The Federal Reserve’s Conundrum – Wash, Rinse, Repeat

The voting members of the Federal Reserve published their rate outlook for the next year. Named the “Dot Plot,” this report is effectively an inside view of how voting members of the Fed think rates will change based on the information they’ve been given. Interestingly, not a single member predicted that rates would be reduced this year. Every member expects the Fed will hold steady or increase rates. Conversely, the market is predicting 100% probability that the Fed will adjust short term interest rates lower in 2019.

Why is there such a large disconnect on the direction of monetary policy?

In the defense of the Federal Reserve, the economy is still fairly healthy and growing at a 1.8% pace. The economy is still producing jobs, wages are increasing, and the labor market appears strong.

However, there is a long list of economic issues that have the potential to negatively impact sustainable growth. With the back drop of slowing global economic growth, the trade war with China is weighing on business investment and corporate earnings. The rate of inflation continues to fall below the Fed’s 2% target.

At the same time, increasing global political tensions between the U.S. and China, Russia, Iran and North Korea would support increased liquidity in the capital markets and easier monetary policy. Not to mention the President is openly badgering the Federal Reserve Chairman Powell to lower rates.

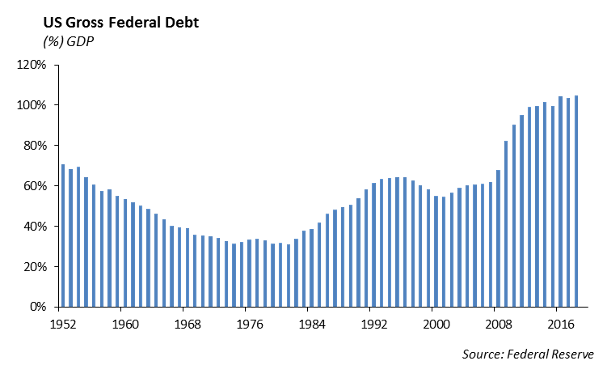

Wash, Rinse, Repeat. Like the directions on a bottle of shampoo, the Fed is stuck in the same monetary conundrum as several other developed countries. Lower rates, buy bonds through quantitative easing, then repeat. This is the new monetary regime, and we are stuck in it. Europe and Japan are also stuck in it. We expect that Europe Central Bank to ramp up its bond buying program next year if the Eurozone economy doesn’t show signs of growth. Ultimately, the growing level of debt becomes a burden as the U.S. approaches 100% debt to GDP. However, when we add back the unfunded pension liabilities, the Social Security funding gap, and the Medicare funding gap, we are closer than we think.

Worth the Read

The June 14 issue of Grant’s Interest Rate Observer has an excellent article titled “All in Favor,” which discusses the current conundrum of the Federal Reserve and its ability to successfully maneuver the economy through a recession. In the article, the author argues that low interest rates help foster increased leverage and speculation, which in turn “require still lower rates to help protect the fragile corporate structures that those very rates made fragile.” Wash, Rinse, Repeat.

Europe

Boris Johnson seems to be the favorite candidate to become the next Prime Minister and lead Great Britain out of the Brexit mess in which they are stuck. He has made no secret of his strong desire to leave the European Union without a deal. If that is the case, we expect the financial markets are in for some volatility later this year when the plan, or lack thereof, becomes evident.

Fixed Income

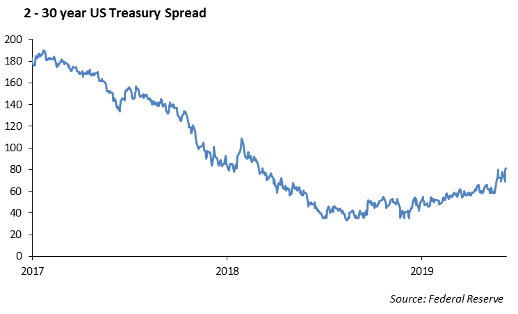

The Fed signaled last week that accommodative monetary policy could be necessary as trade tension extends and causes further global growth slowdowns. This led to a continued decline in interest rates across the globe. The 10-year US treasury dipped below 2% briefly, before ending the week at 2.06%. The 2-year treasury declined 7bps during the week, leading to a steepening of the curve. The 2-year to 30-year curve now stands at 81bps.

US credit was very strong last week, tightening 8bps. Strength was broad across all sectors, and as expected in a risk on market, BBB corporates outperformed A rated corporates. As spreads tightened, we began reducing our credit exposure. We sold Target, Allergan, and Oracle, and we shortened duration in a continued effort to build defense into our portfolio’s.

Municipal Bonds

Tax-exempt municipals outperformed treasuries during the week, and the 30-year Muni/UST ratio declined to 92%. Taxable municipals, on the other hand lagged both corporates and tax-exempts. Supply picked up during the week on the short end. Unlike the steepening of the corporate curve, the muni curve flatten 12bps during the week. We are currently building defense into our muni portfolios by shortening duration through cushioned callables. These bonds offer short call dates and a yield pick up to bullets, and in the event that rates rise dramatically, the yield kicks to a much higher yield to maturity.

High Yield

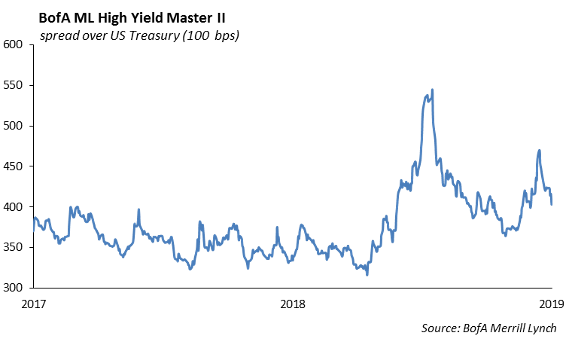

US high yield tightened another 28 basis points last week. Performance was driven mostly by dovish signals from the Fed and higher oil prices. After a 64 basis point tightening in June, high yield now sits almost 140 basis points tight to year end levels. Total return for high yield credit was over a full percent last week, with performance led in BB and B credit. Year to date total return is now over 10 percent in the index, making it the best start since 2009. Quality ties lead the way with BBs over 10.5 percent, Bs over 9.5 percent, and CCCs just short of 9 percent.

High yield funds flows were positive for the second week in a row with $602 million of inflows.

New issuance so far stands modestly above average for the month of June. Refinancing and M&A funding had dominated transaction activity last week. Clean Harbors issued $845 million to address 2021 maturities and Nexstar issued $1.12 billion to partially fund acquisition of Tribune Media.

Last week, we saw WTI prices rise $5.02/barrel, which is roughly 10 percent on the backs of geopolitical concerns between the US and Iran. The drone incident fueled this concern, as well as the attacks on oil tankers in the Persian Gulf.

Equities

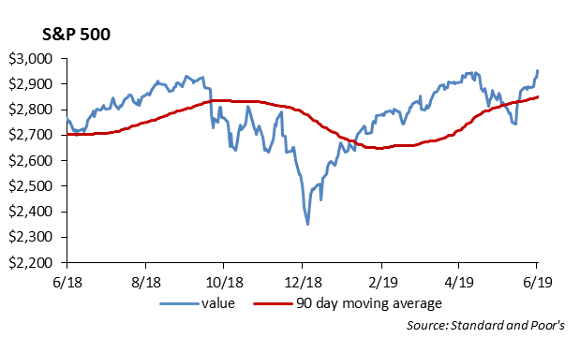

The S&P was up 2.2% this week, rallying to all-time highs. YTD it is now up 17.70%. The DOW was up 2.6%. The two main stories have been the Fed and the upcoming G20 summit in Japan. There have been strong market reactions to tweets from Trump that initially sparked the rally to all-time highs.

For the week, the energy sector had a nice recovery, rising over 5% due to geopolitical tensions pushing WTI up 9% this week. Healthcare and Info Tech were also strong performers, rising 3.1% and 3.3% respectively. The FANNG stocks have had a very nice recovery since the early June lows, with FB, AAPL, AMZN, NFLX, and GOOG all up over 9%.

On earnings news, FedEx and Micron will report after the close on Tuesday, followed by Walgreens, Nike and Constellation Brands on Thursday and Friday.

During the previous week, Adobe and Oracle reported earnings.

- ADBE: EPS of $1.83 beat by 5 cents and revenue of $2.74 Billion. They reported soft guidance, but with revenue growing 25% and earnings growing 10%, the stock was up 5.2% on the day of release.

- ORCL: Beat on top and bottom lines, EPS of $1.16 beat by 9 cents, on revenue of $11.14 billion. They beat estimates in all of their segments, and are aiming for double digit growth in EPS and revenue for 2020. The stock rose over 7% on the day.

In M&A news, Eldorado Resorts agreed to acquire Caesars in a $8.58 billion casino deal. The company will retain the Caesars name, and Eldorado will assume Caesars’ debt of about $8.8 billion. Eldorado will own 51% of the combined company.

To say the IPO market has been doing well would be an understatement. Here are a few of the recent IPOs, with gains above 100% since IPO: Beyond Meat, Zoom, PagerDuty, and Crowdstrike. The Renaissance Capital IPO ETF makes up about 60 recent large IPOs, and is up 34% on the year, about double the S&P.

Portfolio Models

Last week, TrueRock Asset Management released its new model offering, the CIO Equity Series. This series is based on multi-factor strategies that are made up of 40-60 domestic common stock holdings. Factor based investing is a framework that integrates factor-exposure decisions into the portfolio construction process. Factors within TrueRock’s models consist of key metrics that drive risk and return. Some factors used in our investment process include: ROIC, ROE, P/E, Revenue Growth, and even volatility. There are currently five strategies within the multi-factor series, including low volatility, dividend income, growth, quality, and momentum factors. If you have questions, please contact us to learn more about our proprietary security scoring process and how our CIO Equity Models are constructed.

Model Names:

- CIO Low Volatility Equity Model

- CIO Dividend Income Equity Model

- CIO Growth Equity Model

- CIO Quality Factor Equity Model

- CIO Momentum Equity Model.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.