Economic Outlook

We began the year 2020 with the record economic expansion showing signs of slowing. This economic slowdown was partly through its own inertia and was compounded by a tariff war with China. However, the in 60 days the world changed. By mid-March large segments of the economy were being shut down, students were sent home to finish the semester, sporting events were cancelled, large gatherings were prohibited and restaurants and hotels were shut down. In total, an estimated $2.5 trillion in economic activity, nearly 10% of total economic output, was impacted with efforts to control the spread of the virus.

We are nearing the half way point of one of the most turbulent years for investors in recent history. Without a reliable way to control the spread of the COVID-19 virus, we expect the environment for investors will get more difficult in the second half. Statistically, we expect infections to increase as the economy around the country begins to open up.

Hope is not a strategy. We still do not see a sustainable plan to address ordinary day things like school, college football, concerts, funerals, weddings and worship services. Many major sporting events have begun to take place – without fans present. While safe, this is not economically sustainable. Because we are living through a big experiment, it is important for investors to build a context for our current environment as we consider asset allocation, valuations and risk management. This context might include:

- We are living through two experiments in which there is no playbook. The first is the expansion of monetary policy by the Federal Reserve attempting to soften the impact of a severe slowdown in economic output. The second, is a pandemic that has spread quickly around the globe and is so severe that it can cause death.

- The unemployment rate at 13.3% is the largest in history. We expect it will take over five years for the economy to create the jobs to put people back to work.

- Over two-thirds of corporate issuers have a rating of BBB, a sharp increase from 25 years ago. With ultra-low interest rates and tight credit spreads, corporations have loaded up on debt increasing balance sheet leverage. However, the cost of capital for the company, the yield to investors, is substantially lower than it was 25 years ago.

- The U.S. is in the strongest position to afford to provide stimulus. The foreign countries will likely show slower growth for 2020. Of the top 10 emerging economies, all are in severe recession and many governments are unstable.

The second half of the year will likely show an economy struggling to grow, a banking system under stress of increased non-performing loans. Investors are not adequately compensated for taking risk in most publicly traded markets. Investors should have a plan to protect their wealth if volatility shifts higher, the economy muddles in recession and corporate profits stagnate.

Equity

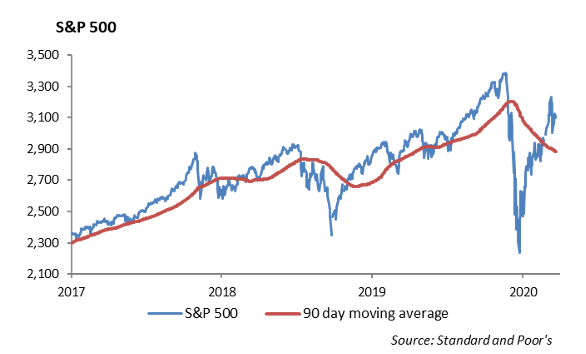

The S&P 500 was up 2% last week, ending at 3100 on Friday; however, the index is down -4% year-to-date. On a 1-month basis, there has been solid performance across every sector with Financials, Real Estate, and Industrials leading the way, up 10% each. These are sectors that were hit hardest in the equity market downturn in March. The Nasdaq Composite finished the week up 3.7%, and it is up 11% year-to-date. The sector rotation has continued and is taking the pressure off large-cap Technology companies to carry the weight of the market rally.

As expected with the re-opening of the economy, coronavirus infections are increasing in some areas; we have seen a rise in Nevada, Florida, and Arizona. However, we believe these increases can be managed through localized lockdowns, and a national lockdown seems unlikely. This time around, hospitals are more prepared, more people are getting tested and statistics are showing the vast majority of cases are asymptomatic. As a result, the equity markets may be better prepared to handle negative news around spikes in coronavirus. At the same time, downside volatility may increase with a bumpy reopening of the economy or the reset to lower company earnings. Additionally, the election is coming up in November and will likely be a source for increased market volatility.

The earnings picture is stabilizing. Downward revisions are dropping, while upward revisions are increasing.

Kroger (KR) reported impressive earnings last week. The company’s EPS of $1.22 beat by 8 cents. Revenue of $41.55 billion beat by $630 million, and is up 12% YoY. Same store sales are up 19%, which easily beat the 13% consensus. This week, we will get a little more insight into consumer behavior as Darden Restaurants (DRI) reports on Thursday and Nike (NKE) reports after the close on Thursday.

Model Portfolios

In our Model Portfolios, we continue to build defense and lower risk. To that end, we are looking to reduce equity in our Growth strategies. Currently, Growth strategies are allocated to about 93% equity. To reduce risk, we are lowering the exposure to both SCHX and SCHG, the large cap domestic growth ETFs. These ETF’s are up 8.5% and has outperformed the S&P by about 12%. We are moving proceeds into fixed income, through the Vanguard Intermediate Corp Bond Index (VCIT). The fund has a yield of 3.09% and an expense ratio of 5 bps.

Finding Income in Equity Investments

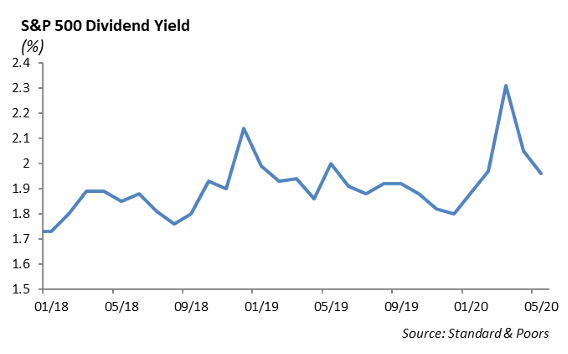

In a world where the 10-year U.S. Treasury is below 1% and the S&P 500 dividend yield is below 2%, investors that rely on investment income will have a difficult time achieving the same results as in prior years. Income can still be found across different asset classes, but it is important for investors to understand the risks and sustainability of income that is imbedded within the investment.

Across equity markets, we continue to favor dividend paying stocks from companies that are able to support their dividend with free cash flow from operations, have a history of growing their dividend, and have a sustainable business model that operates effectively in today’s economy. Here are several examples:

- U.S. Bancorp (USB) is a strong company, and we expect it to have $3.5 billion in 2020 earnings and pay a dividend of $1.68 per share. With the company’s stock currently yielding over 4%, we believe USB is a strong core holding in an income portfolio.

- IBM has struggled to adapt to shifting technology while holding onto its legacy mainframe business which is in serious decline. We believe their acquisition of Red Hat, although expensive, has the potential to lead the firm toward a positive financial change, a return to innovation, and a positive shift in the firm’s culture. IBM currently generates $12.5 billion in free cash flow. Although IBM has not reported revenue growth for 10 years, we believe that trend will trough in 2020 at $75 billion. The company’s current dividend yield is over 5%, and over the past 5 years, the dividend has grown 7%.

- Schwab US Dividend Equity ETF (SCHD) – Across diversified equity ETF’s and mutual fund models, we generally prefer low expense ETF’s. This fund has a low expense ratio of 0.6% and a current dividend yield of nearly 3.5%. We prefer funds that do not excessively overweight REIT’s and Energy in an attempt to boost the yield. Within the fund, energy makes up under 7% and REIT’s are under 3%. While the yield may not be extraordinary, the stability of the income this fund provides is crucial to income investors.

- iShares Preferred and Income Securities ETF (PFF) – This fund’s current dividend yield is over 5%. Because preferred stocks pay a dividend at the discretion of the board of directors, they are not considered pure fixed income securities. However, with a 5-year standard deviation of 10.88 and a 70% correlation to the S&P 500, we view preferred stocks as a portion of the equity allocation.

Income Traps to Avoid

”If something seems too good to be true then it usually is.” When an investor sees proposed or illustrated yields of 10-15%, they should be skeptical of the risks and viability of the income stream. For example, ETRACS 2xLeveraged Long Wells Fargo Business Development Company (BDCL) is an exchange-traded note that boasts a 17% yield. The yield is achieved by levering an already levered asset class in BDC’s. The leverage in the fund leads to heightened volatility and was down over 50% at the lows in March. Dividends for the fund have also been shrinking at a rate of -1.36% over the past 5 years.

In addition, we recommend investors reduce allocation to REIT’s and Energy pipelines near term. While yields are currently elevated, it is primarily due to the negative price performance. With lower expect lease payments due to the decline in economic activity, many REITS are expected to post sharp decline in funds from operations. In addition. With the sharp drop in oil prices this year, many of the pipeline MLP’s are cash flow negative. Therefore, we expect many firms across REIT’s and MLP’s to cut their distributions to shareholders. Overall, we believe the downside risks outweigh the potential for chasing income in these types of funds.

Fixed Income

Interest rates have remained fairly constant over the past few weeks, with little change overall. The 10-year U.S. Treasury ended the week at 0.69%, and global debt was relatively unchanged over the week as well. The Bloomberg Barclays US Aggregate Bond Index, a measure of the broad investment grade bond market, has posted an impressive 6% so far this year. The return has been driven by both lower interest rates and tighter spreads.

The Fed made an historic move last week with its first purchases of corporate bonds onto its balance sheet. The current Fed program includes the purchase of corporate bonds with maturities 5 years and sooner, an investment grade rating as of March 22, 2020, and a limit of 10% of any issue. The initial Fed purchases on Friday appeared small and were spread across a variety of bonds from all industries in an “attempt” to not disrupt the market. In reality, credit markets have run up in anticipation of the Fed’s actual implementation. It seems that the Fed’s announcement did more to prop up credit markets and increase liquidity than will the actual actions of the Fed to buy corporate bonds. Regardless, we have now entered a new regime, and the rules of the game have clearly changed.

High Yield

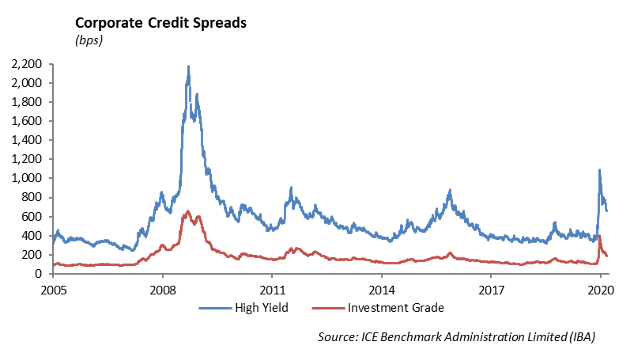

Although the Fed’s corporate bond purchase program is focused on investment grade corporate debt, the Fed’s willingness to act was enough to keep high yield spreads moving tighter. The Bloomberg Barclays High Yield Index tightened 33 basis points last week, with BB rated securities tightening 23 bps, B rated securities tightening 19 bps, and CCCs tightening 78 bps. Securities rated in the BB range are now firmly positive, with year-to-date total return of 1.25%. The lower rated sectors are still negative for the year. The effect on the market from the Federal Reserve and the firming of energy markets were enough to outweigh the increased high yield supply from new issuance. Investors should remain defensive in their high yield allocation. We believe that BB rated high yield bonds are well positioned to survive a second wave of coronavirus, and may benefit from the Fed’s purchasing program, which would help to support any downside price movement.

The high yield primary market picked backed up as almost $20 billion in new volume priced. Year-to-date volume will likely move above $200 billion this week, as new issue volume outpaces 2019 totals by almost 65%. Notable deals include the return of Pacific Gas & Electric, Ford, and Eldorado Resorts. This is the second time Ford has tapped the new issue market since being downgraded to high yield status.

New money continues to pour into high yield funds as $1.2 billion came into high yield ETFs and mutual funds. Funds flowing into high yield is smaller this past week; however, in the aggregate fund purchases have been net positive for roughly the past 15 weeks. Last week, investors poured a net $5 billion into high yield funds.

Energy

Crude oil markets had a strong week, which broadly helped credit spreads. The price of WTI crude oil rose 10% over the week, ending up just under $40 a barrel. OPEC+ has appeared to follow through with their supply cut efforts, and the U.S. inventory build continues to ease. As the rest of the world seems to grasp on economic reopening, all eyes will be on the United States energy industry as its ability to come out of the pandemic is under question.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.