The Economy

The power of social media allows communication to travel around the globe instantly. In 1517, Martin Luther, with the benefit of the recently invented Gutenberg press, nailed his 95 theses to the doors of the Wittenberg Castle church effectively launching what was the spark for the Protestant Reformation. Imagine if social media had been around and Martin Luther could have tweeted directly at Pope Leo X.

With a simple tweet last Thursday, President Trump told China that he would impose 10% tariffs on $300 billion of Chinese goods starting in September. Stock prices fell sharply, oil was down 7% and bond yields tumbled. Up to this point, the market had navigated the expected 25 basis point drop in short term interest rates by the Fed. This move was telegraphed more than one of quarterback Norm Snead’s passes.

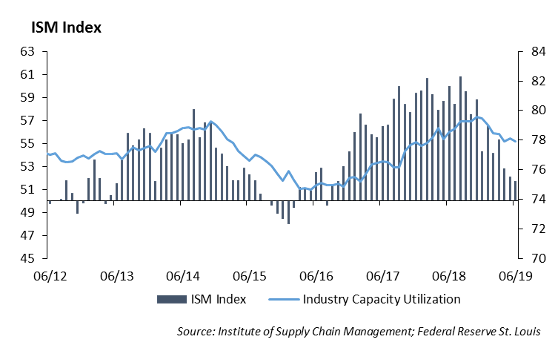

The economy, while still growing, is showing signs of slower growth. The ISM manufacturer’s survey for July came in at 51.2%, a decrease of .5% from the prior month. A number over 50 shows that the economy is still growing. A Department of Commerce report also showed that construction spending fell sharply and unexpectedly in June.

The Fed

Last week, the Fed lowered short term interest rates 25 bps. A recent article suggests that the European Central Bank (ECB) forced the hand of the Fed by lowering rates the prior week. The answer is – absolutely yes. There is now over an estimated $15 trillion in bonds that trade at negative yields. The German bund trades at -0.4%. The ECB needed to lower rates as part of its stimulus initiative. With the yield on the 10 year U.S. Treasury sticking out at 2.08% two weeks ago, the Fed needed to lower rates and provide protection for the dollar.

So, we come back to the question: does a 25 bps shift in interest rates really matter? We believe the answer is still no. The move was symbolic, and to us, it appears the Fed is trying to placate its critics. While the economy is slowing, a 25 bps move does not provide much of a gap to allow for refinancing or stimulate borrowing, particularly in the housing sector.

Europe

The Bank of England (BOE) trimmed its economic growth forecast for the remainder of 2019 and 2020 and indicated that British economic data had become “volatile” as the deadline for leaving the European Union fast approached. At the same time the BOE kept its benchmark interest rate at 0.75%, even as it acknowledged the “intensifying Brexit-related uncertainties on business investment and weaker global growth” were hurting the British economy.

At the same time, France reported a decline in economic activity as GDP slowed to 0.2% in the second quarter. This exceeds both Germany and Italy’s economic growth. The French government has tried to fuel household purchases through tax cuts and benefits, but has gotten little traction as household consumption was anemic in the quarter. The consumer sector remains fearful of joblessness even as the unemployment rate has declined to a 10 year low. In an interesting twist, France’s fiscal spending initiatives, which were designed to spur growth, have put the budget deficit above the 3% ceiling instituted by the European Union. It would be difficult to hold Italy accountable when the other leaders of the EU are out of the required budget deficit ceiling limits as well.

Fixed Income

There was little drama from the Fed last week. Jerome Powell gave the market exactly what was expected, a 25bps rate cut without much insight into where they will move in the future. This doesn’t mean that markets were without drama through the week. After Donald Trump announced increased tariffs on China, there was a broad flight to quality and rates decreased dramatically. The 10-year US Treasury fell 22bps and ended the week at 1.86%. Global rates continued to fall, and the entire German curve moved into negative territory. The 30-year Bund rate is currently 0.00%.

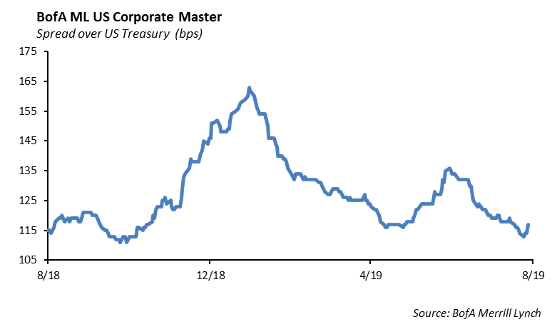

Investment grade bonds were not immune from the risk off trade, as spreads generally widened 6bps. Despite this recent sell off, bonds have had a fantastic run this year. As of the end of August, investment grade bonds have returned over 10%. We believe the second half of the year will be much more challenging, and investors should expect much lower returns going forward. We continue to decrease risk in our portfolios and are shortening duration to build defense as valuations are becoming stretched.

Municipal Bonds

Declining yields has given muni investors a reason to pause. Muni yields declined roughly 10bps over the past week and a 5-year AAA muni now only yields 1.10%. While the yield of munis relative to US Treasuries generally improved last week, outright yields cause a dramatic slowdown in flows into muni funds. Flows came in at only $400mm versus the 2019 average of $1.2bn. While the muni curve remains steeper than the treasury curve, we would caution investors from extending duration in a period where the risk to rates is asymmetrical to the upside.

High Yield

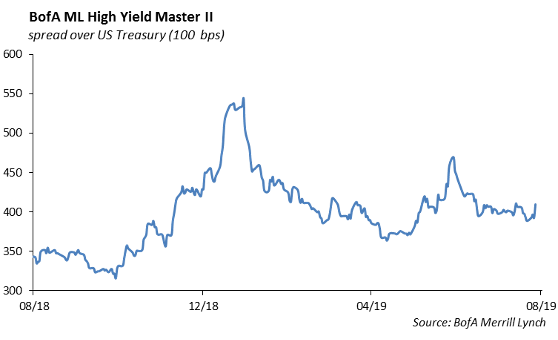

U.S. high yield credit also widened last week, giving back 30 basis points of spread to finish at an option-adjusted spread of 419 basis points. This widening was similar to investment grade credit, being due to increased China tensions and uncertainty surrounding future Fed rate cuts, but also was negatively affected by stock market volatility. High yield as a whole lost 36 basis points of total return. Underperformance came from the riskier tiers with CCCs returning -78 basis points, Bs returning -53 basis points, BBs returning -12 basis points. We still see a substantial opportunity for increased discomfort surrounding China relations and Fed policy, and thus still favor the more defensive BB space, giving even more favorability to short duration credits up to 3 years.

High yield fund flows were a negative $115 million last week, making that the first week of outflows in over two months.

For the past month as a whole, July was a busy week for high yield new issuance with $24 billion coming to market on 33 separate deals, most of which coming from leverage buyout and mergers and acquisition activity. New issuance activity continued on in the first few days in August with $3 billion pricing on Thursday. Notable transactions were iHeart, the online radio company which issued $750 million of secured debt to take out a portion of their $3.5 billion term loan due 2026, and Mattel, which proactively raised funds to retire their 2020 maturities. Both deals saw healthy order books and tight pricing. Something to look for this week is to see if the drama in Washington will quiet the high yield primary markets in the coming week.

Energy markets saw weakness last week with WTI prices falling $0.54/bbl, or 1%, to $55.66/bbl. These falling prices included an 8% drop late in the week with Trump’s threats to impose tariffs significantly offsetting positive news in global demand.

Equities

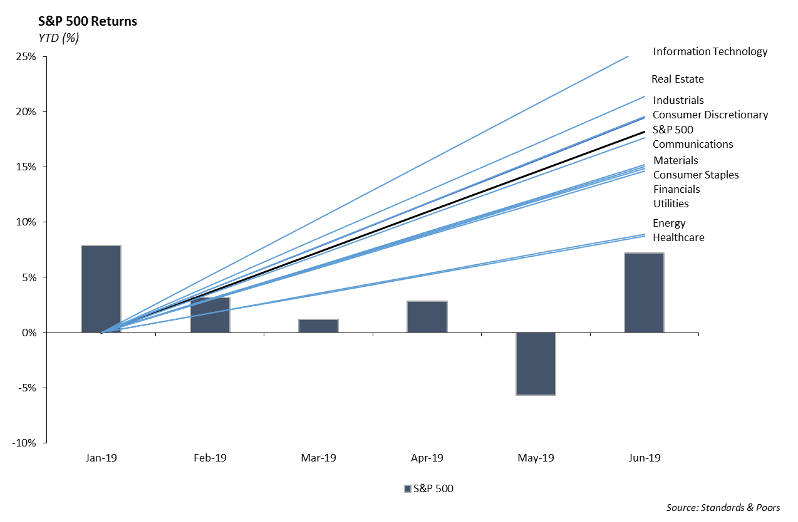

Last week, the S&P fell 3.10% to 2932, with most of its decline coming Wednesday through Friday on tariff concerns. Trump announced that on September 1 the U.S. will enact 10% tariffs on all goods from China. YTD, the S&P is up 17%. Again, we are seeing a shift into defensive sectors as volatility spikes. Info Tech, although the top performer YTD, saw declines of 4.4% last week, and was in the red with every other sector other than Utilities and Real Estate, which were up 0.25% and 2.05%, respectively. The market is continuing the decline in the morning with the DOW implied to open down over 300 points. We’re seeing the flight to safety in multiple avenues, with gold up to multi-year highs, the 10-year Treasury falling 9 bps to 1.76%, and even Bitcoin, up 9% to $11,000.

77% of companies in the S&P 500 have reported results, with 76% reporting a positive EPS surprise, and 59% reporting a positive revenue surprise. It has been a strong season in terms of EPS beat rates, and there is a good chance that the EPS growth number will be positive when earnings season concludes. The Blended earnings decline currently sits at -1.0%, which is still much above the pre earnings season predictions.

This week, Apple reported EPS of $2.18 vs $2.10 and revenue of $53.8 Billion vs. the $53.4 B estimate. Revenue was up 1%. iPhone revenue was lower than expected, falling 12%, and accounting for 48.3% of overall revenue. This is the first time it hasn’t contributed to over half of Apple’s sales since 2012. The positive was the wearables business: Apple watch and AirPods had beats with growth over 50%. They also outperformed in China, with $9.61 Billion in sales. China sales were down 22% last quarter; they were only down 4% this quarter. Apple Pay and App Store search ad business was up triple digits. The stock up 4%.

Portfolio Models

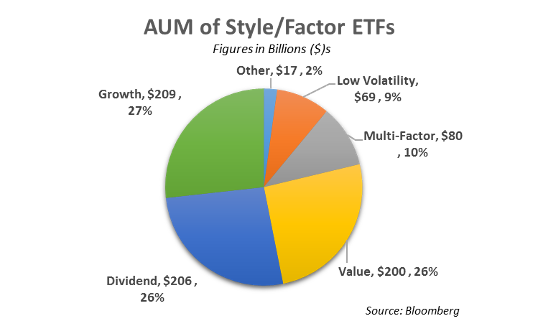

Low Volatility ETFs seek to buy the least volatile parts of market indices such as the S&P 500. Low Vol and Min Vol funds have garnered over $20B in inflows over the last year (over 38% organic growth), far outpacing other style/factor categories. Despite ample inflows, the style still remains a relatively small portion of overall style/factor assets at 8%. Year to date, the Low Vol Funds such as USMV and SPLV are up 19.60% and 19.06% respectively, slightly outpacing the S&P 500.

We believe low volatility funds are a great way to maintain equity exposure while volatility picks in the second half of the year. One fund we are looking at is the iShares MSCI Min Vol Fund (USMV). USMV is a sector neutral, low volatility strategy that maintains index sector weights, holding the lowest volatility stocks within each sector.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.