The Economy

“Money, it’s a crime share it fairly, but don’t take a slice of my pie” – Pink Floyd

The U.S. Economy contracted at an unprecedented rate last quarter as the coronavirus was bearing down on countries around the globe. The Commerce Department reported last week the U.S. gross domestic product declined -9.5% compared to the prior quarter, the largest single quarter decline since records have been kept over the past 70 years.

The contraction was largely a result of lockdowns imposed by states in March and April in order to control the spread of the virus. In spite of aggressive stimulus from the government to help consumption and small businesses stay afloat, the economy experienced a steep decline in output. The decline in second quarter GDP reflected the hit to consumer and business spending as a result of efforts to control the spread of the virus. Business spending fell -27% annual rate and consumer spending declined -34.6%. Given the recent acceleration in the spread of the virus around parts of the country, we are anticipating the recovery in third quarter GDP to lower than previously expected. Uncertainty around such basic things as kids going back to school, fall sports seasons, eating at a restaurant and business re-openings will continue to weigh on the economy and the labor market.

We expect Congress to pass another round of stimulus to help support the economy. Consumers may benefit from another stimulus check. The airline industry is asking for additional money, and small businesses may get more money from another round of Payroll Protection Program support. Getting money into the hands of consumers is the number one priority to stimulate spending. The problem with that initiative is that many recipients will just stick it in savings.

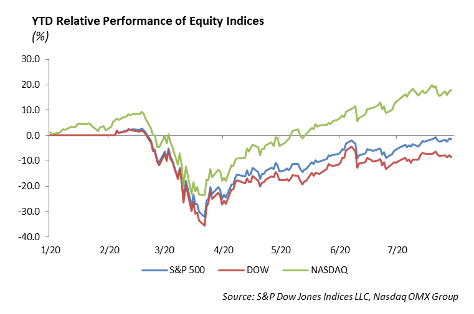

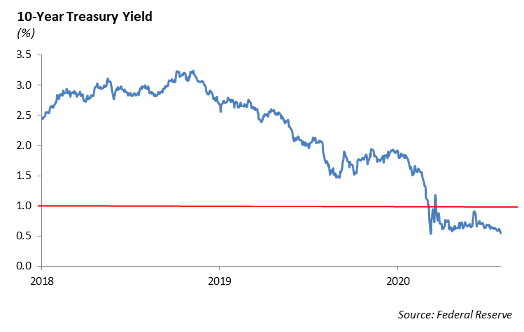

As the economy struggles, the stock market has looked past the downturn, treating it as a temporary blip, and instead has been on a strong rally. Investors are looking past the increase in bankruptcies, the increase in corporate leverage, and the broken business models in many industries. At the same time, interest rates have fallen sharply with the expectation of an economic slowdown.

The question remains, who is right? The stock market with its forward view that the economy will eventually recover, or the bond market with ultra-low interest rates and a view toward a slowing economy.

Equity

The S&P was up 1.73% last week to bring its year to date gains to 1.25%. Huge earnings from the big technology companies pushed the NASDAQ up 3.7% last week and close to new all-time highs. Companies in the S&P 500 continue to beat estimates. Out of 83 companies, 67 have beat their expectations and 30 have raised guidance. 80% of companies have posted stronger than expected earnings. Initially, earnings were expected to fall around -40% this quarter.

Last week, energy companies reported earnings, and they were dismal. Exxon Mobil Corp, the largest domestic oil company, reported a loss of $1.1 billion, its second straight quarterly loss. Chevron Corp reported a loss of $9.3 billion, which included a $5.7 billion write down of $22 billion in its assets. Roughly half of the loss was attributed to its Australian Liquefied Natural Gas business.

Technology earnings are close to flat for the quarter so far, and most companies that are raising guidance are within this sector as well. Last week, Apple, Facebook, and Amazon delivered outstanding results.

Apple, Inc. (AAPL)

Earnings were $2.58 versus $2.04 expected. Revenue of $59.69 billion beat by over $7 billion. iPhone revenue was $26.42 billion versus the $22.37 billion estimate. Revenue was up 11% year over year with every product showing year over year growth and breaking the record for most revenue in the third quarter. Service revenues were up 15%. iPad revenue beat by $2 billion, Mac revenue beat by $1 billion, and other products, such as Air Pods, beat by $500 million and grew 17% year over year. The stock is up 7.3% to $413. Year-to-date, Apple is up 45%.

Facebook, Inc. (FB)

Facebook reported earnings of $1.80 versus $1.39 expected. Revenue was $18.7 billion, beating estimates by $1.3 billion. Daily active users, monthly active users, and average revenue per user each beat estimates as well, despite the protests among large companies. Across all of its apps, the company now has 3.14 billion total users, which is up from 2.99 billion last quarter. For next quarter, they are looking for 10% revenue growth. The stock was up 8% on its big beat.

Amazon.com, Inc. (AMZN)

Amazon reported earnings of $10.30 against the $1.46 expected. Revenue of $88.91 Billion beat estimates by $8 Billion. Amazon expects third quarter revenue between $87-93 Billion, implying 30% growth. AWS reported revenues of $10.81 Billion, which is up 29% year over year. Advertising was up 41% to $4.22 Billion. Subscriptions were up 29% to $6.02 Billion. Double-digit revenue growth was well above expectations and the company rose 4%. Amazon is up over 70% year to date.

Qualcomm, Inc. (QCOM)

Qualcomm reported earnings of $0.86, which beat estimates by 15 cents. Revenue of $4.9 Billion beat by $100 million and was up 0.2% year over year. QCT revenue was up 7%, and QTL revenue was down 19% year over year. Qualcomm reached a settlement agreement with Huawei and signed a long-term patent license agreement. Qualcomm will receive royalties on Huawei sales in the quarter and $1.8 Billion in revenue from past due royalties. Their outlook was strong and that assumes a 15% year over year reduction in handset sales with the delay of the 5G phone from Apple. Shares were 12% on its report.

Fixed Income

The 10-year U.S. Treasury fell to all-time lows during the prior to 0.528%, a clear sign that the bond market believes that the economy will continue to experience turmoil for the foreseeable future. While much of the media points to significant increase in gold prices as a sign of inflation, we would take the other side of that argument. We believe the economy is more likely to move into a deflationary cycle rather than inflationary. The continued decline in interest rates backs up this thesis, and we attribute the increase in gold as being driven by investor looking for a “safe haven” asset to protect against equity volatility. The decline in rates was not isolated to the US, as global negative yielding debt increased significantly from $14 trillion to $16 trillion in just one week.

Unemployment remains above 10%, corporate bankruptcies have increased significantly, and there seems to be no real plan to run a pandemic stricken economy. Yet, credit spreads continue to tighten. Investment grade spreads have now tightened 220bps from their March wide levels, and high yield has tightened 570bps. Combine spread tightening with declining interest rates, and 10-year BBB corporate bonds now yield under 2%. With the Fed’s support of corporate bonds, and investors’ vigorous chase for yield, fixed income market valuations have become extremely stretched. With little upside, we see expected returns investment grade fixed income markets in the low single digits over the near term.

We still believe fixed income is an important component of asset allocations. All risk asset valuation have become stretched recently, and fixed income is still one of the most uncorrelated assets relative to equities and commodities. Across fixed income allocations we have begun to reduce our corporate credit exposure and moved up in quality. We are also diversifying our fixed income allocations by adding high quality agency mortgage backed securities, which are less sensitive to both rising rates and credit shocks. We still believe the path of least resistance for interest rates is down, which ultimately will support returns in fixed income markets despite lower yields.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.