Continuing to Navigate the Coronavirus

Countries, states and cities around the world are trying to restart their economies following a two month shut down to control the spread of the coronavirus. We are in a precarious period. The rate of infection is declining, people are beginning to gather more, and there is no vaccine to prevent the spread of the COVID-19 virus. The risk of an increase in the rate of coronavirus infections appears to be high, given the demographic challenges. Amidst all the anxiety around the virus, the economy, and increased tensions with China, the SpaceX Falcon 9 successfully launched two American astronauts to the space station last weekend, the first launch since the space shuttle was retired 10 years ago.

The Federal Reserve

The Federal Reserve has pumped nearly $4 trillion in stimulus into the U.S. economy. However, do not confuse stimulus from the Federal Reserve with an economic recovery. The stimulus is the lubricant that greases the gears turning in the economy to help it run smoothly. The gears in the global economy are rusty with increased debt burden, high rate of unemployment, and an increase in business closing and bankruptcies. This puts pressure on consumer confidence, consumption, and business investment. Some of the stimulus, including paychecks to individuals and the payroll protection program, has run its course. We expect a slow and weak recovery as the demand curve shifts lower and businesses right-size their labor force and reduce investment.

As part of the stimulus initiative, the Federal Reserve began purchasing investment grade and high yield corporate debt through its two newly formed bond buying programs: the Primary Market Corporate Credit Facility (PMCCF) and the Secondary Market Corporate Credit Facility (SMCCF). While the Fed can purchase corporate bonds directly, it chose to make the initial purchases through exchange traded funds. This is controversial since purchasing the debt of corporations can be viewed as an endorsement to support the company’s financial position and runs counter to the spirit and rules of the Federal Reserve charter established in 1913.

We have moved into a new monetary regime in which the Federal Reserve utilizes an expanded tool kit in an effort to prop up the economy and avoid a deep cyclical downturn. This new tool kit moves beyond, targeting the level of short term interest rates or excess reserves. This tool kit utilizes the entire balance sheet of the Federal Reserve and its ability to purchase securities in the open market to influence the risk free rate curve as well as credit curves

China Moves to Increase Control of Hong Kong

China took a bold step last week to exert more control and influence in Hong Kong. As part of the treaty with Britain in 1997 to move Hong Kong back to Chinese rule, China agreed to a 50 year period where Hong Kong would exist as a democracy alongside of communist China. One country, two systems. However, that changed this past week with China pushing legislation that would effectively give it more control over the region. Up until this time, the U.S. provided Hong Kong with special status since it operated independent of China with its own legislature and laws. However, the U.S. no longer certifies Hong Kong as independent from China and has taken steps to revoke its special status which includes trade agreements.

This is one more pawn in the deteriorating U.S. – China relationship.

Europe – Their Hamilton Moment

As the first Secretary of Treasury, Alexander Hamilton is credited with establishing a common currency, the dollar, for the United States. He also created federal debt, effectively creating the U.S. Treasury bonds to assist in the financing of the war. Eventually Treasury bonds would be used to support government operations and building infrastructure for the new country under a centralized taxing authority. The structure Hamilton created in 1790 still serves as the foundation for our financial system today. And, he did it in five years.

The European Central Bank (ECB) is the central bank for the European Union. It serves as the central bank of the 19 European Union countries which have adopted the euro with the main task to maintain price stability in the euro area and preserve the purchasing power of the single currency. Up to this point, the EU has relied heavily on the ECB to provide economic stimulus through easy monetary policy and bond purchase programs.

However, the European Union is not a Federation like the United States. Members of the European Union are sovereign countries with their own debt, their own fiscal budgets, and their own taxing authority. Because each country has fiscal autonomy, it has been difficult for the members of the EU to coalesce around an initiative to centralize debt borrowings which would be another mechanism to provide much needed stimulus.

Last week, the European Commission proposed a €750 billion debt offering that would help provide economic stimulus for European economies devastated by the coronavirus pandemic. This is an attempt to provide centralized debt financing under the euro currency. This is Europe’s Hamilton Moment.

Unfortunately, without common governance and taxing authority to provide a means to set fiscal priorities and accountability, euro denominated debt issuance is a road that is fraught with danger for the EU. Under the current system in which there is little consequence to be out of compliance with fiscal requirements laid out in the European Union Treaty, the risk of a growing debt without rules to pay it down appears high.

Equity

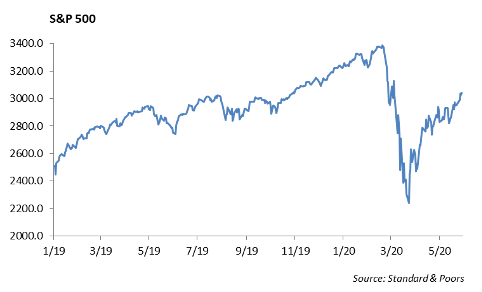

The S&P closed out the month of May with a 4.5% gain. The NASDAQ finished with a gain of 6.7%, and the Russell 2000 finished with a gain of 7%. The S&P is now down -5.7% year-to-date and up 9.3% over the last 12 months.

The Technology sector has shown the most strength for the year relative to other sectors. Some of the lower-performing sectors are showing more strength recently, as Energy and Materials are now trending up. Last week, Financials and Industrials broke out and broadened the stock market rally. Both sectors were up over 6% during last week alone. Although we are seeing a trend to shift to more beaten down sectors, we still believe that the high performing sectors will continue to perform in this environment. Technology and Health Care sectors have both reported solid earnings, and many companies have even raised earnings guidance for next quarter. Market recovery and sector performance has been driven by the “stay at home” order, and we believe that the effects of this movement will continue into the next quarter.

Our top holdings include MSFT, AMZN, FB, GOOGL, PYPL, CRM, and ADBE. All of these holdings have been solid COVID plays in which the business model was not affected as they never had to close business operations and remained beneficiaries of the increased demand in their products. Additionally, the downside risk to these names is less severe, and we believe these names will continue to perform. Many of these stock picks are in our Focused Growth portfolio, which has outperformed the S&P by 18% year-to-date.

Two Winthrop Equity Strategies received PSN Top Guns Awards for performance in the first quarter 2020. Our Large Cap Blend Strategy was awarded 4 and 5 Star ratings, and our Focused Growth Equity Strategy was awarded 1 and 2 Star ratings.

Portfolio Models & Asset Allocation

While the Nasdaq 100 and S&P 500 indexes have both recovered over 30% from their March lows, many investments remain down significantly over the past year. Large cap equity markets have been largely driven by the top 10 largest companies, which now make up a quarter of the index. The returns driven by domestic large caps have become extremely divided. While growth and momentum factors have positive total returns in 2020, value and high dividend have -20% total returns for the year. Energy is the worst performing sector in the S&P 500 index, and financials are still down -25% year-to-date. Small cap and international stocks continue to underperform large cap stocks. The Russell 2000 index, MSCI EAFE, and MSCI Emerging Market Indexes are all down over -15% year-to-date.

Underperformance does not imply that the lagging markets are cheap. The Russell 2000 is now trading at 52 times earnings, which is a 5-year high. The MSCI EFA is trading at 22 times earnings, which is the same level it traded at in December 2019 and is more expensive than the S&P 500. The S&P 500 is also expensive, trading at 21 times earnings. The velocity of the equity market recovery reveals that investors are dismissing the bleak earnings expectations for 2020. We believe that markets are relatively overvalued, and therefore, we’ve been actively reducing equity volatility across portfolios. As the economy navigates a period of negative growth and slowing inflation, we continue to be buyers of Technology, Healthcare, and low volatility large cap equity funds.

Fixed Income

Interest rates were effectively unchanged through the week. The 10-year US Treasury ended the week at 65bps. Short-term interest rates remain anchored to any changes to Fed policy. Corporate spreads tightened over 10bps through the week as the primary market was active but much smaller in scale.

The Federal Reserve finally announced its current purchases of $1.3 billion corporate bond funds last week. The size of the current purchases is minuscule relative to the $3 trillion the Fed has bought across other assets in the past month. The majority of the $1.3 billion was used to purchase the highly liquid iShares Investment Grade Corporate Bond ETF (LQD). The Fed also purchased $100 million of high yield in the iShares High Yield Corporate Bond ETF (HYG). While the move by the Fed to begin buying bond ETF’s is unprecedented worth noting, their daily purchases were less than 0.50% of the daily volume – hardly enough to move the market in any direction. We believe the real intent of their purchases was to solidify the Fed’s willingness to act on any measures needed to support the financial markets.

We believe the support of the Fed in the bond markets will help reduce overall volatility in the near term. However, we are entering an entirely new regime of monetary policy experiments that will take some time to determine the side effects. The market recovery has led investment grade spreads to tighten rapidly, and we continue to move up in quality both in ratings and in industries across our fixed income strategies. We generally like A-rated credits in the technology and banking sectors, and we are sellers of higher beta sectors such as energy, airlines, and hospitality.

High Yield

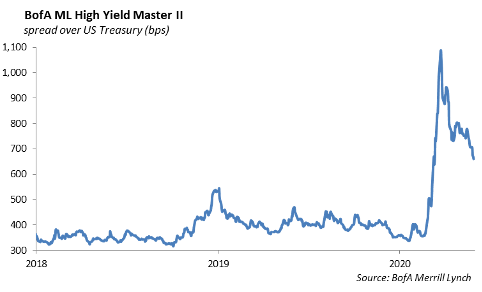

The month of May ended strong for high yield credit investors. The index tightened 35 bps with risk outperforming relative safety. The index has tightened over 100 bps in the last two weeks, and is now only 300 bps wide of year-end 2019 levels, from 725 bps wide levels in March. For 2020, the index is now down less than -6% total return, with BBs down less than -2.5%. As supply starts to taper off in the summer months, expect high yield to tighten further barring cataclysmic bad news in re-openings and vaccine development.

Retail investors continue to be bullish on junk credit. Fund inflows were significantly positive for a ninth straight week, and inflows topped $6 billion. The Fed has only purchased $3 billion of both Investment grade and high yield ETFs over the last 3 weeks, indicating that independent investors are the key drivers to tightening spreads.

The high yield primary market remained robust with $12 billion of new issuance. Total May issuance was $44 billion, making this the third busiest May recorded. A mix of low treasury yields and the need for liquidity due to COVID-19 has led to heavy issuance – both in high yield and investment grade. Macy’s was upsized their offering by $200 million dollars to $1.3 billion. The company’s 5-year note came in at 8.375% after initial price talk closer to 8.5%. Demand for the bond has remained strong, and they are now bid with a point premium in the open market. The issuance was rated BB by credit agencies despite being backed by real estate collateral. The funds were used to repay their credit facility and to pay their vendors. Macy’s is expected to negotiate a new bank line backed by inventory to further enhance their near term liquidity. In other new issuance, a flurry of healthcare names came to market, including Molina, DaVita, and Ortho-Clinical Diagnostics.

Energy

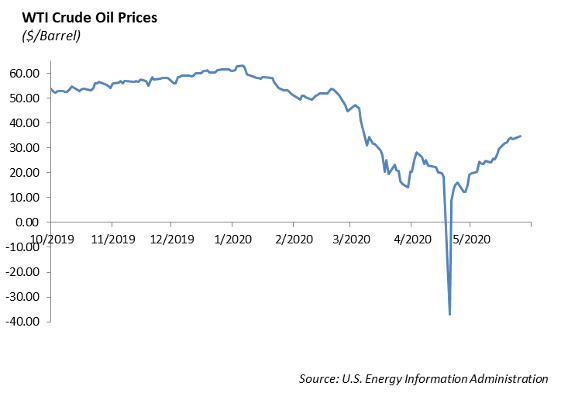

WTI crude oil rose 7% and now sits above $35/barrel. This has caused recovery amongst many of the high yield exploration and production companies. Apache, Continental Resources, and Occidental credit all rose last week with oil prices. It will be important to watch these credits this week as OPEC+ is expected to increase July production by 2 million barrels a day.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.