Economy – Order in the Chaos

By putting nearly every major trade agreement up for re-negotiation, the Trump Administration has effectively disrupted supply chains for domestic manufacturers. Given the uncertainty to new punitive trade tariffs in goods coming from China, the inability for manufacturers to make long-term capital and business decisions to support production and distribution is weighing on economic growth.

With the current impasse with China negotiations to resolve trade tariffs, the Trump administration has now shifted to resolving the trade agreements with Mexico and Canada this past week. We expect the focus will shift to resolving European trade agreements.

Near term, we do not expect the new China tariffs to be inflationary. However, if allowed to persist, by the second half of 2020, we would expect to see an acceleration in the rate of inflation. However, the market response this past week was reflected in a decline in the yield on the 10 yr U.S. Treasury to 2.36%.

Unsurprisingly, the Labor Party broke off talks last week with the British government over the terms of a Brexit deal. The U.K. Parliament remains in gridlock over terms that would allow for an orderly exit for Great Britain from the European Union. We still believe that if you had had three years to come to an agreement and it didn’t happen, then it has little chance of happening over the next three months. Prepare for a hard Brexit.

Worth the Read

To invest in today’s capital markets, believing that everything is back to normal after the Financial Crisis is a flawed assumption. There are several issues impacting the capital markets, such as the growth of student loan debt, unfunded pension liabilities, and the growth of sovereign debt, all of which are mind-blowing in the pace of growth and sheer size.

In last week’s Thoughts from the Frontline by John Mauldin is an excellent article called “Your Pension May Be Monetized.” Mauldin tends to be more on the doom-and-gloom side of the conversation in the room, which is usually where we are sitting. These are important issues that need to continue to be part of the investment dialogue and strategy. However, it may take many years before they manifest and have an evident impact in the capital markets.

https://www.mauldineconomics.com/frontlinethoughts/your-pension-may-be-monetized

Federal Reserve Remains on the Sidelines

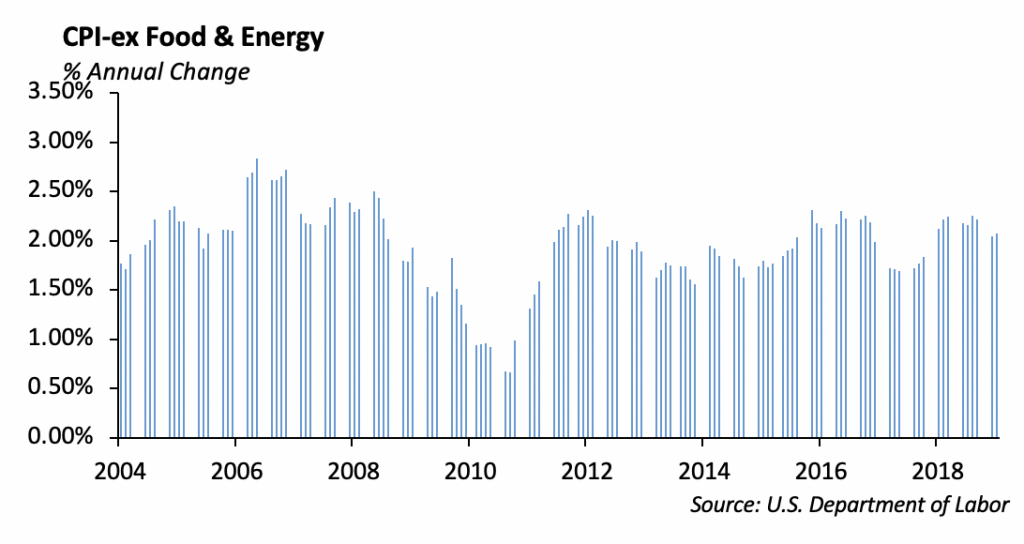

The two mandates of the Federal Reserve are to maintain price stability and full employment. Given the slowdown in economic growth, the Fed signaled an intent to keep short term interest rates at their current level.

The pace of inflation, measured by the Consumer Price Index, has been near the two percent target and within the stated range from the Fed. The argument has been made that, with strong economic growth, the fed could afford to let inflation run hot and not risk the hyperinflation experienced in the 1980’s. However, at this point, we are less concerned about an acceleration in the rate of inflation.

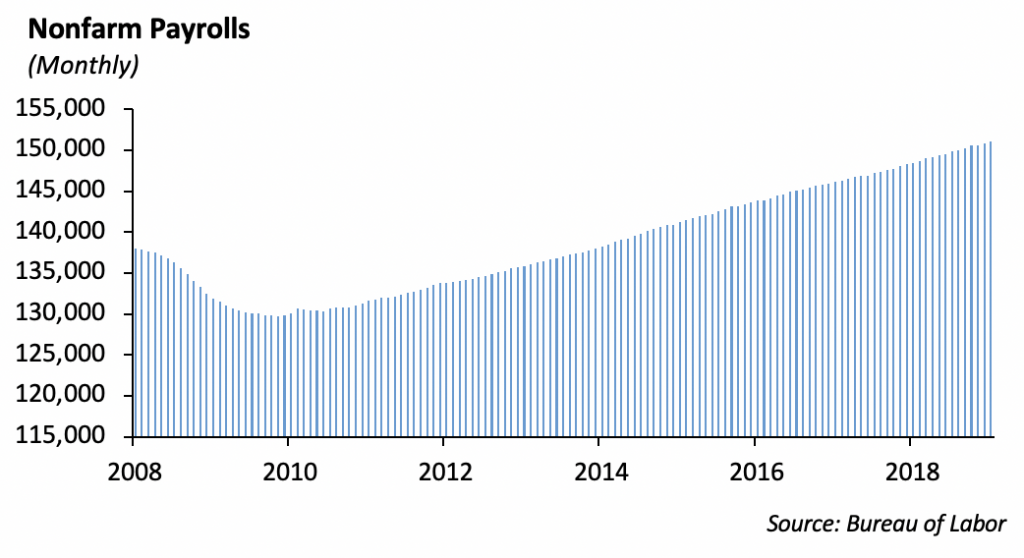

In 1939, the size of the domestic economy was less than $2 trillion and produced, on average, 30,000 jobs per month. Today, the economy is over $19 trillion in size and produces an average of 140,000 jobs per month. The growth in jobs lays the foundation for the consumer sector to spend.

Fixed Income

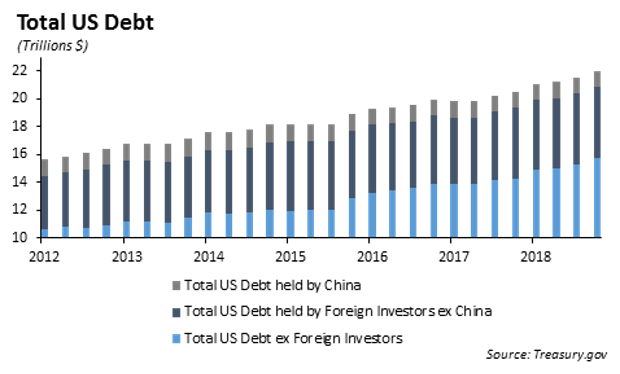

Interest rates continued their decline last week as the focus remained on trade tensions with China. The 10-year treasury declined 5bps to end the week at 2.391%. Last week, there was dialogue in the media surrounding the possibility of China leveraging their holdings of US debt as a way to sway trade negotiations. We believe this approach is unlikely for two reasons. One, while China is the number one foreign holder of US debt at 1.13 trillion, they only own roughly 5% of the $26 trillion US debt outstanding, and markets have shown that they can absorb large quantity selling of this degree. Second, if China were to begin mass selling their US holdings, they would effectively be hurting themselves and the value of their substantial holdings. Given this, we believe it’s unlikely that China will begin dumping their treasury holdings in an effort to hurt US markets.

Investment Grade

Investment grade spreads widened 8bps during the week as the “flight to quality” trade continued to dominate. New issue supply was steady at 30 billion, and books were five times oversubscribed on average. Markel was the best performing issue, tightening 10bps post issuance. We continue to add to our credit position as spreads widen and believe spreads will begin to tighten again as we move to any concessions in the trade talks with China.

Municipal Bonds

Municipals continue to outperform treasuries, despite their historically rich levels. The 10-year muni to treasury ratio declined further to 71%, and the muni curve flattened to its flattest level since 1998. Despite the historically rich levels, we continue to believe munis will outperform two to three times.

- An aging population is driving more retail investors into fixed income securities, particularly municipals.

- The reduction of state and local tax exceptions has driven up the demand for tax exempt income.

- Municipal supply has been lower than expected and currently maturities are outpacing new issuance.

High Yield

US High Yield widened 6 bps last week due to ongoing US-China trade tensions following the 29 bps of widening last week. The index now sits 126 bps tight to YE18 at a level of 407 bps. We had negative performance in the index last week, with a total return of -0.06%. CCCs were the worst performers at -0.27%, then Bs at -0.08%, while BBs were actually positive at 0.02% of total return. For YTD returns the gap in performance between risk tiers is becoming smaller. CCCs still lead at 8.98%, but Bs and BBs are now at 8.22% and 8.08% respectively.

High Yield fund flows were negative for a second consecutive week, with outflows of $2.57 billion, which is large compared to net outflows last week of $212 million. This is the most we have seen in outflows since December.

New issue slowed substantially last week as $3.3 billion of volume was launched compared to prior week of roughly $12 billion. American Airlines issued $750 million of senior notes, and Berry Global issued 1st and 2nd lien secured notes. American Airlines saw healthy oversubscription, while Berry trimmed both of its offerings.

With continued spread widening, we expect to look at Iron Mountain 6% 8/15/2023 and Sabra Health 5.5% 2/1/2021. Iron Mountain is one of the strongest cash flow generators in the high yield space and operates in the high margin industry of document and record storage. Sabra health is a relatively defensive play, carrying ratings of Ba1/BBB-. Both names are within 50 cents of our target purchase price. We are targeting a yield of 5.25% on Iron Mountain and 4.9% on Sabra Health. We already own a 1.5% position of Iron Mountain in our Short Duration High Yield strategy and a 1% position in our Tactical Income strategy. Sabra Health would be a new name to all of our strategies.

Equities

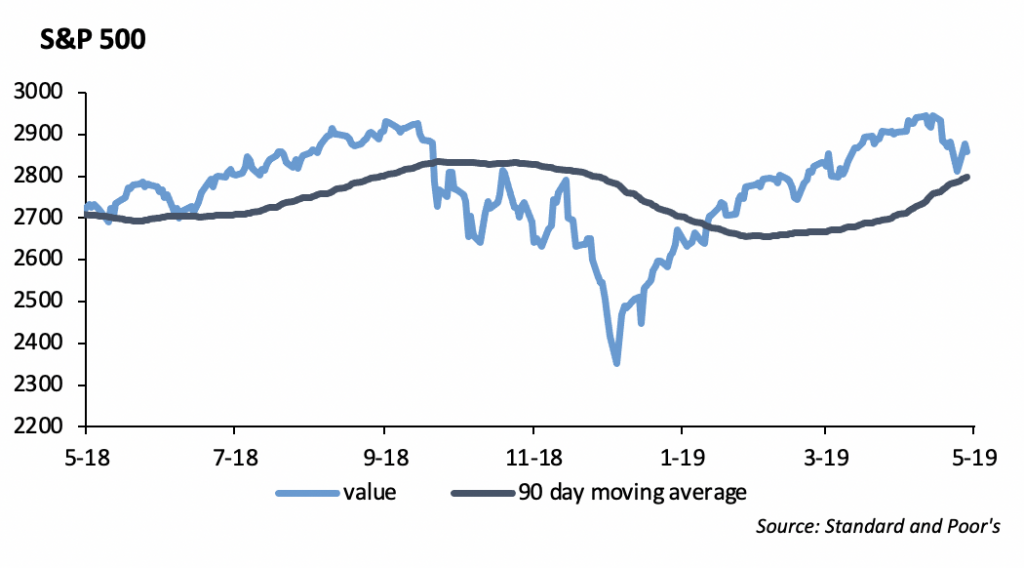

The S&P and DOW fell -0.58% and -0.38%, respectively last week. Stocks started the week negative with more fears on trade negotiations. However, the sell-off ended on Tuesday, and the DOW and S&P made a comeback throughout the week.

92% of companies in the S&P 500 have reported results for the quarter, with 76% reporting a positive EPS surprise, while 59% have reported a positive revenue surprise. The blended earnings decline for the S&P 500 is -0.5%. This would be the lowest year over year decline in earnings since Q2 2016, but it is still well above the -4% decline analysts were initially expecting.

Looking forward to the second quarter, projections show a decline in earnings of -1.9% and revenue growth of 4.2%.

The outperforming sectors YTD are Info Tech at 21.21%, and Communication Services at 18.72%, while the laggard is still Health Care, returning 2.07%. Interestingly enough, the health care sector is reporting the highest YoY earnings growth of all eleven sectors at 9.2%. It is currently trading at an 11% discount to the S&P on a price to earnings basis, while looking at its 5-year average, it trades at a 7% premium.

WMT reported earnings of $1.13, which was an 11 cent beat, but revenue was a slight miss at $123.9 Billion. E-commerce sales grew 37% off of strong growth in grocery and home & fashion categories. Comp sales were up 3.4%, with transactions up 1.1% and average ticket price up 2.3%. The stock was up 2% on the day.

To highlight one of our strategies, our Focused Growth model holds our top growth ideas. Currently, it is up 19.57% YTD, versus the S&P returns of 14.59% YTD. Our current top ideas are Disney, Qualcomm, and MSFT. With our outlook of the 5G buildout, we decided to start a position in Cisco last week. CSCO has a large portfolio of products in hardware and software in the 5G rollout, so it is not just an infrastructure play, but a capture on the ongoing software and services revenue. Cisco’s services revenue rose 3%. Software subscriptions accounted for 65% of Cisco’s total software revenue. All three of Cisco’s segments or core business experienced growth this past quarter, with Infrastructure platforms up 5% YoY, Applications up 9% YoY, and Security up 21% YoY.

On the IPO calendar, Luckin Coffee, the Chinese coffee retailer, came to market. It came in at a $4.2 billion valuation, and after initially popping up 50%, the stock ended its first trading day up 20%. It is the second largest coffee chain in China and plans to pass SBUX by the end of 2019, which would be extraordinary as it has been in operation for less than 2 years.

Portfolio Models

The market outlook has become more benign this year, following a selloff in the last quarter of 2018. Cross asset implied volatility recently dropped to near record low levels. Volatility in the currency markets has been particularly low, dragging down the average level across different markets. However, over the last two weeks market volatility spiked after President Trump initiated tariffs on $200 billion of Chinese goods, which helped push the VIX Index to its highest levels since January.

As we mentioned last week, we like to buy during opportunistic times. Therefore, we added to both the S&P 500 and SPDR S&P China ETF across our Tactical and Core Sector models as volatility spiked and asset prices dropped.

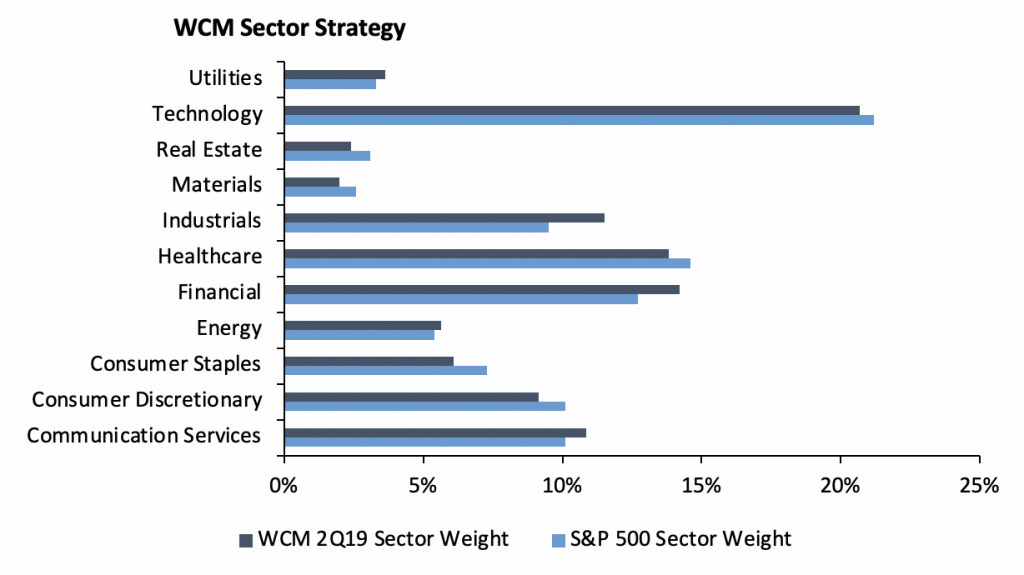

Focusing on our Core Sector Series Models, we have five underlying strategies that vary in allocations to different asset classes, offering investors the ability to choose their risk/return preferences. Our Strategies include: Aggressive Growth, Growth, Growth & Income, Moderate, and Conservative. The Aggressive Growth strategy has the most aggressive allocation to equity with the portfolio being made up of sector sleeves and a small allocation to the S&P 500. On the opposite side of the spectrum, the Core Sector Conservative Strategy has 57% of the portfolio invested in fixed income funds and just over 40% in equity funds. Our underlying weights for sector funds in each strategy are the same. While they differ on the weight basis of the entire strategy, each sector weight stays the same in regards to the sector weights in total. These weights get shifted on at least a quarterly basis as we see new catalysts for individual sectors.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.