The Economy

It was fifty years ago this past Saturday that the Apollo 11 mission landed on the moon and safely returned, marking a milestone in science and engineering. It was a simpler time – when families had one car, one television with three channels, and TV dinners, eaten off of TV trays, were a special treat. Student loan debt hadn’t been created yet. In July, 1969 there was a total of $36.7 billion in Motor Vehicle Loans Owned and Securitized outstanding. Today there are over $1.16 trillion.

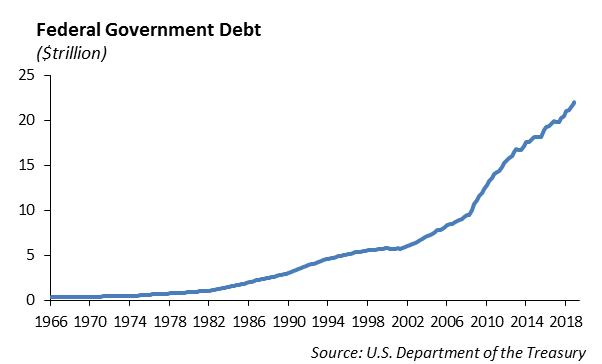

Debt and low interest rates are the fuel for our capital markets and are helping to inflate values for financial assets. In July of 1969, the total public debt outstanding of the United States was $360.7 billion. Today it is over $21.5 trillion and growing at an accelerated pace. Debt helps to fuel the economic machine producing goods, service, and jobs. However, the next economic downturn will hit us hard as lower tax collections, increasing interest expense, and massive spending on social programs put pressure on the U.S. financial condition.

Today, the stock market is still strong with the S&P at 2977, 10 year U.S. Treasury yields are near 2.04%, and credit spreads are tightening. The Fed is expected to begin lowering short term interest rates by 25 bps this week, which has helped to fuel stock prices. We expect corporate earnings to trend lower, based on fundamentals, and continue to slow for the remainder of the year. As a result, we believe there are more catalysts for lower valuations once the decline in short-term interest rates is discounted into the market. We continue to reduce risk in our portfolios and models for the second half of the year.

The Fed

If you watch Stranger Things on Netflix, you know there is a place called the “Upside Down,” which is a mirror image of the real world, but it is a dark and bad place. The show takes place in 1983 in a make believe town in Indiana, called Hawkins. There is an awesome Ford Pinto and a yellow phone with a cord attached to the wall. All the phone calls are listened to by people from Hawkins Lab. For some reason, every time they look for the entrance of the Upside Down, it’s at night. Scary stuff.

After eight years of watching the economy start to function following the shock of the Financial Crisis, the Fed began to slowly move interest rates higher in an effort to normalize monetary policy. However, in an abrupt about face, the Fed has now signaled that short term interest rates will be lowered this week by 25 bps. We aren’t sure whether it’s pressure from the White House, the media, or if the Fed actually sees an economic slowdown heading our way, but the shift in monetary policy raises concerns.

The equity market loved it. The bond market loved it, too. But, something doesn’t feel right – it feels like Stranger Things, and we are shifting into the Upside Down.

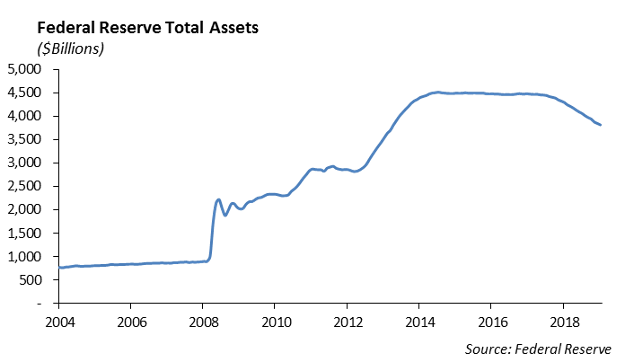

Does a 25 bps shift in interest rates really matter? With the Federal Reserve sitting on $3.5 trillion in bonds that it purchased as part of its quantitative easing program, we can’t ignore the power of the central bank to shift rates across the yield curve through open market purchases. The assumption that a shift in short term rates will have a meaningful impact on economic activity gives us pause. We are moving to reduce risk in our portfolios.

Worth the Read

It has been said that the technology that launched the Saturn V rocket and took the Apollo 11 crew to the moon and back was less sophisticated than our smart phones. The July 20, 2019 edition of the New York Times celebrates Neil Armstrong’s walk on the moon 50 years ago with several articles including a reprint of the original article published on Monday July 21, 1969. The headline “MEN WALK ON MOON” was the largest font that the New York Times had used up to that point.

Fixed Income

Interest rates continued to show volatility last week, especially after New York Fed President, John Williams, expressed his opinion that monetary policy needs to be adjusted quickly to protect against low inflation. After these comments, the implied probability of a 50bps cut in July jumped from 10% to 63%. Rates abroad still remain in negative territory, with the German and Japanese 10-years at -32bps and -14bps, respectively. We continue to believe that the Fed will not cut rates by 50bps unless there is significant economic data to back such an aggressive move.

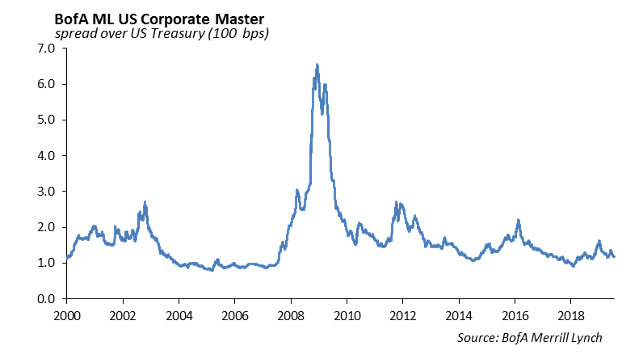

Investment grade spreads continue to remain stuck as investors await the July 30th Fed meeting. While spreads are not at their tightest, they have been significantly tighter over the past year, and the Bloomberg Barclays Corporate Bond index has had a 9.88% total return this year. We continue to reduce spread duration by selling longer duration credit, however we continue to like crossover and high yield credit three years, where we can pick up additional income to offset our higher quality barbell on the long end.

Municipal Bonds

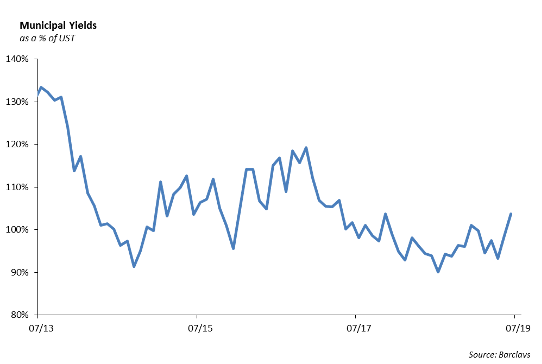

Muni fund flows continue to be strong, after $1.7 billion flowed into funds marking the 28th straight week on positive flows. Retail demand continues to drive down the short end of the muni curve, which has tightened 80bps over the past 6-months. The muni 2-10 year curve now stands at 124bps, which is almost twice the steepness of the treasury curve. We think this steepness provides an opportunity for muni investors to begin extending their portfolio in the face of lower global yields going forward.

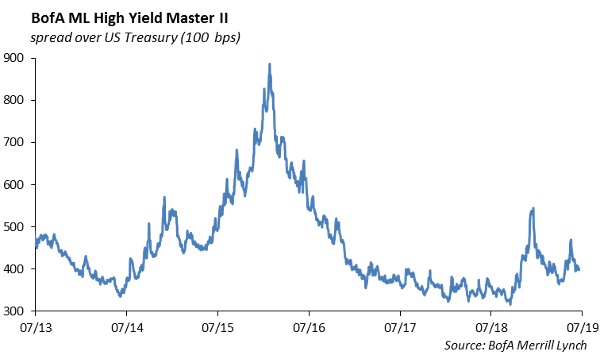

High Yield

The U.S. High Yield Credit Index again saw modest spread widening last week. The index finished 5 basis points wider last week, after widening 4 basis points the week prior. We still sit significantly tighter than year-end levels at 126 basis points tight to December 31st. The index as a whole returned -0.17% last week, with risk tiers leading the underperformance. The difference in return among these risk tiers was a bit more pronounced this week, as both CCCs and Bs returned quite in the red at -0.37% and -0.30%, respectively, while BBs had flat total returns. We still favor BBs over lower quality credit, as we see no catalyst for BB outperformance to stop. BBs are now the only risk tier with over 10% total return year-to-date, as Bs fell below that threshold this week.

Despite high yield’s negative performance, fund flows remained positive for the sixth consecutive week with inflows of $573 million.

New issue volume remains high in July. $7.6 billion priced last week on seven deals, putting this July on pace to be the busiest month in five years. We see this as the biggest reason for high yield spread widening, as investors can get more yield with relatively better quality than they would be able to do in the secondary market. Notable new issues last week were Sinclair’s $4.9 billion secured and unsecured deal to fund their new subsidiary’s, Diamond Sports, acquisition of several local sport stations from Disney, and Hertz $500 million senior unsecured paper to repay 2020 and 2021 maturities. Interestingly enough, part of Sinclair’s contribution is equity stake in their new station Marquee, a regional sports network created in tandem with the Chicago Cubs. Both these deals saw good levels of demand, with Sinclair 4 times oversubscribed and Hertz pricing 12.5 basis points tighter than initial price talk.

Equities

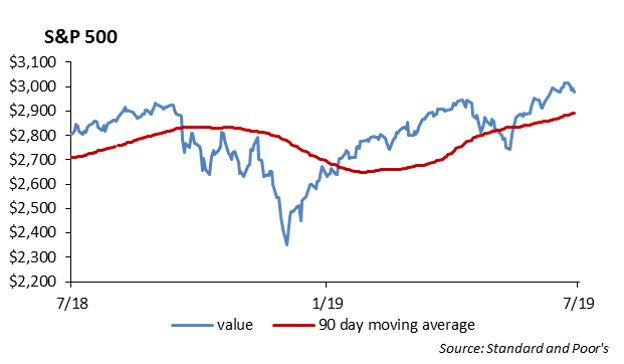

The S&P was down 1.23% this past week, ending at 2976, although still returning 19% YTD. Large cap indices are all up about 2% this month, while small cap still lags in July, as the Russell 2000 is negative for this month. Small Cap outperformed early on this year, but haven’t kept up since then, as they are underperforming the large cap index by 4%.

The focus for the next few weeks will continue to be earnings. Expectations are set fairly low for this earnings season, with consensus forecasts currently reflecting a decline of 1.4% on a YoY basis. With lowered earnings forecasts, expect a lot of beats, which stocks have done of 5 consecutive quarters by about 3-5%. Info Tech will again be the sector to watch, as it is the most impacted as a result of trade, given its exposure to China. It’s also the top performer by a wide margin, returning 31% YTD.

- NFLX– Netflix reported the first drop in U.S. users since 2011. It had 130k fewer subs at the end of the quarter compared with the first quarter, and the stock fell 11% on the news. It added 2.7million subs in the quarter, which missed the 5mil forecast and the 5.5mil from last year. It lost The Office and Friends, their top 2 shows, and their stance is that they will have more to spend on originals. It still has 60mil subs in the U.S. and 91.5mil internationally for a total of 151.6mil, which was short of the 156.5 expected. Revenue rose 26% to 4.92 Billion, which slightly missed.

- MSFT– EPS of $1.37 vs $1.21, Revenue of $33.72 Billion vs $32.77 Billion. Revenue grew 12%. Microsoft’s Cloud segment which includes Azure, had $11.39 Billion in revenue, revenue from Azure was up 64% year over year. The Personal Computing segment, which is Windows, Surface, and Xbox, ended with $11.28 Billion in revenue, which beat the consensus of 10.99 Billion. The stock rose 2% on earnings release.

Disney’s “The Lion King” had a huge weekend – way above expectations. It made $531 million worldwide in 10 days, and $185 million this weekend in North America, making it the biggest opening for July and the biggest opening for a PG-rated film. It was also the second highest opening of the year, behind the Avengers, which became the biggest box office blockbuster of all time this past week, surpassing Avatar. Disney now owns 5 of the top ten highest grossing films of the year.

We have a busy schedule of earnings this week. Just to name a few: Lockheed will report tomorrow; Boeing, FB, and PYPL on Wednesday; and Google, Amazon, and Starbucks on Thursday.

Portfolio Models

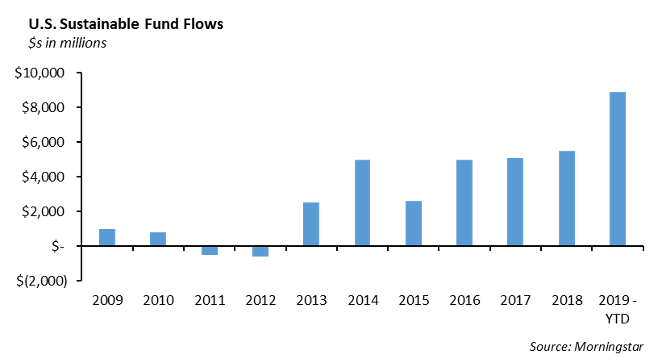

Investing in ESG (Environmental, Social, and Governance) companies has become a prominent topic among many investors. In today’s day and age, companies have been scrutinized for excess carbon emissions, burning fossil fuels, and lacking social sensibility. ESG investing focuses on supporting companies that go above and beyond on such criteria.

We introduced our CIO Equity model series at the end of 2Q19, with five primary factor Strategies. In addition, we are building a sixth, ESG-focused strategy. This new Strategy will be composed of primarily common stock holdings and allocated across companies based on an aggregated Environmental, Social, and Governance score. There are several underlying factors that go into a companies’ score, such as: Carbon Reserves, Green House Gas/Revenue, Employee Turnover, and even the amount of independent board members. Stay tuned to find out more about our new CIO Strategy as it is released in early August.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.