An Update on Earnings Season

The S&P fell -0.28% last week, while the NASDAQ bounced off all-time highs and fell -1.33%. Year-to-date, the NASDAQ is up 15% and the S&P is down less than -1%. Earnings season continues to reveal terrible results due to the impact of the virus, as expectations on S&P 500 earnings indicated a contraction of -44%. With little to no guidance after the first quarter, estimates for company earnings have varied greatly across industries, resulting in over 75% of companies reporting a beat on estimates. The upside surprise indicates that analyst estimates were far too low. On a positive note, companies are beginning to raise guidance for next quarter, providing more clarity and optimism in the near term. Last week, we gained insight into Tech giants Microsoft and IBM, as well as data behind the damage in the airline industry.

TECHNOLOGY SECTOR

Microsoft, Inc (MSFT)

Earnings were $1.46 a share vs. $1.34 expected. Revenue was $38.03 billion vs. $36.50 billion expected. Overall revenue grew 13%. Their cloud segment reported $13.37 billion, up 17% year over year. Within that segment, Azure grew at 47%, which actually slowed from the 59% in the previous quarter. The Productivity segment, which includes Office and LinkedIn, was up 6% to $11.75 billion in revenue. LinkedIn was up about 10%. Personal Computing, which includes Windows, Surface, and Xbox, was up 14% to $12.91 billion. Xbox content was up 65% with record high engagement levels from users. Guidance for next quarter was slightly lower than expected at $35.6 billion. Shares were off by -1% due to the lower guidance and the pullback in Technology for the week.

IBM (IBM)

IBM reported earnings of $2.18 vs $2.07 expected. Revenue was $18.12 billion vs $17.72 billion expected. Year over year, revenue dropped -5%, but with the big beat on expectations, shares rose 6%. The company had slower business from retailers and automakers, causing their Global Tech Services segment to fall -8% year over year to $6.32 billion. IBM’s Cloud segment, which includes Red Hat, was up 3% to $5.75 billion. Red Hat made up $1.09 billion of the total and was up 17%. Red Hat continues to prove the acquisition to be a great decision, with 18% growth in the first quarter and 17% growth in the second quarter.

AIRLINE INDUSTRY EARNINGS

Earnings in the airline industry were consistently negative across the board, which was expected given the performance of this sector year-to-date. Revenue dropped over -80% year-over-year for Southwest, American, United, and Delta. Although demand initially began to pick up in May and June, sales have stalled again with COVID cases spiking in July. In addition, there have been multiple warnings that several thousand employees are at risk to lose their jobs on October 1, when payroll support expires. Airlines are attempting to give employees buyout packages, with some success so far. Both capacity and planned flights are expected to decline going into the third quarter.

United Airlines Holdings Inc (UAL)

Revenue fell to $1.87 billion for the quarter, which is an -87% drop from the $11.4 billion in revenue last year. UAL still beat estimates, but they lost about $1.63 billion during the second quarter. They lost $9.31 per share compared with $9.02 expected. Average daily cash burn was $40 million during the second quarter. Capacity for 3rd quarter is expected to be down -65% year over year. They warned earlier that 36,000 employees are at risk to lose their jobs on October 1 when payroll support expires. They have had 6,000 employees so far accept buyout packages. Payroll costs were down -29% year over year, similar to Delta’s -24% drop. Shares are off 63% year to date.

COMMUNICATIONS SERVICES SECTOR

Snap Inc. (SNAP)

Snapchat fell -8% after reporting their second quarter earnings. Daily active users was 238 million, which was up 4% from last quarter and up 17% year over year. Loss per share was in line with estimates at 9 cents per share and revenue of $454 million beat the $439 million expected. Advertising demand in the third quarter usually includes the back to school season, film releases, and sports leagues. Snapchat did not give any guidance but warned that demand will be affected this coming quarter. This caused the decline in stock value as advertising makes up the majority of Snapchats’ revenues.

Twitter Inc. (TWTR)

Twitter reported revenues of $683 million, which missed revenue expectations by $24 million. However, they beat on active users, with 186 million daily active users vs. 173 million expected, which was up 34% year over year and is the highest total users Twitter has recorded. Advertising revenue slowed to $562 million, and is down -23% year over year. However, demand for advertising is beginning to pick up again. Shares were up 6% on earnings release.

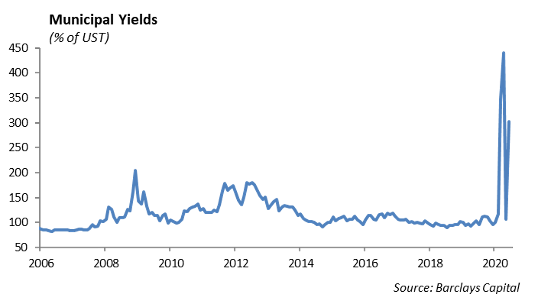

The Municipal Bond Market and COVID-19

U.S. Municipal bonds have benefited from the extreme drop in global interest rates, and despite municipality credit concerns, they are significantly outperforming equity markets. Year-to-date tax-exempt municipals have returned 3.56% and taxable municipals have returned 7.44%. The Bloomberg Barclays Municipal Index now yields 1.27% at a duration of 5 years. The relationship of municipal bonds to U.S. Treasuries has become distorted as the Fed has meaningfully pushed rates lower. We believe there are significant risks in the municipal market as the compensation for risk is low, and the level of uncertainty is at all-time highs.

As the economy shut down in March due to COVID-19, municipal revenue was significantly impacted. The overall revenue shortfall is expected to be over $500 billion over the next 2 years. Extreme unemployment, a sharp decrease in travel and a shut down in large events has led to an unmanageable decline in tax revenue.

In an effort to bridge the gap, municipalities have issued a significant amount of debt as a means of terming out the problem. In the first 6 months of 2020, $194 billion in new debt has already been issued, surpassing last year’s total issuance of $168 billion. Issuance will not be enough to cover the gap. Some areas have already begun increasing taxes, primarily on corporates, excise, and sales taxes. Cost cutting has already begun as well. In April, 1 million state and local public employees lost their job, almost doubling the total 600,000 lost in 2008-2011. Ultimately, these measures intensify the negative effects the virus has had on the economy, and the bottom line is that a federal bailout is going to be needed in order to avoid large scale defaults. Below are some key state initiatives:

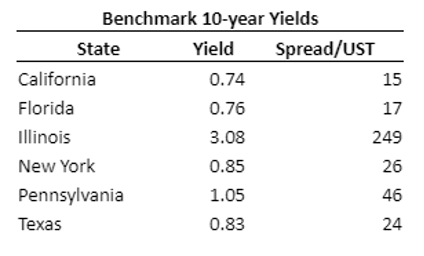

- The 2021 Illinois budget is heavily dependent on federal funds, whether or not MLF ($5 billion) and Phase 4 funds ($7 billion) are approved.

- New Jersey is seeking up to $9 billion in federal funds from both MLF and Phase 4 and negotiating with the legislature on constitutional authority to do so.

- Texas operates a balanced budget, and the legislature is not expected to reconvene until January 2021. Given the initial lower COVID outbreak experience to date and large, diverse economy that is not income tax dependent, the state has not moved on fiscal policy besides the 5% budget cuts and monitoring lower tax revenue. Texas has an $8.5 billion reserve fund that could bridge the budget gap caused by the oil shock in the 2nd quarter.

- New York City, the hardest hit site of the pandemic and the U.S.’s main economic center, has a two-year gap of $9 billion. The city is cutting spending and drawing down reserves at the same time that the state’s multi-year funding lifeline is being cut.

- Philadelphia’s mayor called for property and wage taxes and cost cuts to plug a $650 million deficit; city council is negotiating the budget bill.

While we believe the overall municipal market will find its footing through a combination of measures, we see specific risks in pockets of the muni market. Our primary concerns are toll road, stadiums, convention center, airport, and university revenue bonds. While unemployment will eventually rebound for general obligations, these specific segments are experiencing a secular shift in how individuals live their lives. A general decrease in both business and vacation travel is likely to result in a long-term shift that will significantly decrease the volume for toll roads and airports. While sporting events, concerts and conventions will likely come back, there is no established plan or near-term fix to get these facilities back up and running. Lastly, university revenue is under pressure as students contemplate taking time off of school. There has also been a general push back on the cost of tuition for classes offered virtually. While large universities with endowments will be able to weather the storm, smaller universities could see a significant wave of declining enrolment that will ultimately lead to a lack of solvency.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data