Time to Reassess

As we near the mid-point of the year, it’s time to evaluate our investment themes and assess our investment strategy heading into the third and fourth quarters. Investors benefited from the capitulation trade early in 2019; however, underlying fundamentals and security valuations will be critical for the second half of the year.

- In spite of the impressive employment reports, the domestic economy is slowing. When adjusted for inventory accumulation and trade anomalies, we expect normalized GDP growth to be growing around 1.8% in 2019. This is substantially lower than the 3.1% 1Q 2019 revised GDP report. Across major segments of the economy, including autos, real estate, manufacturing and agriculture, the domestic economy is showing signs of slowing. Annual auto sales are running at $16.5 million, but production has declined. While this is still a healthy clip, we expect the decline in auto production to marginally impact the economy. Auto inventories are dropping sharply. In June 2017, dealer inventories were 1.2 million units, and today they are near 700 thousand, according to data from the Federal Reserve.

- The trade war with China has contributed to a slowing domestic economic growth rate. For example, we would typically expect China to buy over 65 million tons of U.S. soybeans; however, their purchases have nearly stopped. As a result, U.S. soybean inventory is poised to reach an estimated 955 million bushels in 2019, nearly doubling the 2018 stockpile. Effectively, we have over a two year supply of soybeans before farmers go to plant in 2019. We are expecting a slowdown in agriculture equipment sales as farmers are holding off on investing in new equipment.

- Brexit is not going to be easy. After three years of negotiations, it has become more apparent that an answer is not going to magically appear out of thin air. With Prime Minister Theresa May resigning, a new government in Great Britain will need to be formed. Once formed, the government faces a bi-furcated decision: Britain leaves the European Union and deals with the consequences of an abrupt exit, or Britain takes another vote. Either way, the Brexit affair at this stage is an overhang to both Europe and the United Kingdom’s economic growth.

- Up to this point, the capital markets have navigated the economic uncertainty fairly well. At its peak, the S&P 500 was up nearly 14% in 2019. However, volatility has increased with the recent uncertainty in the U.S. – China trade deal and the new threat of tariffs on Mexico. Domestic equity, measured by the S&P 500, posted its worst month of May performance in seven years.

- The credit markets are under pressure. Wall Street appears to be long credit, and redemptions from credit-based Exchange Traded Funds have contributed to the pressure on spreads. Liquidity in the bond market has declined with even high quality investment grade bonds more difficult to sell. This will be an important theme in the second half of the year.

- With the growth in structured securities, collateral is in high demand. Commercial Mortgage Loans, leveraged loans, and middle market loans are being underwritten at a hectic pace, and in turn, being packaged up into CLO’s, CMBS, and ABS. The Leveraged Loan market is over $1 trillion and 85% of leveraged loans underwritten are “covenant light” loans. The seeds are planted for a destructive credit market event which will prove treacherous for individual investors as these products and collateral have crept into mainstream traditional mutual fund and ETF’s.

Worth the Watch

This week’s recommendation is not so much a read, but a recommendation to watch. On 60 Minutes last week, Jerome Powell was interviewed along with Janet Yellen and Ben Bernanke. We have experienced ten years of economic expansion following the Financial Crisis, and the collective wisdom from the Fed Reserve Chairs in this interview is worth listening to.

https://www.cbsnews.com/news/jerome-powell-federal-reserve-chairman-60-minutes-interview-2019-06-02/

Federal Reserve – Inflation Remains Below Target

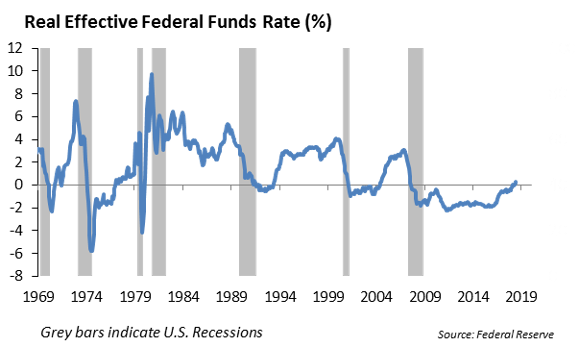

After a weak start to the year, the pace of inflation increased in April as the price index for personal-consumption expenditures rose a seasonally adjusted 0.31% in April over prior month. According to the Commerce Department, this is the largest monthly gain since January 2018. Inflation has been consistently coming in below the Fed’s target of 2%. The slower pace of inflation will provide some cover for the Federal Reserve to begin to lower short term interest rates in the second half of the year, if economic growth slows as we expect. This would signal an important shift in monetary policy. With the slower pace of inflation, the real Fed Funds rate is near zero. Historically, economic recessions don’t occur during periods when the real Fed Funds rate is trading below zero. We expect the economic growth to slow, but not to roll over into recession.

Fixed Income

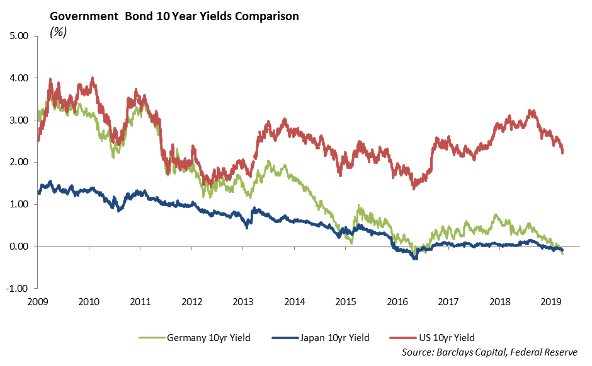

The US trade war continued to dominate headlines over the past week, leading to a significant rally in US Treasuries. Treasuries across the curve tightened 15bps, the 10-year hit 2.16%, and the 2-year fell below 2% as investors moved up in quality. Global yields also fell into further negative territory during the week with the German 10-year at -0.20% and Japan 10-year at -0.09%. The media was focused on the flattening of yield curves when using the 3-month treasury as the basis. However, we believe the 2-year spread to 10 or 30-year treasuries is more telling of economic conditions, and these curves are positive sloping, actually, steepening over the week.

Corporate credit spreads widened through the week, leaving the Corporate index wider by 15bps for the month of May. As the risk off trade consumed the markets, the street was noticeably heavy on credit, leading to difficulty getting a reasonable bid from dealers. Conversely, investors who were buyers of credit were able to find tremendous value. We were net buyers during the week on the long end in Qualcomm, Lowes, Edison International and Mastercard.

Municipal Bonds

Municipals had a strong week, with the AAA muni curve tightening by 7bps, but generally underperformed treasuries. The 30-year Municipal/Treasury ratio saw some relief, moving back to 93%. While municipal yields are low, we still believe they offer competitive tax equivalent yields to corporates for investors in the highest tax brackets.

Taxable municipals have not experienced the volatility of the corporate bond market and are still trading at near their tightest spreads year to date. Currently, 10-year taxable munis are trading inside of single A corporates at 2.80%. At this point, taxable munis look relatively rich and would use their outperformance over the past month to swap into high quality corporates at wider spreads.

High Yield

With the global economic slowdown, interest rates have dropped sharply. Yields on 10-year sovereign debt in developed countries, including Germany and Japan, are again negative.

Last week was the fourth straight week of spread widening in the high yield index. The spread widening has been partially offset in price performance due to the continued drop in treasury rates. US high yield total return was negative with all risk tiers negative, but CCCs did meaningfully underperform its B and BB counterparts. Year to date, CCCs are now the underperformers in the high yield space.

High yield fund flows last week were a negative $1.27 billion, marking the third largest outflow of the year. Last Tuesday, two high yield ETFs, JNK and HYG, both experienced their largest single day outflows since last December, with JNK losing over $400 million and HYG losing over $300 million in a single day.

High yield new issuance slowed to a crawl last week with only $1 billion pricing. Despite this, the month of May still had the highest monthly total since September 2017.

Since the rally in January and February, our strategy in high yield has been to remain defensive with higher rated issuers. We have seen this strategy begin to pay off with BBs now outperforming CCCs year-to-date. We still favor this defensive play.

Equities

For the week, the S&P was down 2.6%, and the DOW was down 2.9%. This continues a 5-week decline as May was the first negative month of the year. As of close on Friday, the S&P is up 9.8%.

As U.S./China talks have become more negative, the focus shifted to Mexico on Friday. Trump announced that he would be adding tariffs on Mexican imports to pressure the Mexican government in helping the U.S. stop the flow of illegal immigrants. The tariffs would start at 5% and reach 25% by October. The market did not take that well, and there was a sell off on Friday morning, particularly in autos. GM fell 5%, Ford was down 3%, and European and Asian carmakers with Mexican exposure were also under pressure, with the Europe Auto Index down 3.2%.

The 200 day moving average of the S&P of 2776 was broken on Friday with the Mexico news. With tariff news and news from the UK that Theresa May is stepping down, there has been a large shift toward defensive sectors, such as Utilities and Real Estate sectors. Due to low investor confidence, many prefer low growth, income producing stocks. Real Estate is now up 17% and is the top performing sector YTD, with 63% of stocks above their 50 day moving average. Now, 75% of stocks in the Utilities sector are above their 50 day moving average, painting a clear picture of the shift that is occurring.

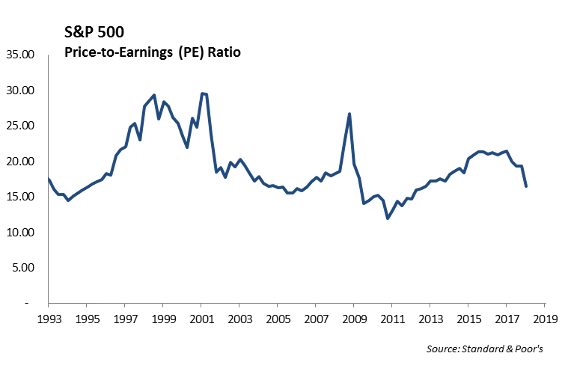

From a price to earnings perspective, Tech’s P/E is 20.4, down from 24.0 in 2018, and the Utility sector P/E ratio is 20.0, which is 5 points higher than the end of 2018. Tech and Utilities are trading at nearly identical P/E ratios.

Retail stocks have been hit hard on earnings news. Specifically, shares of Abercrombie & Fitch and Canada Goose were both down over 20% last week based on weak sales and earnings misses. GAP and Capri were down roughly 15%. As a group, retailers’ earnings are down 24% for the first quarter of 2019, which is the worst earnings since the first quarter of 2008. S&P 500 retail fell 13% in May. This negative news seems to be very focused on mall based retailers experiencing traffic issues, since the consumer is doing well, and WMT and TGT both had solid first quarter reports, with strength in apparel. With the additional taxes on clothing and footwear from China plus the tax on Mexico, there could be additional pressure on these companies. This is a sector to watch carefully heading into the second half of the year.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.