Economic Outlook

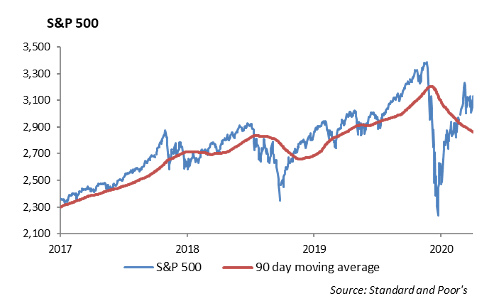

The first half of 2020 was one of the most tumultuous periods in economic history. A global pandemic ripped through the planet, shutting down parts of the economy and causing a swoon in stock prices not seen since the 2008 Financial Crisis. Central banks around the globe stepped in to provide monetary stimulus, which has helped prop up prices of financial assets. In addition, governments have been quick to provide much needed support for businesses and consumers. Amazingly, the total return for the S&P 500 over the first six months of 2020 is -3.08%. In order to better understand the impact of the coronavirus on portfolios of assets, we need to first separate our analysis between its impact on the economy, the financial system and the capital markets. Economic activity and asset prices often move in different directions based on facts and changing expectations.

As a country, the United States is still in the early stages of understanding and solving the problems in the economy caused by the coronavirus. After shutting the economy down for 60 days, states have begun to reopen and return to normal without a way of controlling the spread of the virus. As expected, the number of COVID-19 infections is increasing, which further hinders state and local government’s efforts to reopen.

We estimate the hit to the U.S. economy will be close to $1.4 trillion, or roughly 7 percent of total Gross Domestic Product. Because the U.S. GDP is 70% consumer sector, we expect that the domestic recovery will be slower than other economies. We expect that it will take three years for the United States to recover its $20 trillion in total domestic output, resulting in a strain in employment, and further stress on major parts of the economy, including airlines, hospitality, leisure and real estate. By early next year, we expect to see China take over the top spot as the largest economy in the world.

The Financial System

We believe that a strong financial system will help countries weather economic calamity, and the U.S. financial system came into the pandemic very strong. After the Financial Crisis, banks were forced to increase their capital levels in order to provide better stability. In addition, the Federal Reserve put in place annual stress tests to better help banks understand how their capital and reserves are set up to handle the economic stress on their balance sheet. However, we expect the bank’s loan portfolio will be severely hit as a result of the pandemic. Loan loss reserves were trending lower over the past two years given the rosy economic period, resulting in less cushion for banks to absorb problem loans. Ultimately, domestic banks will weather the storm; however, we expect weaker earnings as banks are forced to shore up loan loss reserves.

The Capital Markets

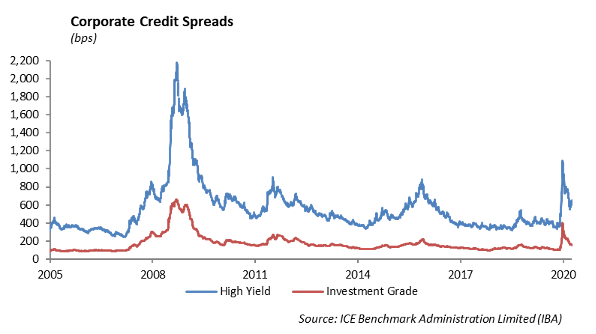

Publicly traded financial assets have experienced high levels of volatility over the past six months. Domestic equities appear overvalued. Credit spreads have tightened but are still wide from a year ago. The fundamentals do not support current valuations in the stock market. However, the Federal Reserve’s monetary stimulus provides a safety net for financial assets. The Fed knows that a sharp drop in stocks will impale consumer confidence, which will compound an economic recovery.

Equity

Earnings are expected at about a -20% decline year over year. Earnings season has just begun for the second quarter, and the first few companies to report have solid earnings.

Micron Technology, Inc. (MU)

Micron exceeded earnings expectations with 82 cents per share and revenue of $5.44 billion, which is up 14% year over year. Estimates were 77 cents per share on revenue of $5.31 billion. There was strong demand from cloud giants, with more investments to support the spike from COVID lockdowns. Guidance for the 4th quarter was strong, with revenue estimates between $5.75 billion and $6.25 billion, which is a growth of 18-28% and well above consensus. Microsoft and Sony have new console launches coming up with the PS5, so this probably plays a role. The stock was up over 5% on the day.

FedEx Corporation (FDX)

Shares of FedEx were up more than 13% on its earnings release. Earnings were $2.53 per share versus $1.52 expected. Revenue was $17.4 billion, which beat estimates by $1 billion. U.S Domestic residential volume was 72% for the fourth quarter. FedEx Ground reported a 20% revenue increase.

Upcoming Earnings

This week will be light with Walgreens reporting on Thursday.

Next week, there are 42 S&P companies reporting, with Financials leading off. Citigroup, JPMorgan, and Wells Fargo report on Tuesday. Goldman Sachs, PNC, and U.S. Bancorp report on Wednesday. Bank of America, BlackRock, Morgan Stanley, Delta, Johnson & Johnson, Microsoft, and Netflix report on Thursday.

Fixed Income

Despite continued strength in risk markets, bond yields have continued to be the stubborn asset, remaining largely unchanged since mid-April. The 10-year U.S. Treasury is currently trading at 0.68%, and the 2-year to 10-year U.S. Treasury curve is at 53bps. With inflation remaining relatively level, real yields based off of Core CPI are negative at -0.57%. Global negative yielding debt continues to grow once again, currently at $13 trillion, as the growth prospects abroad are weakening.

Primary fixed income markets have slowed tremendously relative to the first half of the year. This, along with the initiation of the Fed to buy corporate bonds, has incrementally tightened spreads to 144bps. There was a record level of over $1 trillion in newly issued debt in the first half of the year, and a second wave of COVID-19 begins to shut the economy back down, it is likely that we could see a second wave of corporate issuance as companies attempt to weather the economic storm.

We believe the market volatility is not behind us. Social unrest, a looming election, and continued spread of COVID-19 will be a headwind to asset returns for the second half of the year. As we search for value opportunities across fixed income securities, it is becoming increasingly difficult to source ideas. This is usually the sign of a market topping, so we are continuing to build defense into portfolios to mitigate rising volatility by moving up in quality across all fixed income portfolios.

High Yield

U.S. high yield credit investors took the risk-on approach last week in the shortened trading week, but investors did favor quality in high yield. The Bloomberg Barclays U.S. High Yield Index was tighter by 25 bps for the week starting June 19th. BBs were tighter by 31 bps, Bs tighter by 23 bps, and CCCs were tighter by only 3 bps. We expect high yield issuance to remain slow in the coming weeks as companies enter into earning blackouts and many notable high yield issuers have already coming to market if not once, but twice in this existing environment. High yield new issuance is up 60% year-over-year. Demand for new issuance has not shown any signs of slowing down; however, the past six months begs the question that companies have much more reason, or capacity, to issue out new debt.

Likely the most surprising development last week was fund flows. For the first time in about three months, high yield ETFs and mutual funds had meaningful outflows. Over $5.5 billion worth of U.S. High Yield funds were sold off, likely due in part to financial advisors locking in gains before the half way mark of the year. In addition, reports of an increased spread of coronavirus probably led to some net selling among retail investors.

In review of the first half of the year, high yield has had a difficult time. Among the different ratings, only BBs are positive in total return year-to-date, but at 1.4%, they are still trailing treasuries by almost 9%. Wireless was the winning sector for the first half of the year, as its high yield debt has seen over 5% total return year-to-date, mostly due to the blockbuster T-Mobile/Sprint merger. The Wireless sector is also the tightest sector in high yield with an option-adjusted spread of only 319 bps. Investors could also find a relative safe haven in the high yield Banking and Insurance sectors with total returns over 1% year-to-date. The Utility was also an outperformer with about 1.25% year-to-date total return. In contrast, independent energy or oil field services high yield debt were down -18% and -37% respectively. Some of the names in those sectors have rallied since April, but their losses remain inflated.

Some sectors that may be opportunities for outperformance in the second half of the year include Gaming and Healthcare. Both high yield sectors have seen negative returns year-to-date and have spreads over 550 bps. Build out of online sportsbooks has been streamlined in states like Illinois and should be seen in other states. Healthcare is a diverse sector, but with spreads still wide, one may be able to pick a spot to benefit on combating the current pandemic.

Energy

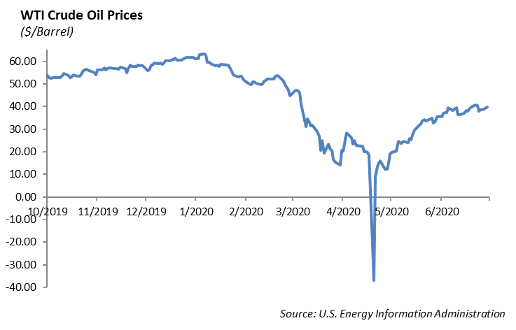

Energy prices hit a milestone last week as WTI crude oil is back above $40 a barrel, a number that many energy companies have advised is workable. The state of energy prices remains perilous, as market increases were due in part to a strong jobs report. However, these new jobs could easily be wiped out in the coming months.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.