Whistling Past the Graveyard

The phrase “Whistling Past the Graveyard” describes the tenuous uncertainty that accompanies ignoring growing negative circumstances which could ultimately culminate in terribly bad outcomes. As we measure the euphoric response from the stock market to monetary stimulus and hope for a vaccine, we contrast the elevated valuations in the stock market against the backdrop of an economic environment still largely shutdown, the carnage of growing problems and the lack of plans to address them.

The first six months of the year was one of the most tumultuous periods in economic history as global economies struggled to combat a growing pandemic forcing business shutdowns in a manner never before experienced. In a period of 60 days, our domestic economy moved from one of the longest periods of economic expansion, to a deep recession with a 14% rate of unemployment and 23 million people out of work.

We are now transitioning to the second phase which involves managing through re-opening the economy without a way to control the spread of the virus or a cohesive plan to address the economic re-opening.

We want to be careful not to confuse monetary stimulus with a recovery. The Federal Reserve has initiated several programs to help provide stimulus and liquidity to the markets. However, in the second phase of dealing with the pandemic, we must now address the growing problems which include:

- The growing problems in the municipal bond market where projects that rely on proceeds from sales taxes from hotels and restaurants to offset the debt are insufficient

- The $4.5 trillion gap in unfunded pension liabilities which will be difficult to narrow due to inadequately low investment assumptions

- A chronically high rate of unemployment as lay-offs and furloughs continue

- The deterioration in the economics of higher education and its impact on state and local economies

- An airline industry that has too many planes and too few people to travel on them

- The growing problem in commercial real estate where declining rent payments will no longer cover the interest expense,

- The uncertainty around the November elections

- Unresolved trade agreements with China and Europe.

Unfortunately, this list is not comprehensive. However, the fundamental premise for investors is that there is no coordinated plan to address how to safely re-open the economy and drive economic growth. While earnings expectations are adjusted lower, we are expecting an increase in volatility and lack of patience for earnings misses.

Equity

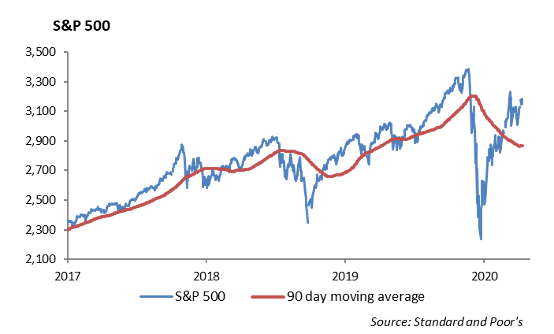

The S&P traded up 1.5% last week to finish at 3185. Year to date, the index is only down 1.42% and 7% off all-time highs. We saw the Nasdaq continue its rally, bringing its month to date gain to 11%. Stocks like Amazon, Apple, Netflix, and Google continue their new highs.

The upcoming week will provide us with significant insight into the actual damage sustained by companies from COVID-19 as 42 companies in the S&P are reporting earnings. This quarter of earnings will show the largest drop since 2008, as estimates range from 20-40% decline in earnings. Sectors such as Energy, Consumer discretionary, and Financials are expected to see well over a 50% drop in profits, while Tech is expected to see closer to a 10% drop in profits.

The calendar for the week ahead is as follows:

Monday: PepsiCo

Tuesday: JPMorgan, Wells Fargo, Citigroup, Delta

Wednesday: Goldman Sachs, United Healthcare, US Bancorp, PNC

Thursday: Bank of America, Morgan Stanley, Netflix, Truist Financial, Johnson & Johnson, Abbott Laboratories, PPG, Domino’s Pizza

Models

We are constantly monitoring our exposure to large cap and large cap growth as it continues to outperform within our Core Series and Tactical Models. We remain cautious on value, as many of these industries continue to be impacted by COVID-19. These industries include airlines, cruise lines, and hotels.

Fixed Income

Interest rates finally broke to the downside during a week, led by a strongly bid 30-year auction and general risk off tone across markets. The 10-year U.S. Treasury tightened by 7bps to end the week at 0.62%. We believe rates are more likely to decline than increase over the near term as continued market volatility and decline in growth have created a ceiling to how high rates can go.

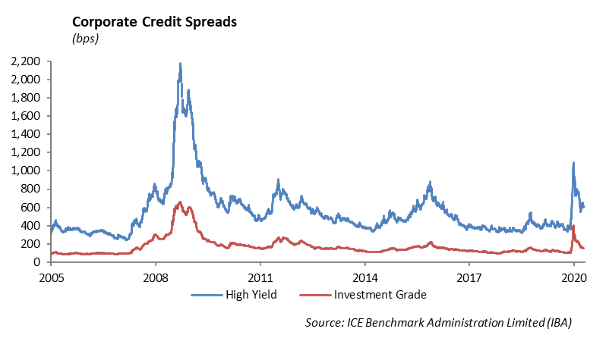

Similar to equity markets, corporate spread tightening stalled over the past couple of weeks. The lack of continued performance is even more striking given the continued purchases of corporate bonds totaling nearly $200 million per day by the Fed. Given the enormous issuance in corporate debt in 2020 that has led to an uptick in leverage from 3.2x to 3.6x, it is clear the Fed backstop has supported a market that fundamentally should be weakening. Increased debt burdens may help some companies limp through this ongoing pandemic, but ultimately high debt loads will suffocate future growth and will stress the system.

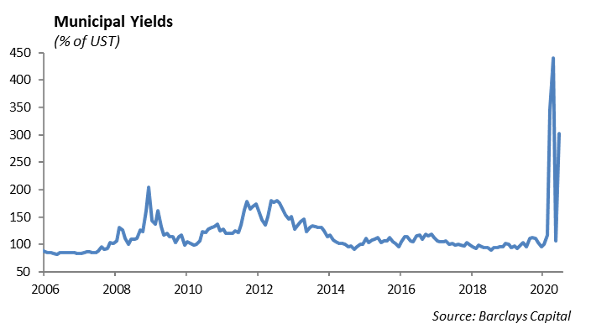

Similar to corporates, municipal bonds have recovered sharply from their March sell off and are positive for the year. This performance comes despite heavy headwinds from a historical decrease in tax-payer income. Much like corporate debt, municipalities have issued a large amount of debt. So far this year, $194 billion has been issued versus $163 billion for the entire 2019 year.

The fact remains that many municipalities are under significant stress and cannot survive without a federal bailout. Transportation revenue bonds such as Metropolitan Transit Authority, and revenue sources such as convention centers and parking garages have experienced obvious declines in revenue. Whether there is a federal bailout of stressed municipalities is questionable. Bailouts have become another pawn piece in the partisan political environment we live in. The Trump administration has already stated that “fiscally irresponsible” democratic regions would not get bailout money.

High Yield

High yield spreads hardly changed over the week as the Friday market rally offset the earlier weakness. The beginning of July has been quietly good for high yield as the total index is up about 1% in price change. This performance is still driven by the higher quality credit. BB’s remain the only rating tier that is positive year-to-date in total return.

The primary market was surprisingly active last week compared to investment grade. $8 billion worth priced last week. The credits were primarily focused in higher-quality and were met with decent amount of demand. Taylor Morrison, Alcoa, and Charter (unsecured) all came to market to further bolster liquidity. We still expect primary issuance to be light this week as much of the market enters their earnings blackout. This should be a slight technical to help support credit spreads.

In keeping with the theme of “Whistling Past the Graveyard,” Winthrop Capital Management remains to be negative on high yield. If second quarter earnings are poor, it will drag on high yield spreads as they are moderately correlated with equities. Default risk is real in high yield, especially in oft maligned industries such as energy and airlines. In strategies that call for high yield, Winthrop Capital Management remains defensive in the BB area where outperformance continues to be in high yield, picking names that we believe to have better credit metrics than some of the low-quality BBB names.

After a brief breather, high yield fund demand picked back up. There were just over $2 billion in inflows into high yield ETFs and mutual funds, offsetting about a third of the outflows two weeks prior.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.