The Fed Takes Center Stage

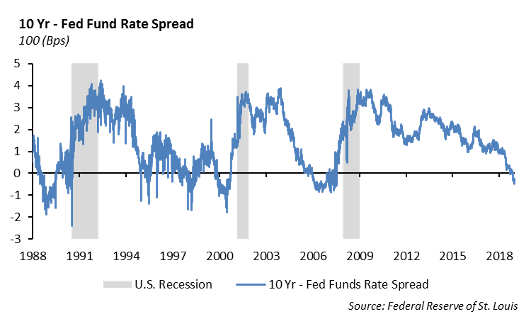

We are at the front end of earnings season and we expect some challenges with second quarter earnings. However, the market is focused on the heightened potential for the Federal Reserve to begin to lower interest rates. In two days of testimony in front of Congress, Fed Chairman Jerome Powell all but said out right that the next move by the Fed would be to lower rates beginning as early as this month. With an economy that is still growing, a tight labor market, unemployment rate at 3.7% and wage growth, the Fed has abruptly shifted to lowering rates. This is both peculiar and unprecedented for this monetary regime.

This Federal Reserve, under the current monetary regime following the Financial Crisis, has foreshadowed moves in short term interest rates as the central bank attempted to normalize policy after holding short term rates near zero. It has used words such as “data dependent” and “patient” to describe its decisions to incrementally move short term interest rates. After seven years of near zero interest rates, the Fed finally was able to begin raising rates in an attempt to normalize policy. Just last December, the Fed was considering its next move to raise rates. However, in an abrupt change in its communication, Powell has described an economy that is at risk of slowing given the uncertainty of the global slowdown and the China trade tariffs.

In 1995 and 1998 the Fed took small steps to lower the Fed Funds rate only to push rates higher as economic growth and inflation accelerated. The economic recovery following the Financial Recovery has been fragile and sustained economic growth challenging. If the economy slows and the Fed is unable to impact economic growth through lowering rates, we expect the next move will be to reignite its quantitative easing program.

Worth the Read

James Grant, the renowned author, financial market historian, founder and Editor of Grant’s Interest Rate Observer, has an essay published in the July 12, 2019 edition of the Wall Street Journal titled “The Fed Could Use a Golden Rule.” With the nomination of Judy Shelton to the Federal Reserve Board, talk of the gold standard has resurfaced. President Nixon moved the United States off the gold standard in 1971 effectively creating a fiat currency backed by a government promise to pay its bills on time. The untethering of the dollar has been a catalyst for the growth in debt. In today’s global monetary regime, with short term interest rates near zero, over $13 trillion of debt securities worldwide are priced to deliver a negative yield to the investor. If we went back to a gold standard, we would expect economic growth would be restricted to an untenable rate.

Fixed Income

After last week’s Powell testimony, markets continue to price in a near certain 25bps rate cut in July, but the chance of a 50bps cut in July remains unlikely. Regardless of whether we get 25 or 50bps of short term rate cuts, the likelihood of a rate cut in general and move back into an easy monetary policy period led to a sharp steepening in the curve. During the week, the 3-month treasury tightened 8bps, while the 30-yeaer treasury widened almost 10bps. The 10-year treasury was wider by 7.6bps, to end the week at 2.11%.

Investment grade spreads were essentially unchanged during a week that saw interest rate volatility and a larger than expected new issuance calendar. Micron and Panasonic both came with new deals more than four times oversubscribed and minimal concessions. ArcelorMittal on the other hand was not well received, and came with a 10bps concession to its existing debt and even widened once they traded in the secondary market.

We are struggling to generate meaningful buy ideas in the credit sector, which generally is a good indicator that the market is rich and investors should move up in quality. That is exactly what we have been doing over the past few weeks with the investment grade index now at 118bps. We see some value in Anheuser-Busch, which has widened 10bps after canceling the IPO of their Asian business.

Municipal Bonds

After a very slow start to July, the muni market was essentially a one-sided market last week, with demand far outpacing supply. Strength in the market led to the muni/UST ratio tightening by 5% and ended the week at 90%. California was a heavy issuer during the week, but demand was there with the average 10-year AA issue coming at 1.48%. This is 10bps inside the AAA muni curve.

We continue to believe that the technical behind the muni market will drive performance, despite looking relatively rich in historical terms. We are currently funding muni portfolios at a 2.15% yield to worst. For top tax bracket investors this offers a 3.63% tax equivalent yield, which is considerably better than the 3% an investor would earn buying 10-year A-rated corporates.

High Yield

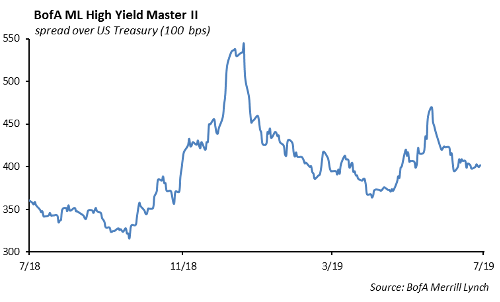

The U.S. high yield credit index widened 4 basis points to finish last week at an option adjusted spread of 402 basis points. This widening was based on technical pressures as heavy supply outweighed market sentiment on lower rates. The index is now 131 basis points tights of where the year started.

This spread widening came with negative total return as the index generated -0.03% last week. All risk tiers were negative with CCCs the underperformer at -0.11% total return. US high yield is still the best performing fixed income asset class year to date, returning 10.33% for investors. Year-to-date the story remains the same as it has been for about the last two months now with quality outperforming risk. BBs are just short of 11% total return year-to-date, while Bs sit at 10.12% return and CCCs are substantially underperforming at around 8.50% year-to-date total return.

High fund flows have remained positive for the fifth consecutive week at $619 million, following last week’s inflow of $802 million.

New issuance coming in at $4.6 billion month to date is a nice surprise in what is a traditionally very quiet month of high yield new issuance. Year to date new issuance volume is $136 billion, showing a 21% increase from the respective period last year. Notable transactions came from B issuers MTS Systems and Horizon Pharma, both of which had strong orders and pricing. Sinclair Broadcast is coming with a two part $4.9 billion acquisition financing that is expected to price this Saturday.

As we have been for the entirety of 2019, we remain defensive in high yield favoring BBs over their lower quality counterparts. An important development to consider in the BB space is the potential for refinancing and extension. With the drop in interest rates with US treasuries, we have seen average duration reduced to 3.8 years from 4.6 years at the start of 2019 and average dollar price up to $103 from the $95 we saw at the end of last December. We would expect issuers to consider using low interest rates to retire their high interest debt. We exercise caution in choosing to invest in high yield debt that the market has priced a negative yield to a near term call date.

Equities

The S&P added another 0.78% this past week, rising 0.46% on Friday and ending at 3014, sitting at all-time highs. The S&P is up 20.22% YTD. Info Tech is still the top performing sector at 30.90% YTD, while consumer discretionary is not too far behind, returning 26% YTD. Health care continues to trail returning just 6.8% YTD.

Second quarter earnings season kicked off with Delta and Pepsi both beating estimates. Delta earnings were $0.96 cents a share, beating estimates by 6 cents. It generated $10.47 billion, which jumped 5.1%. Delta’s revenue per seat mile also rose 2.4%. They have been unaffected by the problems with the 737 MAX jets from Boeing unlike Southwest and American who cut guidance and were both downgraded on cancelled flights. The stock jumped 2% on the record revenue numbers. With its dividend history, this was actually a recent addition to our Dividend Growth model, and we like the stock here.

Pepsi reported EPS of $1.54, which beat by 4 cents, and revenue of $16.45 billion. Healthier snacks and sparkling water helped its second quarter performance. Frito-Lay North America was its strongest performer again, rising 5% and its Quaker Foods business finally returned to growth as well. Organic revenue was up 4.5% The stock was up marginally on the day and up 20% YTD.

More than 50 companies are set to report this week including all of the major banks. Citigroup is reporting today and Blackrock, Schwab, JNJ, GS, WFC report tomorrow to start the week.

Portfolio Models

This week in Models we are bringing the Income Series back up. Our Income Series Model has four underlying strategies: Growth, Growth & Income, Moderate, and Conservative. Equity exposure varies per strategy, with the Growth strategy consisting of 82% equity, and the conservative strategy consisting of just 25% equity.

The purpose of this model series is to capture a strategic collection of Exchange Traded Funds paying out high income/dividends with the potential for price appreciation. Exchange traded funds in this model series are screened for Expense Ratio, Distribution Yields, Total Return, Fund Management, and Sharpe Ratios. Once screened, we choose the funds that best meet the above criteria to produce a high income paying portfolio of low expense Exchange traded Funds.

The Income Series is ideal for time periods in which volatility begins to spike and interest rates fall lower. As it becomes harder to find yield in the fixed income market and equites begin to look too risky, the income series masks the negative outlook for both by identifying ETFs that hold underlying fixed income and equity securities that continue to pay out income to investors.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.