The Half-Way Point of the Year

‘Did I miss anything?’ –Daniel Thorson

Emerging from a 75 day silent retreat in early June, Daniel Thorson asked the question through a tweet: “Did I Miss anything?” In early March this year, Thorson had voluntarily cut himself off from society and remained isolated in a remote cabin in northwestern Vermont as part of a Buddhist spiritual retreat. Like Rip Van Winkle, although away for a much shorter period of time, the world had changed.

The first six months of this year has been the most tumultuous period in recent history. The pandemic forced the closing of the global economy, shutting down businesses, travel, and entertainment. Almost everything that our society takes for granted was closed. The result was a massive dislocation in demand and resources. The complexity is compounded by the global connectivity of economies and capital markets.

The Economy

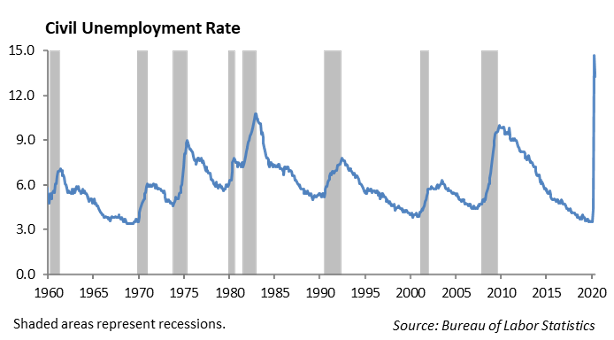

As businesses were forced to shut down to help control the spread of the coronavirus, the impact on the economy has been nothing short of devastating. First, the labor market was crushed as businesses shed unneeded workers. The rate of unemployment spiked from 3.3% in February to 13.3% in May this year. This is the sharpest increase in unemployment since World War II. The number of jobs lost or furloughed in the economy rose to over 20 million.

Then, businesses that couldn’t wait out the storm closed. According to bankruptcy filing statistics reported by the American Bankruptcy Institute, U.S. bankruptcy filings increased in May by over 45% from a year ago. The pandemic has accelerated the closing of business models that no longer are efficient and companies that can’t compete in a world where we need to stay six feet apart to remain safe. Recently, Nieman Marcus, J. Crew, and Hertz have filed for bankruptcy protection as a result of the pandemic.

We estimate that the effort to fight the pandemic cost over $2.0 trillion in Gross Domestic Product. We are still in the early stages of fighting the coronavirus. While an unprecedented amount of government assistance has been implemented, it will not be enough to elevate output to pre-Covid 19 levels. It is important to not confuse an acceleration in growth in GDP with getting back to a level of economic output such that our resources are once again maximized to a level near $20 trillion.

Our base case for the domestic economy in the second half of the year is a slow recovery with persistent high unemployment, continued credit deterioration, and slow rate of new business formation. We expect the government will continue to provide assistance as we head into an election in November. Ultimately, we expect an economic recovery will likely take the better part of two years.

The Financial System

In our analysis of the impact from the pandemic, we separate the financial system from the movements in the economy and capital markets. The financial system provides the grease that lubricates the economic engine. The financial system came into the turmoil this year with a strong capital base and we believe is strong enough to weather the storm.

Last week, the Federal Reserve announced the results of the annual stress test, which was amended to include Covid 19 impact. The Fed acknowledged that the domestic banking system is strong and can weather the shock caused by the pandemic. While most large banks passed, the Federal Reserve took steps this quarter to preserve capital by suspending share repurchases and capping dividend payments. The Fed also is requiring banks to re-evaluate their long-term capital plans.

The result is that Wells Fargo and Capital One will need to re-examine their dividend payment to shareholders over the next several quarters. In addition, regulators announced an additional roll-back of the Volcker Rule which limits how much banks may invest in risky assets. This appears to be an unusual step to take in the middle of a crisis. The loan portfolios of banks, particularly commercial real estate and business loans, will be negatively impacted by the virus in the second half of the year.

Equity

Index Overview

The S&P 500 is down -6.86% year-to-date; the DOW is down -12.34% year-to-date; and the Nasdaq, which is heavily weighted to Technology, is up 8.74% year-to-date. The equity market hasn’t experienced this much dispersion in the broad market indices in over ten years.

Within the S&P, the Technology and Consumer Discretionary sectors have performed well, with Technology up 11% and Consumer Discretionary up 3.4% year-to-date. Consumer Discretionary’s performance can be misleading, however, as Amazon.com (AMZN) makes up over a quarter of that sector and is up 45%. In addition, Home Depot (HD) makes up 12% of the sector and is up 10.36% year-to-date. In reality, over 80% of stocks within the Consumer Discretionary sector are negative for the year. The worst performing sectors so far this year are Energy and Financials, falling -39% and -27%, respectively.

Growth stocks are up 4% year to date, while Value is down -19% year-to-date.

Both small and mid-cap companies are underperforming large caps year-to-date. Midcap stocks are down -17%, and small cap stocks are down -23%.

World Overview

European stocks have fallen -15% year-to-date. Countries like the UK, Spain, Italy, and France have been the largest contributors to the negative performance, all down between -20 to -25% year to date. Emerging markets equitites are actually outperforming Europe, down about -11% year-to-date. In addition, Japan and China have outperformed Europe, down -6% and -2% respectively.

Strategy

We expect volatility in the equity markets to continue over the next couple of months. Until there is a clear catalyst to the markets, we expect it to continue trading within a range. Future catalysts that we are evaluating and preparing for include the second quarter earnings season and the election. Additionally, any progress on a COVID vaccine or announcements regarding localized lockdowns will result in strong swings in either direction.

In the current environment, Technology has become a more defensive play. If we assume that more lockdowns are on the horizon, Technology has the best downside risk case out of every sector. The sectors that have been damaged from the effects of COVID-19 will continue to underperform. Underperforming sectors include Energy, Financials, Industrials, and many Value plays, such as airlines, hotels, cruises.

Model Portfolios

In our Core and Core Sector Series Growth strategies, we continue to build defense in our portfolios. This past week we reduced domestic large cap equity exposure. and reinvested into corporate bonds including VCIT, the Vanguard Intermediate Corporate Fund. This fund has a yield of 3.11% and provides more defense going forward. This is intended to be a tactical move and expect to redeploy the allocation in the second half of the year if the market experiences further dislocation.

Fixed Income

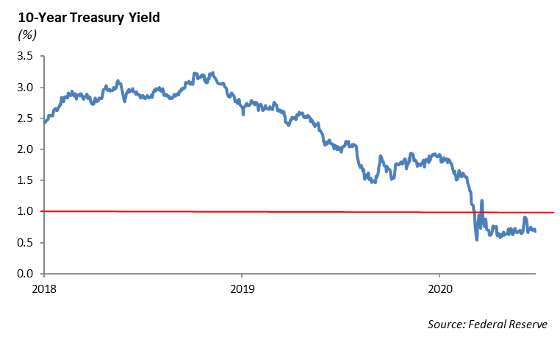

The velocity of change in the markets for the first half of the year makes it easy to lose perspective on how we entered 2020, where markets traveled, and where we are now. At the beginning of the year, the U.S. Treasury curve was inverted at certain maturities, and the 10-year U.S. Treasury rate was 1.88%. Since then multiple Fed rates cuts have driven all treasuries inside 3 years to levels below 20bps and the yield on the 10-year treasury is currently below 70bps. Globally, rates continue to be suppressed as growth and inflation show little sign of accelerating.

There are clear winners and losers in the fixed income markets from the first half of the year. US government bonds have been the leader in 2020. Long-end treasuries are up 22%, short-end treasuries are up 3%, and TIPs are up 6% year-to-date. Treasuries have largely avoided the drawdowns seen in credit and equity markets. Corporate credit was down by over -10% in March, driven by lack of liquidity and a general move away from risk assets. However, credit has recovered and is now outperforming stocks as the iShares Investment Grade Corporate Bond ETF is up 5.9%. The strength in corporate credit has been largely driven by the Fed’s initiative to begin buying corporate bonds. Fundamentally, corporate credit has ticked up over the past year, and so far this year, over $1 trillion in corporate issuance should be a headwind to spread tightening. Municipals have also performed relatively well in 2020. The iShares National Muni Bond ETF is up 2%, driven primarily by the decline in rates this year.

Credit quality has mattered this year. AA corporates have outperformed BBB corporates by 300bps this year. High yield credit has returned -4.5% this year, but more meaningfully, CCC and below bonds have returned -12% so far in 2020. Not surprisingly, levered loans and CLO’s are down between 5-10% through the year as well.

We believe markets will continue to remain volatile through the back half of the year. The focus on higher quality assets will continue, and we have moved up in quality across all fixed income strategies. While income is difficult to place into portfolios, we see lower interest rates in the near term as further potential for spread tightening as long as the Fed continues to purchase corporate bonds. By moving up in quality and building defense into portfolios, we are better positioned to take advantage of market dislocations.

High Yield

Last week, risk assets began to sell off again as investors’ nerves surrounding COVID-19 picked back up, and investors desired to lock in profits for quarter-end. High yield widened about 40 bps, but the index is still tighter by 30 bps for the month of June. “Quality” was the outperformer in high yield last week, as BBs widened less than Bs and CCCs, however the risky tiers have outperformed over month of June.

The primary market is expected to have another quiet week with shortened trading week.

The biggest news of the week was the FDIC’s decision to reduce enforcement on some of clauses in the Volcker Rule. The Volcker Rule was established to regulate banks and keep them from taking huge risks in the market. The decision to relax enforcement would allow banks to avoid the need to set aside cash for derivatives trades between different units of the same firm. It would also allow banks to more easily make investments into venture capital. In this decision, the FDIC is looking to free up more cash for the financial sector to invest in start-ups and small businesses.

The policy decision will have little effect on high yield issuer rated banks, such as CIT Group, but it is much more geared to the big six banks in the U.S., many of which have high yield rated junior subordinated debt.

Energy

Crude oil declined by about -3% last week, making it the second straight week of decline. Demand is still the main driver of energy prices, as fears of another wave of shutdowns lead investors to have a negative sentiment on near term demand. WTI’s price decline aided to the spread widening realized in high yield and culminated in Chesapeake Energy’s decision to file bankruptcy. This bankruptcy is the second major domino to fall in the U.S. oil industry after Whiting Petroleum’s bankruptcy earlier in the year.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.