Continuing to Navigate the Coronavirus

In order to begin to understand the capital markets, we must first acknowledge that we are living through not one, but two experiments. The first experiment is the extreme monetary policy that has been applied to help stimulate economic growth after the halt in economic activity due to the coronavirus. These additional monetary programs only build on the stimulus that was introduced after the Financial Crisis in 2008. The second experiment we are experiencing involves the government’s actions to control the spread of the coronavirus, which include closing businesses, wearing masks, social distancing, and working from home.

The ramifications for investors are nothing short of significant. Earnings projections for many companies are nearly impossible to estimate as supply chains have been disrupted, revenue cannot be estimated, and in some cases, the company can’t measure its operating margins. In the absence of a vaccine, we expect to see a surge in cases as we move to reopen the economy. It’s like we’re in a gun fight, but all we have is a paper bag and a stick. The intersection of normality and fighting the virus with only a stick in our hand the collision of economic ruin.

The impact of the pandemic goes beyond company earnings. There is still little clarity on how to facilitate large gatherings in a way that won’t further the spread of the coronavirus. State and city financials will be negatively impacted as tax receipts come in significantly lower to support operations and debt service. Colleges and Universities are challenged to reduce costs in the face of uncertainty around the fall semester.

Even if a vaccine was available today, it would still take two years for companies to reassemble supply chains, for the labor market to show some stability, and for aggregate demand to approach prior levels. We have begun a long period of economic recovery that, at best, will last two to three years. Chairman Powell’s assessment last week was more sobering, indicating the economic recovery could last well into the decade.

Monetary Policy Does Not Equal Economic Recovery

Following the Financial Crisis, the economy lost over eight million jobs. It took the seven years to rebuild the economy and put eight million people back to work. In fact, by the end of 2019 the economy had created over 22 million jobs since the low point reached in 2010. Many of these new jobs were in the hospitality and service industries, which are being decimated now as a result of the virus.

The Federal Reserve and Treasury Secretary have moved quickly to establish programs for an economic recovery. However, do not confuse an aggressive monetary policy with economic recovery; they are two different things.

One of the critical things we believe that is needed for sustained economic recovery is a coordinated plan for economic growth. The coordinated private-public sector plan should go beyond giving people money, and rather focus on creating stable jobs and growth. We are in an unprecedented period of the economy, and the monetary policies are a new experiment.

Investment Strategy

Investors in equities should remain focused on domestic large cap. We are constructive on technology, healthcare and communications.

We are underweight international and severely underweight emerging markets. Within emerging markets, the top seven countries are either in political turmoil, recession or both.

We still like investment grade bonds. We expect continued credit deterioration and investors need to be cognizant of the heavy debt load many companies have taken on during the pandemic.

Equity

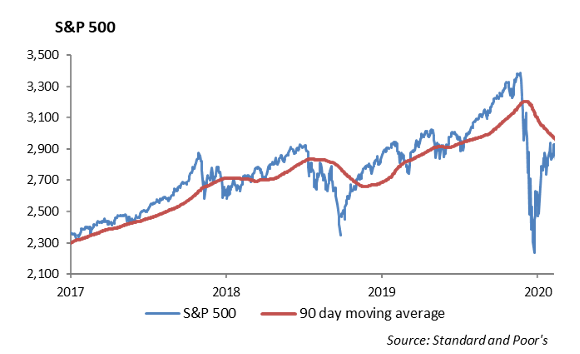

Last week, equities revealed a tale of two very different markets. On Wednesday, the S&P 500 recovered all of its 2020 losses and closed positive for the year. However, the market jubilation hit a wall the following day, and global markets were down over -5% for the day. The Dow Jones Industrial Average dropped over -1800 points, and the CBOE Volatility Index spiked once again to over 40.

We continue to see a substantial sector rotation. Investors have begun selling stocks in industries that have led the recovery and reallocating to the sectors with lagging price performance. Health care and technology stocks have pushed the S&P 500 back to all-time highs, but over the past 30 days, they have been the largest laggards. Financials and Industrials, who have generally lagged the recovery, are now up over 15% in the past month.

We continue to believe that we have entered a sustained period of heightened volatility. Markets are now pricing in 1-year volatility to remain above 30. In attempt to lower overall risk across equity and asset allocation models, we are reducing the weights to both domestic and international equities and increasing our allocation to low volatility ETF’s, such as iShares Edge MSCI Min VOL (USMV). This fund provides downside protection, with a downside capture of 70% of the S&P 500, without forfeiting too much upside with a capture of 90%. This ETF remains relatively equal weight across sectors when compared to the S&P 500.

Fixed Income

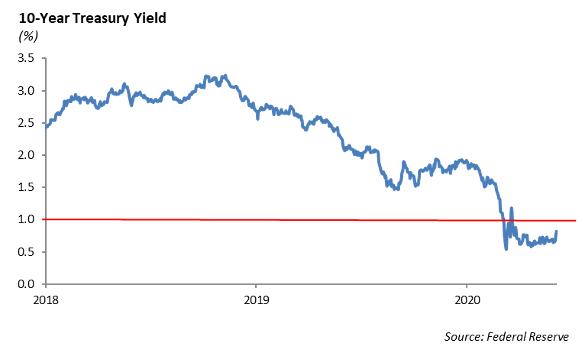

Interest rate volatility increased last week as the sharp decline in the stock market once again led investors to low risk assets. The 10-year U.S. Treasury declined from 85bps to 70bps over the week, and interest rates across the globe followed suit. The 10-year debt of Germany, France, and Japan all remain negative yielding. The total negative yielding debt across the world rose above $12 trillion after dipping below $8 trillion in March.

The risk off mode of global markets caused credit spreads to widen by generally 10bps. New issuance has remained strong, but new issuance concession was non-existent, and several issues traded wider post launch. Overall, we continue to make tactical trades around primary market issuance, and we are incrementally reducing credit exposure across fixed income portfolios. In credit, we are seeking quality by buying the debt of companies with sound balance sheets and business models that can weather another potential wave of COVID-19.

While many sectors across fixed income have recovered most of the market shock in March, others have struggled to recover, including airline oriented bonds, commercial mortgage backed securities, and collateralized loan obligations (CLO’s). We think the underperformance in these sectors will likely continue. The near term future of airlines remains in question as reduced seat capacity, high fixed costs, and unpredictable consumer behavior are all significant headwinds to recovery. We believe the shock to the CMBS market has not yet been fully realized as retail and restaurants are slow to open and businesses begin to scale back the amount of office space required to operate. Finally, CLO’s are facing pressure as the chance of default correlation has increased significantly with retail, restaurants, and energy business models under significant stress. We generally do not believe the large spreads in the asset classes gives investors enough compensation for the risk taken. We continue to move up in quality across fixed income portfolio’s as spreads have tightened back to historic levels.

High Yield

High yield investment activity reversed sharply last week compared to most of May and the beginning of June. The Bloomberg Barclays U.S. High Yield Index widened by 75 bps, dispersed fairly evenly among the rating groups. The index is still over 24 bps tighter this month.

Despite the risk of sentiment, high yield funds inflows remained positive for the eleventh consecutive week, although the income $5.1 billion was modestly lower than the prior week. The continued fund inflows raises the question: who are the players buying these ETFs? The Fed’s purchasing program is certainly helping, but it does not explain the significant winning streak for high yield funds.

Much like investment grade credit, high yield primary issuance slowed to a halt late last week. Before Thursday, however, the market priced $9 billion in high yield new supply. We saw a mix of quality come to market: American Axle’s $400 million represented the B tier, while Sirius XM’s $1.5 billion and International Game Technology’s $750 million represented the BB tier.

Energy

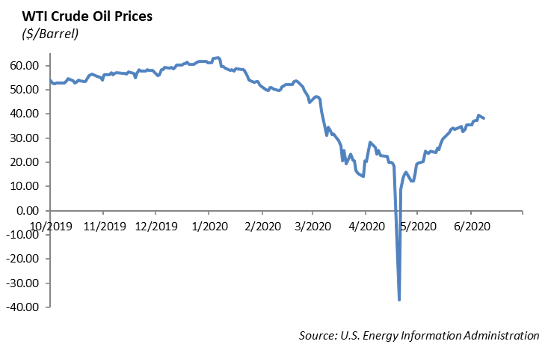

Energy markets also fell last week. WTI crude oil fell -8%, the first meaningful decline for almost two months. Oil prices are still far from their March and April lows. WTI opened this morning at just over $36 a barrel. The fall in prices last week can be attributed to changing demand sentiment. Supply seems to be under control for both OPEC+ and American oil, but the fears of a second wave of the coronavirus has definitely impacted global growth.

WCM Summer Reading List

The Trouble with Gravity by Richard Panek

Thinking Fast and Slow by Daniel Kahneman

Misbehavior of Markets by Benoit Mandelbrot

Siddhartha by Herman Hesse

Catch-22 by Joseph Heller

Hedgehogging by Barton Biggs

Warning by Anonymous

7 Men and the Secret of Their Greatness by Eric Metaxas

Cat’s Cradle by Kurt Vonnegut

The Silent Patient by Alex Michaelides

Managing Humans by Michael Lopp

Success Mindsets by Ryan Gottfredson

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.