The First Half of 2019

Over the first half of the year, performance of publicly traded securities was impacted by a perceived shift in the Federal Reserve monetary policy, a restructuring in trade tariffs with Europe, Mexico, Canada and China, and a general slowdown in the domestic and global economy.

Sectors posting top performance for the first half of the year included:

- S&P 500 increased by 17.8%

- Russel Mid-Cap increased by 20.2%

- MSCI ACWI increased by 15.7%

The laggards included:

- MSCI EAFE which increased by 13.5%

- MSCI Emerging Markets increased by 10.6%

In the domestic fixed income market,

- Bloomberg Barclays U.S. Aggregate increased a solid 6.06%

- Bloomberg Barclays U.S. Intermediate Aggregate increased by 4.7%

- Bloomberg Barclays U.S. High Yield 1-5 year increased 7.15%

Given the global economic slowdown, an unresolved Brexit, and unresolved China trade issues, we are reluctant to increase international and emerging market exposure. However, we believe the China trade war may result in a shifting of manufacturing and supply chains away from China. Beneficiaries from a shift away from China would be emerging markets, including Vietnam and Malaysia. As a result, we are looking to potentially increase emerging markets exposure in the second half of the year.

Investment Themes – Looking Forward

- We expect domestic economic growth between 1.8% and 2.0% for 2019. Slower economic growth will help keep interest rates low and provide downward pressure on corporate earnings.

- Corporate earnings will remain under pressure as revenue growth slows and profit margins are pressured. Corporate America is largely through the refinancing of debt, which has helped to lower their cost of capital and extend the credit cycle. We expect the next move to support earnings will be labor force reductions similar to Ford and Volkswagen announcements this past quarter. The rosy employment market, which has been the strength in the recovery, will likely deteriorate by the end of the year.

- The trade war with China has contributed to the slowing domestic economic growth rate. We expect that Trump wants a trade deal nailed down with China heading into his re-election campaign. Last weekend, President Trump and Chinese President Xi Jinping agreed to renewed trade talks at the G-20 meeting in Japan. Discussion included a cease-fire on hostile initiatives toward Huawei and a commitment from China to buy large amounts of American agriculture products.

- Boris Johnson is the apparent leader to replace Theresa May. The Brexit process has put a significant weight on both the U.K. and European economies, contributing to a slowdown in growth. We do not expect an acceleration in growth until the lines around Brexit are more clearly marked. We expect a hard Brexit by the fourth quarter.

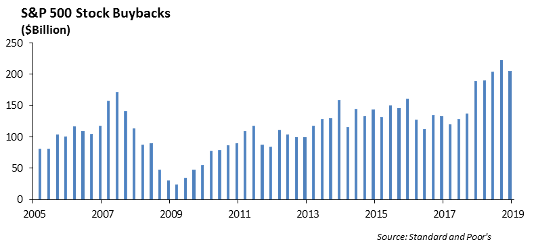

- We expect volatility to remain high this summer unless the China tariff issues are resolved quickly. Stock buybacks will likely be a major theme in the second half of the year as earnings growth slows.

- Liquidity in the credit markets has been difficult at times. New issue volume is down significantly, and Asian buying has declined. While we do not see a significant shift in the credit cycle yet, the seeds are planted for a change. Leveraged loans and commercial real estate are both drawing significant capital, and valuations appear excessive.

Investment Strategy

- We are reducing risk in our portfolios following the sharp rally in domestic stock prices in May. This includes lowering large cap domestic equity. Current valuations do not support slower earnings growth expectations.

- We expect there is a point in which global markets begin to accelerate at a faster pace than domestic economic growth. We are not there yet. As a result, we have not added to international and emerging market exposure. We expect to increase international exposure in the second half of 2019.

- We continue to shorten durations in bond portfolios given the sharp move lower in the ten year U.S. Treasury yield.

- Tighter credit spreads are pushing the “up in quality” trade.

- We are reluctant investors in publicly traded forms of real estate, given the low cap rates and significant amount of money flowing into real estate development. In addition, the quality of underwriting has deteriorated for loans flowing into structured securities. We are extremely cautious on public forms of commercial real estate.

- In general, leverage loans are problematic for us. The amount of “covenant light” loans coming to market is indicative of a peak in the cycle. Credit based mutual funds that use leveraged loans, as well as business development companies should be approached with reluctance given current valuations.

Fixed Income

Treasuries last week rallied ahead of the G-20 meetings as concerns around trade and global growth lead to a stronger belief of a dovish response coming from central banks globally. The 2 year ended at 1.75%, the 10 year at 2.01%, after we saw 10 year rates venture below 2.00% multiple times during the week, and the 30 year ending at 2.53%. We did see a curve flattening during the week with 2s-30s curve losing 4 basis points. Positive news on trade has rates a bit up this morning, with both the 2 year and the 10 year up 2 basis points. Positive news included no new tariffs (for now), Huawei to resume operations in the US where there is no security threat, and China to ramp up its purchasing of US agriculture products.

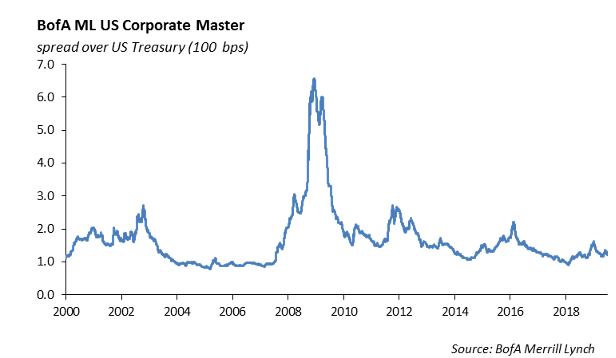

In investment grade credit, spreads slightly tightened last week to a tune of 3 basis points. Option-adjusted spread is in line with where spreads were a year ago, as well as the 5-year average on the index. BBB credit was the outperformer, and we believe investors are still reaching for any yield opportunities. We also saw outperformance in longer dated bonds, cementing the idea that investors are starved for yield.

We believe that the Fed’s dovish tone has had a fairly substantial effect on this month’s spread tightening, but we also see low supply as a leading factor of compressed spreads. Year over year investment grade supply is down 12% this year, and July will likely be quiet as well. Large M&A deals in the near term future are few and far between – the only two being the newly announced AbbVie/Allergan merger and the Department of Justice contingent T-Mobile/Sprint merger. The AbbVie/Allergan deal dominated investment grade credit news with Allergan bonds tightening 20 basis points while AbbVie bonds widened 20 basis points.

High Yield

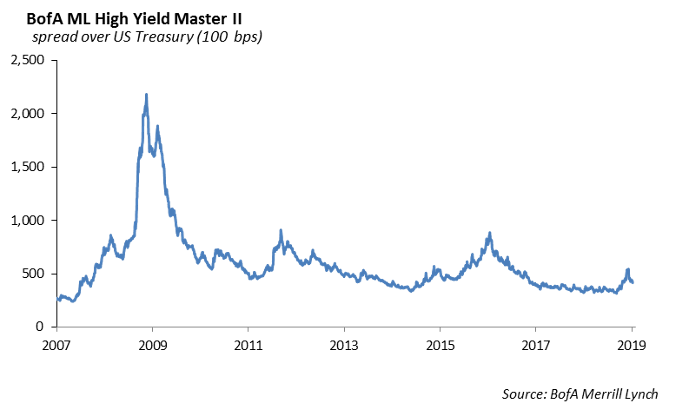

For high yield credit, we saw spreads deviate from their investment grade counterparts, widening 12 basis points. Total return in the index was negative at -0.02% last week with underperformance driven by the lower quality CCCs. Despite the negative return, year to date total return for the high yield index is still continuing its best start since 2009, with over 10% total return.

High yield fund flows were positive for the third consecutive week at over $3 billion, making it the largest inflow in four months.

Another deviation from investment grade credit, we saw the second busiest week of the year in high yield new issuance. Sirius Computer’s $300 million CCC-rated leveraged buyout financing saw significant pushback over covenants and priced at 11% yield to maturity. Allied Universal’s $2.05 billion refinancing was another notable transaction. This week should be light given the Fourth of July holiday.

Crude oil continued to recover last week, rising almost 2% on the week. WTI crude prices now sit at $58.47/barrel, over 9% higher than when the month of June started.

Equities

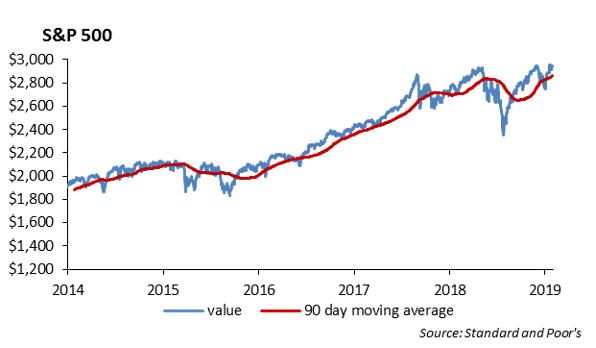

The S&P ended the week down 0.29%, and is now up 17.35% YTD. We are still near all-time highs as last month was the best June for the S&P since 1955.

Financials were the top performing sector this week, rising 1.50%, while Real Estate fell 2.7% and Utilities fell 2.1%.

In earnings news, Micron reported earnings this past week. Micron’s performance is a good indicator of the trade war with China, as they receive over 10% of their revenues from Huawei. EPS came in at $1.05 vs the 79 cents expected and revenues were $4.79 billion. U.S. tariffs had less than a 30 basis point impact on gross margins. Shares were up over 10% on the day and Micron proved they can grow despite all the tariff issues. No earnings are scheduled for this week.

In M&A news, AbbVie announced that they are buying Allergan for $63 Billion, at a premium of around 40%. AbbVie is best known for Humira, the world’s top selling drug at about $20 Billion in revenue per year. They are acquiring the $8 billion Botox franchise. These are two struggling companies whose top drugs are facing declining revenues and increased competition, so this move indicates they are just looking for some type of change and a way to please investors with inflated earnings and revenue numbers. In the end, this merger will likely result in one mega company still searching for answers.

Finally, for your IPO weekly recap, 8 companies raised $2.1 billion this past week, capping off the US IPO market’s largest quarter in 5 years. The online luxury resale company, TheRealReal came to market, and rose 45% on Friday. Adaptive Biotech also had a great day, rising 102% on its first day. As of last week, the Renaissance IPO index is up 35.6% YTD.

Portfolio Models

The Core Sector series integrates a mix of asset allocations based on investors’ risk preferences. Strategies under the model range from an allocation of 100% equity / 0% fixed income (Aggressive Growth) to 40% equity / 60% fixed income (Conservative). Every strategy in this model series holds a sleeve of all 11 sectors. Each sector is weighted in a tactical manner reflecting our beliefs for which sectors will generate Alpha. The sectors are re-evaluated weekly and changed anytime we sees shifts in the forecasted outlook.

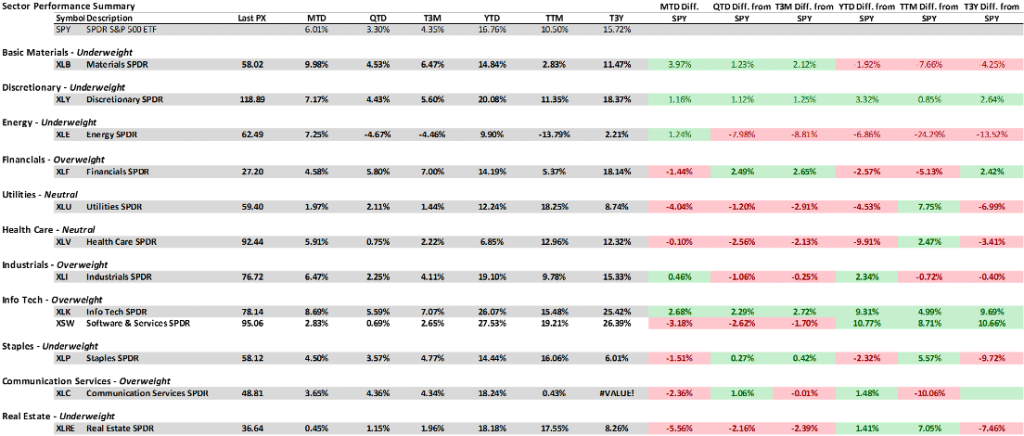

We evaluate overweight/underweight exposures in relation to the S&P 500 weights. We are currently overweight Financials, Industrials, Information Technology, and Communications.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.