Whistling Past the Graveyard (Part 2)

We are currently living through not one, but two major experiments that have no precedent or road map for success in our lifetime. The first experiment is the global pandemic as we are tasked with protecting ourselves and loved ones from a terrible virus while, at the same time, not impaling business activity and the economy. The second experiment is the central bank’s aggressive use of monetary stimulus. This includes the Federal Reserve using its balance sheet to purchase securities in an effort to maintain liquid and orderly capital markets with low interest rates, ultimately aiming to mute the negative effects of a sharp slowdown in economic activity.

As we assess current valuations of financial assets against the backdrop of these two separate experiments, we feel like we are “whistling past the graveyard” and ignoring the potential downside risks to a longer economic recovery.

It is important to separate the stock value of the domestic economy from the growth rate. The economic output of the United States, measured by gross domestic product, is near $20 trillion. Roughly $1.4 trillion is represented by sports and entertainment such as concerts, football games, and conventions. Nearly 7% of the economic output is currently turned off, and there is not a cohesive plan to get it moving over the next six months.

The United States is the largest, most diversified economy for investors and it has the most sophisticated capital markets in the world. One of the fundamental tenants that allows the machine to operate efficiently is free market capitalism. Capitalism relies on the free flow of credit. Today, our labor market, credit and productivity are sharply constrained, which impacts the level of gross domestic product.

Much of the government support, such as the Mainstreet lending Program, is not desirable for businesses to access. And, the Payroll Protection Program loans that were hugely successful at getting need funds into the hands of small business in March have now been spent. Time has run out for many small businesses and we expect to see a staggering increase in bankruptcies in the third quarter. We still have a staggering 17.8 million people unemployed and an unemployment rate over 11%.

This is going to be a long recovery that will be impeded by social distancing and forced reductions in capacity utilization. Whether it’s a restaurant, a school classroom or a football game, without a way to control the spread of the virus, we do not expect to see a meaningful movement in economic growth.

Portfolio Models

With extended valuations in domestic and international stocks, and a plethora of risks heading into the second half of the year, we are working to build defense into our models.

We expect the back to school shopping season to be muted given that an increased number of students will be studying from home. The labor market appears fragile and we expect that job postings will decline as uncertainty around re-opening the economy dampens job creation. As a result, we are increasing MSCI Low Volatility as part of the Large Cap weight in our Portfolio Models.

Equity

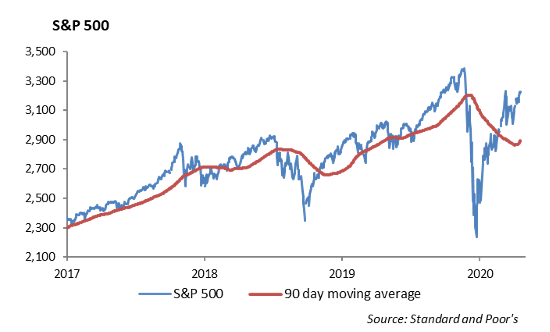

The S&P 500 ended the week up 1.25% and is now breakeven for the year. The index is only -4% off all-time highs. Earnings season began with financials reporting solid results. Trading revenues surged in the banking sector. However, there were large increases to loan loss reserves. If this trend continues throughout the earnings season, the preview so far indicates analyst estimates are too low. Earnings are heavy this week with technology, semiconductor and financial firms reporting.

JPMorgan Chase & Co. (JPM)

Earnings were $1.38/share vs. $1.04 expected. Revenue was $33 billion, which beat by $3 billion. Trading revenue was up 80% to $9.7 billion, with both bond and equity trading exceeding expectations. Bond trading revenue was $7.3 billion, which beat estimates by $1.5 billion and rose 120% year over year. Equities came in at $2.4 billion. The stock was up 4% but had $8.9 billion in expected loan losses.

Citigroup Inc. (C)

Citi reported a huge surge in trading revenue as well. Earnings of 50 cents beat the 28 cents expected. Revenue was $19.77 billion, which beat the $19.12 estimate. Fixed income trading was $5.6 billion, which beat by $750 million. They are maintaining their dividend, close to a 4% yield. The stock was up 2%.

Wells Fargo & Co (WFC)

WFC reported a loss of $0.66, lower than the 20-cent loss expected. Revenue missed at $17.8 billion vs. $18.4 billion estimate. They announced earlier that they would be cutting their dividend; today, they announced the cut to be 10 cents per share. That is down from 51 cents, an 80% cut. The stock was down -4%.

Delta Air Lines, Inc (DAL)

Revenue was down -88% year over year to $1.47 billion. They lost $4.43 vs. the $4.07 expected. They also cut the amount of flights per day planned for August from 1000 down to 500. Current demand is at less than 30% of last year. They cannot lay off any staff until October 1 due to the federal aid they received and have warned all of their employees of impending cuts. The company is trying to get staff to take early retirement packages to reduce payroll. Shares were off by 1%. DAL is down -54% YTD.

Goldman Sachs Group Inc (GS)

GS reported earnings of $6.26 a share, which beat the $3.78 estimate. Revenue beat by $3.5 billion and came in at $13.3 billion. Bond trading revenue was up 150% to $4.24 billion, and equities trading revenue was up 46% to $2.94 billion. Trading in general beat estimates by $2.5 billion. Investment banking revenue was up 36% to $2.66 billion, which beat by $550 million. Wealth management was up 9% to $1.36 billion, mostly due to higher fees. GS was up 6% on the release.

Bank of America Corp (BAC)

BAC reported earnings of 37 cents, which beat the 27-cent estimate. Revenue of $22.5 billion slightly beat the $22 billion estimate. Bond trading revenue was up 50% to $3.2 billion, and equities revenue was up 7% to $1.2 billion. The trading division combined beat expectations by $500 million. Investment banking fees were up 57% to $2.2 billion. The stock was down -3%.

Johnson & Johnson (JNJ)

JNJ earned $1.67 per share beating by 18 cents. Revenue was $18.3 billion, which also beat the $17.6 billion estimate. Revenue was down -10% year over year. Its pharmaceutical business revenues came in at $10.7 billion, up 2.1% year over year. Its medical device unit was the cause of its overall revenue decline, as it fell 34% to $4.2 billion. Hospitals were forced to postpone elective surgeries during the pandemic. They raised full year guidance and its sales forecast for the year to $80-81 billion from $77 billion. Stock was unchanged upon release.

Netflix Inc (NFLX)

Earnings per share of $1.59 missed the $1.81 expected. Revenue slightly beat at $6.15 billion vs. $6.08 billion expected. Global paid net subscriber additions were 10.09 million vs 8.26 million expected. The stock was down on the release with guidance for new subscribers being about half what was expected. They expect 2.5 million net subscriber additions for the 3rd quarter while expectations were 5.27 million. They do not expect any content to be affected by COVID. NFLX initially fell -12% recovered and fell -6%.

Fixed Income

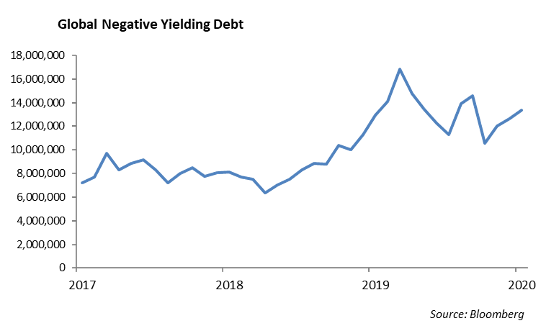

US Treasuries continue to price in an extended period of high volatility and low growth. Flatness of treasuries from 1 to 3 years at 15bps demonstrates the markets expectations that the Fed does not raise rates for at least three years. Global negative yielding debt continues to increase, now above $14 trillion. These factors run in stark contrast to the exponential performance in risk assets such as investment grade credit and equities.

The “tale of two markets” across equities is also true in credit markets. While investment grade credit is now up almost 9% in 2020, other components of the market still show signs of weakness. Down the capital stack, preferred stock spreads have tightened only 25bps since April, while AT1s (CoCo’s) and BB high yield have tightened 150bps and 100bps respectively. While investor are forced to chase yield, there are obvious limitations to how far down in quality they are willing to go. Yields on 10-year BBB corporate are currently at all-time low’s of 2.11%. Municipal bonds are in a similar set, with 10-year municipals at 0.74%. The longer we remain at such low interest rate and tight spreads, the more likely investors are to begin to go down in quality in an attempt to replace income. While levered companies have benefited from refinancing at historically low interest rates, terming out one’s debt has become increasingly costly for companies with a murky future.

As spreads have tightened since the wides in March, we have been incrementally reducing credit across our fixed income strategies. As spread tightening has stalled, we have moved more aggressively up in quality by swapping corporate bonds for treasuries. If volatility across risk markets begins to rise in the back half of the year, we want defense in portfolios. Both high quality and high liquidity are crucial allocations to give portfolio managers the ability to reposition portfolios.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.