Economic Growth Continues to Slow

The economy continued to show signs of slowing this past week. The U.S. economy, measured by Gross Domestic Product, is shaped by 70% consumer, 18% manufacturing, and 17% government sectors with a net drag of -5% for trade balance. While the government sector is typically pretty stable, shifts in consumption and manufacturing have an impact on GDP growth. According to the most recent data from the Bureau of Labor Statistics, nominal GDP is roughly $19.4 trillion.

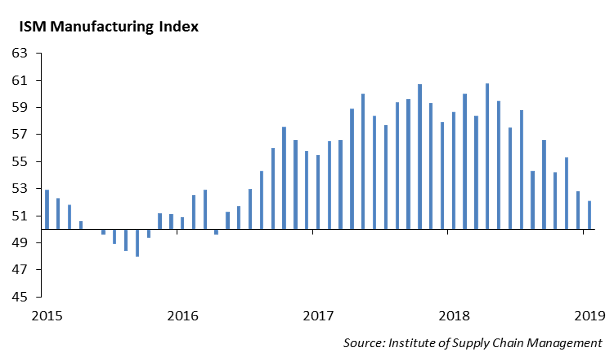

The ISM Manufacturer’s Purchasing Manager’s Index declined to 52.1 in May. While a reading above 50 is still considered growth, the ISM Index was as high as 58 in April of 2017 and declined from 52.8 in April. Last month’s Index was the slowest reading in two years.

The economy added a mere 75,000 jobs in May, as reported by the Bureau of Labor Statistics. The hiring slowdown appeared to be broad based across industries as the unemployment rate remained at 3.6%. We believe the health of the labor market is the key indicator of the next move in monetary policy by the Federal Reserve. The economy has consistently produced an average of over 150,000 jobs a month over the past several years. However, as corporate profit margins are pinched, we expect to see an increase in lay-offs. Last month, Ford announced cuts of 7,000, and last week, Volkswagen and IBM announced cuts of 4,000 cuts and 1,000 respectively. With the slowing in momentum in the economy, the next few months may prove difficult for the labor market.

The President resolved his recent trade dispute with Mexico on Friday through an immigration deal clearing the way to ratify the new U.S.-Mexico-Canada Agreement, which will replace the NAFTA agreement.

Federal Reserve – Lays a Path for a Cut in Rates This Year

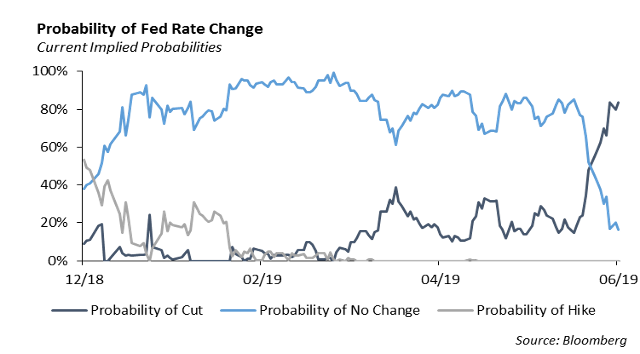

Fed Chairman Powell, in remarks this past week, indicated that the Federal Reserve would consider reducing interest rates if the trade adversity were to have a prolonged impact on domestic economic growth. An escalation in trade tensions with China, Mexico and Europe have arguably been a drag on global economic growth. However, the market reaction to Powell’s comments was favorable as stocks rallied and bond yields remained low. While the curve was inverted from 3 month T-Bills to 5 year US Treasury yields, the curve is positive 65 bps from 2 year US Treasury to 30 year US Treasury yields. With the current deceleration in the pace of economic growth, we would expect to see the Fed cut rates by the fourth quarter.

Europe

A combination of imbedded structural problems, the effects of Brexit, and trade tariff issues has caused a severe impact on Europe’s economy as growth in the Eurozone continues to slow. As expected, the European Central Bank opened the door to a cut in interest rates over the past week. This represents a sharp reversal to Draghi’s initiative to phase out the “extraordinary policy tools” the ECB had implemented, including the €2.6 trillion bond-buying program, which the ECB had announced last December. Europe is faced with rising populism and protectionism and the inability to enforce fiscal discipline on its members.

The European Union has warned Italy to reduce its spending and comply with the treaty of Maastricht. The rules require all countries in the EU to maintain a budget deficit of less than 2.5% and to maintain total debt of 60% under Eurozone guidelines. Italy has consistently run budget deficits greater than 2.5% and currently has debt-to-GDP of 132%. The new populist-run government has reduced taxes and increased spending in order to stimulate growth. However, the economy is growing at a mere 0.1% this year. No country has ever been fined by the EU for violating its fiscal rules. But, they have been downgraded. We would expect to see a downgrade of Italy’s debt from major rating agencies.

Fixed Income

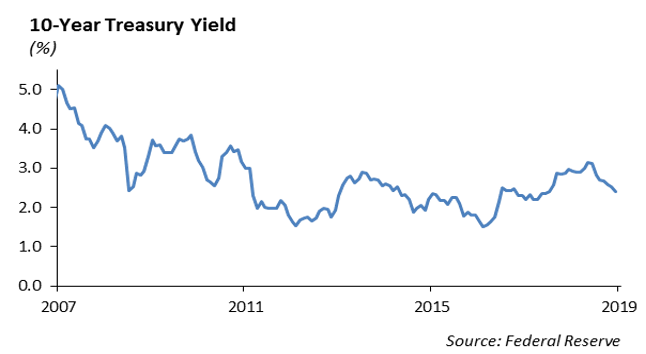

Last week, the fixed income market acted like the bully in the classroom, with its victim being the unsuspecting Fed. Rates from the 1-year to the 10-year dropped significantly, and the forward rate curve is now pricing in a 97% probability that there will be a rate cut this year. The 10-year fell 9bps to end the week at 2.08%, which is its lowest level in almost 2 years. The 30-year actually rose slightly through the week, and the 2-30 year curve steepened to 72bps. Despite pressure from the markets, we believe the Fed will remain data dependent and will not raise rates until the economy clearly signals substantial weakness.

Corporate Credit

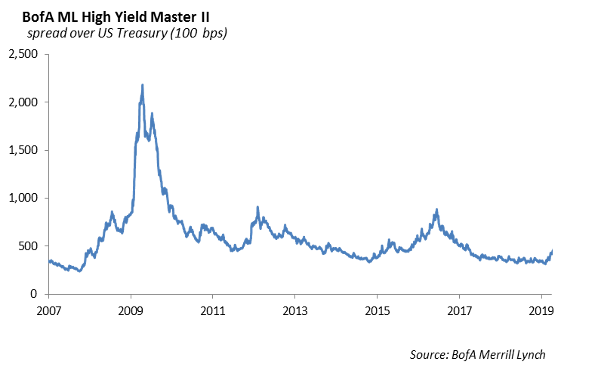

Corporate credit was notably stronger during the week and ended the week 5bps tighter. Investment grade funds had over $1bn of inflows, and the new issuance orderbooks saw an average of 4 times oversubscription. The most notable was senior secured HCA, which tightened 10bps after its launch. Banks and Pharma were the strongest performers during the week, but higher oil prices led to continued spread widening in the oil sector. We continue to favor credit over treasuries and believe an inevitable trade deal will push spreads back to historic tights. Over the past week, we have shortened portfolios across all strategies as rates have fallen over the past two weeks.

Municipal Bonds

The Bloomberg Barclays Muni Index returned 1.38% in May, marking a 4.71% return year to date and underperforming treasuries slightly. Fed Funds data has shown that, over the past year, P&C insurer holdings of municipals has declined by $45bn, and bank holdings has declined by $74bn. As a result of the tax changes in 2018, this unwind has led to an underperformance on the long end of the muni curve, creating a steeper curve relative to treasuries. We believe 10-30 year munis are currently undervalued, and in the face of very low interest rates, we would consider their tax equivalent yields for high income investors.

High Yield

For the first time in five weeks, the high yield credit market saw spread tightening, where we saw spreads lessen by over 20 bps. This spread tightening came from hopes of a Fed rate cut, and the appearance of the Trump administration progress with Mexico on tariffs and immigration. We are now sitting just short of 100 bps tight of year end 2018 levels.

We have continued to see quality outperform in high yield, with BBs outperforming Bs by 50 bps and CCCs a full percent on year to date total return.

New issuance bounced back last week with over $5 billion of new supply hitting the market vs. $1 billion the last week of May. Notable transactions included L Brands, the parent company of Victoria’s Secret, and Bath and Body Works, Sirius XM, and the crossover credit HCA. All these deals priced significantly tighter than initial price talks. While the L Brands new issue struggled at the break, Sirius XM and HCA continued to see considerable yield tightening.

In high yield this week, and as we move into the second half of the year, we’re keeping eye on the energy sector. Energy has performed quite poorly so far this month, with all subsectors lagging the market and oilfield services being one of the only sectors to still see spread widening in June. It is important to note that the price performance in the high yield energy space is highly correlated with crude oil prices, even more so than investment grade credit. At the end of May, we saw crude oil prices drop about 9% between May 29th and the 31st, and high yield energy bond prices followed suit. It appears that the market has a bugaboo on WTI price of $50/barrel, and if prices go below that, we should expect HY energy spreads to gap. Trump’s proposed 5% tariff on Mexico also aided in HY energy volatility with the tariff potentially slashing profit margins on Maya crude in half. News over the weekend and into this morning shows the Mexican tariff is being delayed, and Saudi Arabia and Russia are agreeing in principal to keep the market balanced. We should expect relative strength in HY energy bonds this morning.

Equities

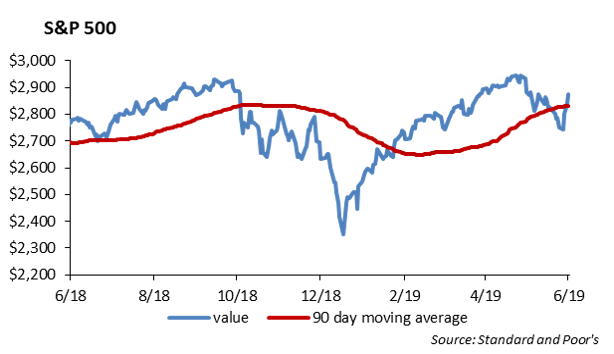

There were three main themes throughout the week, including China, Mexico, and the Fed. The market showed strength with four straight days of gains last week, and the S&P ended up 4.4%, while the DOW gained 4.7%. We are 2.4% off of the all-time high and up 14.6% on the year.

Late on Friday, President Trump dropped his threat of tariffs on Mexico after they reached a deal to slow the flow of migrants. Mexico said it would expand border programs and tariffs of $350 billion were suspended. Futures are showing opening gains of about 0.40% for the S&P and the DOW.

An additional catalyst for last week was Jerome Powell’s comments that the Fed is open to easing monetary policy. On Friday, the market ended up 1%, regardless of the weak jobs report. The U.S. added 75,000 new positions, which was less than half of expected. However, traders saw this as good news, as slowing economic growth leads to a higher probability that the Fed will cut rates.

Info Tech has rallied back and is now up 22.55% YTD, which is the top performing sector. It is worth mentioning that all of the tech giants are under regulatory investigations. There is an anti-trust investigation into Alphabet, and Facebook is the subject of an FTC investigation into whether its practices harm consumers. The chances of breaking up of these companies are obviously extremely low. Government doesn’t partake in the billions in revenues, and the attack on big tech will ultimately just lead to millions collected in fines.

On specific company news, United Technologies has reached a deal with Raytheon to merge, which would give the company a valuation of over $100 Billion, making it the 2nd largest aerospace and defense company. Both stocks were up over 5% in premarket trading. The combined company will be Raytheon Technologies. There doesn’t seem to be a chance of antitrust review based on their current markets. UTC makes engines and parts for commercial planes while Raytheon focuses on missiles and defense systems. About one third of the two companies’ revenues last year came from the Pentagon, and although Pentagon spending has expanded in previous years, it looks to be slowing to low, single-digit increases.

Finally, Salesforce announced this morning that they have agreed to buy Tableau Software in an all-stock transaction valued at $15.7 Billion. The deal is going to add about $400 million in revenue and will close in the third quarter. Tableau’s software is expected to help CRM’s Einstein, its AI platform.

Portfolio Models

Across our models series, we have added to our S&P 500 basis since the beginning of May this year. The S&P gave up nearly 7% of its YTD returns in the face of global headwinds, and as such, we added to our S&P basis 5 times since the beginning of May. The S&P is currently 2% from its all-time high, appreciating from its drop in price. Looking forward, we see further price appreciation through catalysts such as an ease in trade tensions.

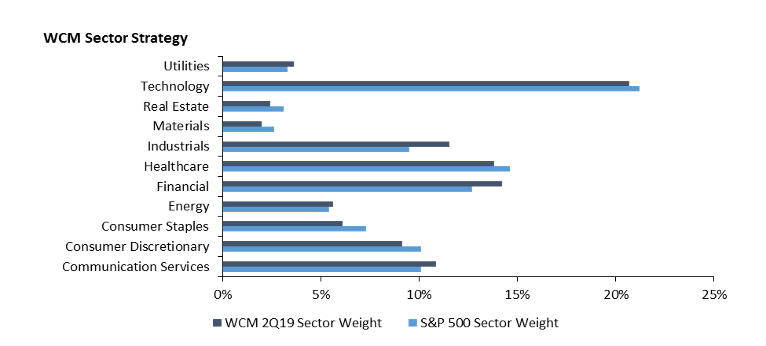

Looking forward to the end of June, the we have already begun discussing revisions to our sector outlooks. The team is currently overweight Communications, Industrials, and Utilities. There are several factors we are taking into consideration for the third quarter of 2019, including trade progressions, Brexit, and rate cuts as opposed to rate hikes. If the Fed does cut rates, we would expect to see a rally in the S&P 500, typically rally led by healthcare and consumer staple sectors, with IT as the laggard. On a valuation basis, we evaluate the sectors’ Price/Earnings and Price/FCF ratio. Financials, Industrials, and Materials look the most attractive compared to their 5 year average metrics.

As we finalize our sector outlooks heading into the third quarter, our Core Sector model allocations will be adjusted. Look for our 3Q 2019 Model Catalog at the beginning of July.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.