Continuing to Navigate the Coronavirus

To better understand the impact of the coronavirus, we separate its impact on the economy, the financial system and the capital markets. We do not expect an immediate rebound in economic activity until COVID-19 testing is easily accessible and there is a reliable way to control the spread of the virus, which could include a vaccine. Here is a summary of where we are this week:

The Growing Problem in Europe

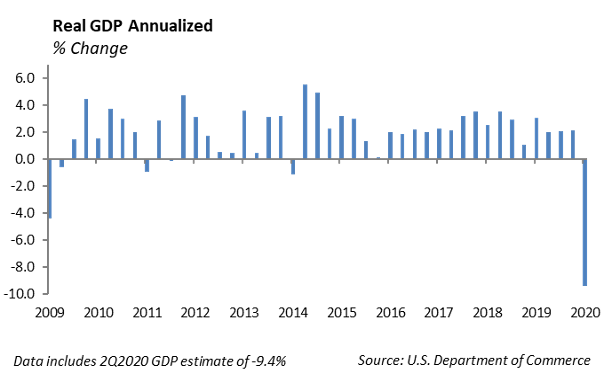

In response to the pandemic, the Federal government and the Federal Reserve moved quickly to put stimulus in place to help cushion the blow to the economy. Still, the U.S. economy has been hit hard as 1Q GDP posted a decline of -4.8%. The second quarter of 2020 is on track to contract further. The cost of the stimulus programs so far is close to $4 trillion, which will push the debt/GDP ratio up to 110% for the United States.

We are now in a place where economies, large and small, are attempting to reopen. While bringing workers back into plants to manufacturer goods is an obvious move forward, reopening the service sector is substantially more difficult given the fear of increasing the spread of COVID-19. Optimism around reopening and experiencing a surge in economic activity is misplaced.

In addition, Europe has major problems that are unfolding currently. Europe has never fully recovered from the last Financial Crisis which impaired their banking system and forced Greece into austerity measures to control its spending. The European Central Bank has been active purchaser of sovereign debt through its bond purchase program, which has helped to push interest rates into negative territory for many of its issuers.

Europe is in dire need of economic support in order to weather the storm caused by the pandemic. However, the European Central Bank and the EU do not have the same tool kit that the Federal Reserve has to provide stimulus to its member countries. While the EU has a common currency, the euro, it does not have common taxing authority and common euro denominated debt issuance. Which brings us to the problem: in an effort to provide much needed stimulus to countries impacted by the coronavirus, the European Commission has proposed issuing euro denominated debt to fund roughly €500 billion of grants to help the economies of member countries hit by the coronavirus.

While the concept of euro denominated debt appears to have the support of France and Germany, a group of four countries including Austria, Denmark, Netherlands and Sweden have preemptively rejected the initiative. This is a critical issue that will ultimately lead to the unwinding of the euro in its current form.

Domestic Equity Valuations

We have three major concerns with respect to the domestic equity markets:

- The stock market, measured by the S&P 500 appears overvalued. We would expect the S&P 500 to trade closer to 16 times earnings. However, with declining earnings and rising stock prices, the P/E ratio is closer to 21 times earnings. Our expectations for company earnings this year have been rattled by the coronavirus.

- The stock market, measured by the S&P 500 is highly concentrated. The Top five stocks, including Microsoft, Apple, Alphabet, Amazon, and Facebook represent nearly 20% of the market value of the S&P 500, and the top 10 largest companies in the index represent over 25% of the market value. This concentration effect potentially causes a more volatile price movement than a more diversified index resulting in higher embedded risk in a portfolio.

- The stock market, measured by the S&P 500 is highly concentrated. The Top five stocks, including Microsoft, Apple, Alphabet, Amazon, and Facebook represent nearly 20% of the market value of the S&P 500, and the top 10 largest companies in the index represent over 25% of the market value. This concentration effect potentially causes a more volatile price movement than a more diversified index resulting in higher embedded risk in a portfolio.

Equity

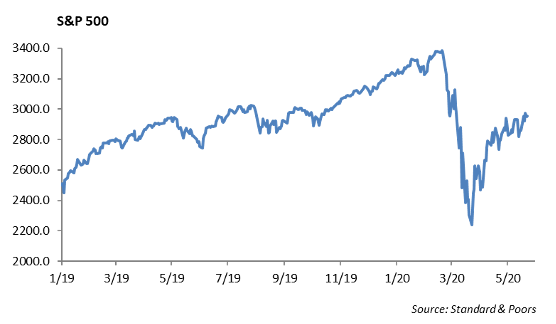

The S&P 500 has been fairly unchanged in May, and the index is down -9% year to date. The NASDAQ is up 4% year to date, and the DOW is down -14% year to date.

Earnings Season Update: 477 of the 505 issues in the S&P have reported earnings (95%). 60% of the companies have beat on sales, and 66% have beat on earnings. Healthcare and Info Tech had the highest percentage of companies that beat earnings with 81% and 77%. Technology is the best performing sector on a year to date basis, up 5%. Healthcare is also outperforming the index, down only -2.5% year to date. Earnings fell about -13% year-over-year which beat expectations, although expectations were fairly low. We expect next quarter’s earnings to reflect even more of the negative impact from the coronavirus. For the quarter, 12 month earnings per share were $139.07. That puts the S&P price to earnings ratio at over 21, which is quite rich compared to prior years.

Earnings wrapped up with the following retailers reporting last week.

- Walmart Inc (WMT) – Walmart reported a great quarter with revenue of $134.62 billion, up 8% year over year. Earnings were $1.18 per share, which beat the expectation of $1.12 per share. Same store sales grew 10% this quarter versus 7.2% expected. E-commerce sales grew by 74%, which was well above the 37% growth last quarter. International sales were up 3.4%, and Sam’s Club was up 9.6%. They withdrew guidance for 2021. Shares were up 4% on earnings release.

- Lowe’s Companies, Inc. (LOW) – Lowe’s reported a beat on earnings and revenue. Same store sales were up 11.2% versus 3.3% expected. Revenue was up 11% to $19.68 billion. Gross margins were up 160 bps to 33.1%, and operating margins were up 210 bps to 10.1%. Lowes.com finally had a good quarter, with sales increasing 80%. The stock was up 7% on its earnings release.

- Target Corporation (TGT) – Target reported mixed results for first quarter earnings. Their digital sales showed very high growth, up 141%. Same store sales were up 11% versus consensus of 7.5%, with total revenues up to $19.62 billion. However, their profit was impacted by higher labor costs and a fall in sales of higher margin items, such as apparel. Food sales were up 20%, but apparel was down 20%. Target’s margins were squeezed. Gross margin contracted -450 bps to 25.1%, and operating margin fell -400 bps to 2.4%. They have extended their $2 an hour temporary pay increase for employees through July 4. The stock rose about 1% on earnings.

Fixed Income

Volatility in fixed income markets was noticeably lower across both rates and spreads last week. The U.S. 10-year Treasury ended the week at 0.66%. Heading into the holiday weekend, new issue markets were much lighter than the past several weeks. With the primary markets subsiding, secondary spreads were finally able to tighten. Investment grade credit spreads tightened 10bps, which was led by A-rated banks that were tighter by over 20bps.

As spreads have continued to tighten, we are reducing credit across the long end in total return portfolios. March was a very difficult month for credit spreads, but the Federal Reserve’s intervention has helped markets recover most of the losses across investment grade strategies. While we believe the Fed’s support will help reduce overall volatility across markets, we still believe the economic recovery will take some time. The fundamental backdrop in credit remains that companies have been levering up while growth is dramatically slowing. This never leads to a good outcome.

Tax-exempt municipals continue to trade at a premium to U.S. Treasuries. As municipals look relatively cheap, we are buyers of essential service municipals and high-grade bonds with state aid or that are insured. We are staying away from university bonds and event/convention centers due to the significant impact that COVID-19 has had on those business models.

High Yield

Last week, the high yield index tightening significantly. Performance was due to strong investor sentiment and reduced new issue supply. High yield tightened 72 bps to an option-adjusted spread of 706 bps – the lowest level since mid-March. However, the index is still sitting about 350 bps wide of year-end 2019. High yield saw almost 2.75% total return that was broadly similar among the different ratings with a slight edge to the lower-rated Bs and CCCs. BBs are only down 3.60% year-to-date. U.S. high yield fund flows continued their streak of meaningful inflows. $1.64 billion flooded into ETFs and mutual funds, marking the eighth consecutive week of net buying.

The primary market remained active, although it was a bit slower due to the holiday weekend and shortened Friday session. High yield priced about $10 billion in volume. Junk credit offerings mainly came from B issuers, including U.S. Steel and Goodyear Tire, both for liquidity support.

Fallen Angels

Fallen angels have been at the fore front of fixed income investment news amidst the coronavirus environment. Fallen angels are corporate credits that were recently downgraded from investment grade to a high yield rating by the majority of recognized credit rating agencies. Fallen angels pose significant risk to the performance of a portfolio, as the move from investment grade to high yield implies a more meaningful default risk and reduced pricing. With the COVID-19 crisis wreaking havoc on macroeconomic demand, there has been an increase in the number of credit downgrades. Recent fallen angels include established names such as Occidental, Macy’s, and Ford. Some estimates show that another $300 to $400 billion of investment grade debt could fall to high yield in the next 2 years.

From a portfolio management stand point, it is important to identify these potential credits early. Generally, spread widening in these names takes place up to 30 days before their impending downgrade. Risk adverse investors should sell out of these credits early. On the other hand, high yield downgrades often brings forced sellers to the market as some investors have mandates to only hold investment grade securities. Forced selling tends to lead to actionable buy levels much lower than market valuation. It is not uncommon to see a bounce back in spread once investment grade credits are downgraded to high yield.

Companies on the fallen angel watch list: Energy Transfer Partners, Conagra Brands, Expedia, and Nordstrom. The first three names have seen good performance recently, while Nordstrom has struggled along with much of the brick and mortar retail industry.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.