditions to the worst employment market since World War II. Just last quarter, we were discussing comparisons to the low unemployment rate of 3.5% compared to 50 years ago. We expect it will take several years for the labor market to return to below a four percent unemployment rate.

The ISM reported that its index for nonmanufacturing activity climbed to 45.4 from 41.8 in April, another indication of a revival in economic activity.

Europe – Another Bold Step

The European Central Bank announced a significant increase to its existing bond purchase program by increasing bond buying to €1.35 trillion. The euro rose to its highest level relative to the U.S. dollar since March. The Eurozone economy was fragile heading into the pandemic, and it has been hit extremely hard as a result of the coronavirus. The ECB indicates that GDP will likely contract by -8.7% this year. The increase in bond purchasing is a strong move by European leadership, which typically waits until the last minute to address difficult decisions.

European leadership is still grappling with the decision to issue euro denominated debt. This move would require the European Union to address a common tax authority to support the repayment of debt. They would also need to address the mechanics of distributing and managing proceeds from the debt. In other words, pulling together a fiscal union across sovereign countries with different political systems and social welfare programs will be very difficult.

Equity

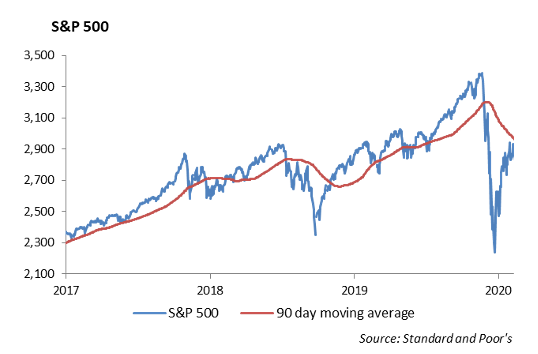

Since the lows of the market crash on March 23rd, the S&P 500 Index is up 39%, and it is down only -1% year-to-date. The index is currently at 3193, which is only 6% off of all-time highs. The DOW is down -5% year-to-date and the NASDAQ is up 9% year-to-date and very close to all-time highs. There was a significant shift in sector performance last week. Information Technology still leads, up 11% year-to-date. However, Consumer Discretionary is now up 6.5% year-to-date.

We continue to see a shift into beaten down sectors. In just the past 30 days, Industrials, Financials, Energy, Materials, and Consumer Discretionary are all up 15-20%.

Five Stock Picks for a Recovery

Southwest Airlines Co (LUV)

Southwest Airlines has a very strong balance sheet, and it is an industry leader trading at a discounted price. The company is very consistent company in generating profits, and in the last 10 years, they have grown revenue by 8% compounded annually. In addition, their free cash flow has been positive for 9 out of the last 10 years. For the trailing 12 months, they generated a substantial $2.1 billion in free cash flow. Of the four largest airlines, Southwest has the highest return on invested capital at 12%. Although there is a short-term impact in air travel demand, the overall growth of the economy will lead to a rebound in the airline industry. As air travel gradually returns, it appears that domestic travel will be the first to return as many international borders remain closed, and Southwest’s revenue is primarily generated from domestic flights. The company has the best downside protection compared to other airlines with ample liquidity, highest market share, and most profitability. The stock is down -30% year-to-date. We believe this is a good pick for a recovery in a diversified portfolio.

Ford Motor Company (F)

Auto sales over the past five years have been consistently above 16 million units annually. The pandemic cause a dramatic drop in sales to below an annualized rate of 8.58 million units at the end of April. Ford is one of many global automakers experiencing extreme stress as a lack of revenue, high debt, and a general lack of liquidity drove the stock down by more than -50%. While we expect negative company earnings through 2020, we are modeling a return to profitability in the second half of the year and earnings per share of $0.50 through 2021 as overall consumption returns to normal. At 14 times forward earnings, we believe Ford’s valuation makes it a tactical buy for the next six to twelve months. However, we expect the company’s culture and broken business model will challenge Ford from remaining a long-term holding.

AT&T Inc. (T)

AT&T is down -16.15% in 2020, with underperformance driven by a halt in box office sales out of WarnerMedia and increased churn rate in the mobile segment due to the higher unemployment rate. With AT&T trading at 10 times forward earnings of $3.35 in 2021, we believe it is a good buy right now for three reasons. First, the pandemic has accelerated the move towards digital media due to social distancing, and the combination of Turner, Warner and HBO media catalogs give AT&T a solid footing in the shift. Secondly, we still believe 5G will drive incremental growth starting in 2021, and AT&T’s low band spectrum build up is well above all competitors aside from the T-Mobile post-merger. Lastly, AT&T’s dividend yield of 6.35% is adequately covered by over $25 billion in free cash flow, pays investors while we wait for a recovery and mitigates price volatility.

U.S. Bancorp (USB)

U.S. Bancorp is down -28% year-to-date as a heavy reliance on mortgages and wealth management have led to the bank being one of the worst performing large cap banks in the S&P 500. U.S. Bancorp is the 5th largest US bank and is well capitalized with a CET1 ratio of 11%. While home buying and mortgage application understandably dropped sharply in March, the MBA US Purchase Index has already recovered to above 2019 levels. Wealth management now accounts for roughly 15% of U.S. Bancorp’s revenue. This creates sensitivity to global equity markets, but as the S&P 500 and Nasdaq are now both positive on a total return basis for 2020, we believe this will boost earnings for the second half of 2020. We believe 4% dividend is currently safe, which adds to the long-term benefit of owning USB.

Tyson Foods, Inc. (TSN)

Tyson Foods is down -28.69% in 2020, as food service company demand has shrunk and contaminated hog farms were forced to terminate product. In the long run, we believe overall meat consumption should not be meaningfully impacted by COVID-19. We expect 2020 earnings to be $4.50, and at 14.50 times forward earnings, we see Tyson as a tactical relative value investment. Long-term, we believe that the commodity-based meat industry will continue to see margin pressure, and therefore, we would buy Tyson as a short-term recovery play.

Fixed Income

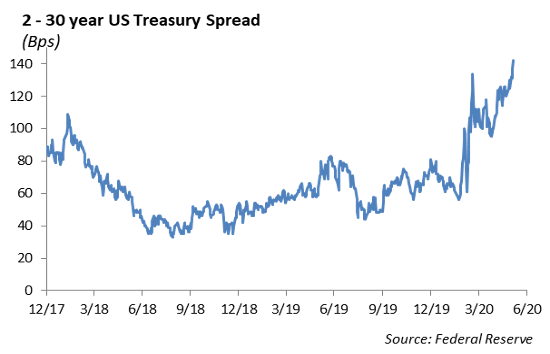

U.S. Treasury rates rose significantly over the past week, from 0.65% to 0.90% as investors moved back into a risk-on mode. Overall growth and inflation estimates across Wall Street rose as the employment picture was better than expected, and COVID-19 death rates were lowered by the CDC. Overall, we still believe that the consumer is not as strong as the consensus believes, as the lagging effects of over 15% unemployment and a halt in global spending still have not completely materialized in economic and earnings data. Regardless, the 2-year to 30-year treasury curve steepened 25bps through the week, a firm representation that the bond market believes the economy is back to normal growth. While this week’s move was large, it is important to remember where we have come from. The 30-year U.S. Treasury at 1.66% is still 100bps lower than this time last year.

Corporate credit followed the equity markets over the week as the Bloomberg Barclays Corporate Bond Index tightened by 25bps through the week. Industries such as autos, airlines, and hospitality, who largely have not recovered from the pandemic sell off, began to tighten sharply. 10-year Delta bonds rose 10 points and tightened 140bps, while Ford 10-year bonds tighten 130bps. While we largely remain overweight to credit across total return fixed income strategies, we continue to incrementally sell outperforming credits as markets tighten. While riding the coat tails of the Fed’s corporate bond purchases has provided low volatility returns, we remain focused on fundaments. The fact remains that leverage has meaningfully ticked up, corporations have used up free cash, and CFO’s are pulling every lever in the tool box during this cycle turn. We intend to lean into our defensive position across all portfolio’s as risk markets once again look overvalued.

High Yield

High yield credit tightened by 100 bps, last week, and the CCC tranche tightened over 175 bps. The index is just under 200 bps away from year-end 2019 levels. In addition, BB credit performance turned positive last week and is now up 1.72% year-to-date. Possibly the best news for junk credit investors was the recovery seen in the various energy sectors.

Energy credit had a positive week as well, with oil up to almost $40 a barrel. Midstream companies tightened 82 bps, independent energy companies tightened 143 bps, and oilfield services tightened almost 300 bps. For example, Continental Resources’ 2044 dated debt opened this morning at $78.50 on the bid, which translates to +505/30yr in spread. In contrast, lows were under 40 cents on the dollar and spread over +1200/30yr in late March. The current levels appear to provide an opportunity to take risk off in the energy sector; however, the market seems to still be tightening. Without an early second wave of the coronavirus, we would expect Energy companies continue as the best performer in high yield. We would expect the Technology, Media, and Telecom (TMT) sector would continue as the worst performer, based on their relative defense from the blow out in March and April.

As expected, funds inflows for high yield ETFs and mutual funds continued their 10 week winning streak, bringing in $5.8 billion last week.

The primary market continued their activity, pricing in excess of $12 billion into the market. High yield new issuance is up almost 60% over this respective time period last year. Royal Caribbean re-entered the market, offering $1 billion of 3-year secured notes to keep the cruise line business afloat. L Brands ran a two part deal, offering both secured and unsecured 5 year notes. The bonds were highly attractive to high yield investors, as each offering is up more than 5%. Altice and Univision both offered large deals to the market as well.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.