Economy

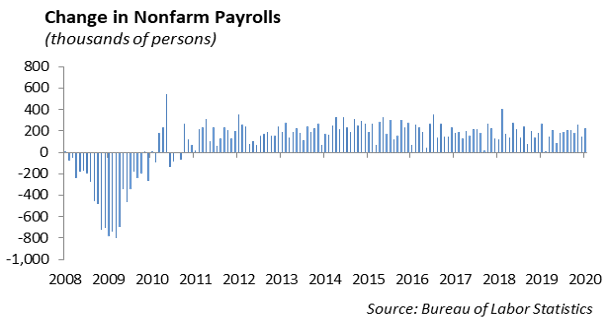

The economy received a boost Friday with the latest jobs numbers. The labor market strengthened again with the Labor Department reporting an increase of 225,000 jobs for January. At the same time, however, the unemployment rate ticked up to 3.6%, mostly as a result of more people entering the work force. In addition, wages climbed 3.1% on an annual basis, which helps support the notion that the tight labor market will result in wage growth. In turn, higher wages will support an increase in consumer spending.

The jobs gains were across industries, including leisure, hospitality and construction, which benefited from mild weather. The January report maintains a consistent string of monthly jobs reports that support a slow and steady recovery following the brutal impact of the Financial Crisis on the labor market. The rosy jobs number contrasts our thesis of an increase in lay-offs as companies trim headcount to support profit margins. Companies including Zimmer, CNO, Old National, John Deere and Lyft have all announced lay-offs recently.

Despite the healthy-looking jobs report, we expect the Federal Reserve may still lower short term interest rates as a result of the global economic slowdown caused by the coronavirus.

Equities

Overall, we are experiencing more volatility in equities driven by the global economic uncertainty caused by the coronavirus.

Earnings

Google reported earnings of $15.35 a share, which is up 20% and beat estimates. Revenue was $46.08 billion, which missed estimates, although it was still growth of 17.3. The interesting thing about this release was that it was Sundar’s first release as CEO, and for more transparency, they finally included a breakout of YouTube and cloud numbers in the report. YouTube ad revenue generated $15.15 billion in revenue in 2019, and $11.16 billion in 2018, which is 36% growth. Even though they gave us the numbers they kept it limited still, making it hard to gauge profitability. They did not report what percentage of ad revenue goes to creators. The cloud business had $8.92 billion in revenue in 2019, compared to $5.84 billion in 2018, which was 53% growth YoY. Although that seems high, if you compare to Azure from Microsoft which had 62% growth, it still is lagging. Obviously Google is much newer to the cloud game compared to AWS and Azure. The stock was down 3% after release of earnings and is actually the first FAANG stock to miss on revenue.

Disney+ had 26.5 million subscribers since its launch on November 12th. It has launched in U.S., Canada, Australia, New Zealand, and Netherlands. It will launch in Europe on March 24th, which will provide another big market. Initially, the forecast for subscribers was 60-90 million by 2024, and those numbers have not been updated in this report. Looking at its other streaming services, ESPN+ has 6.6 million subscribers, and Hulu has 30.4 million subscribers. Apple TV+ rolled out in November, AT&T has HBO Max, Comcast has Peacock in April, and now CBSViacom is releasing their own service as well so the competition in this space is at an all-time high.

Core Series

In the Core Series, we continue to shift the equity basis from a large cap growth bias in order to build downside protection. We have increased our exposure to dividend growth ETF’s.

We are planning on growing the income in this series through an increase of our dividend ETF, SCHD. The growth ETF currently makes up the majority of our large cap exposure. With a dividend yield of close to 3% among high quality large cap U.S dividend stocks, we are looking to increase this position in this series.

Core Sector Series

Communication Services – Overweight

Wireless demand is rising, the rollout of 5G appears promising, and ad revenue is strong for communication services. The top holdings in the sector are Facebook and Google. Although there have been privacy and regulation concerns, the sector has been able to navigate these problems effectively.

Consumer Discretionary & Consumer Staples – Neutral

Valuations seem to be fair value and in line with 5 Year averages. Consumer confidence is high and the unemployment rate is at historically low levels, but with quiet labor cutbacks and a weak manufacturing index that could bleed into the labor market, we remain neutral.

Energy – Neutral

We don’t believe geopolitical tensions can be considered a true catalyst, but the sector is at such a deep discount that we have chosen to remain neutral for now.

Financials – Overweight

We continue to be overweight in this sector, specifically in banks. We believe the banking sector will outperform due to continued consumer spending across credit cards and homes. Financials are also still the cheapest sector in the S&P. A sleeve of our position is made up of KBE, the SPDR Banks ETF.

Healthcare – Overweight

This sector has quite a few catalysts in our opinion. In general, you have an aging population, M&A spike, healthy balance sheets and finally the large pullback last year due to major legislative changes that now seem to be at very low risk of execution. This sector will retain a lot of focus heading into elections so we do expect volatility.

Industrials – Overweight

In this sector, we are overweight specifically in aerospace and defense. But with tentative trade agreements, we continue to like this sector.

Real Estate and Utilities – Underweight

We have seen rallies here with low interest rates and do not currently like the valuation of these sectors.

Technology – Overweight

Cloud growth is not appearing to slow down, and Apple and Microsoft stocks continue to push higher. In our Tech position, we like ticker IGV, the iShares Expanded Tech Sector ETF. This ETF offers exposure to high growth software companies that we like, such as Adobe, Salesforce, Oracle and Intuit. These are a lot of our top ideas that are found in our Focused Growth model and help provide a little bit of diversification away from Tech’s core holdings, Microsoft and Apple.

Fixed Income

Interest rates rode a rollercoaster through the last week. The 10-year treasury increased roughly 15bps at the beginning of the week, only to fall by 8bps later in the week. The 30-year ended the week at 2.04%. Unsurprisingly, global rates continue to experience downward pressure, and $13 trillion in negative yielding debt remains. The bottom line is that rates are low across the globe, so what are investors to do for income?

High Yield

U.S. high yield had an interesting week, with spread tightening almost 30 bps as investors’ worries on coronavirus subsided a bit, the index is still wide of year end levels. CCCs saw the best performance last week, and year-to-date are essentially tied with BBs in the total return category. Fund outflows slowed a bit last week as investors pulled $784 million out following an outflow of almost $3 billion the week before. The primary market in high yield was active last week with $14 billion of new paper coming into the market. The big deal this week will be Zayo Group, which may come with over $3 billion of both secured and unsecured debt to fund its buyout.

Energy markets were again down based on what should be less demand from China due to the virus. Reportedly, Chinese refiners are processing 15% less crude oil than before the outbreak. WTI fell 2% while natural gas rose 1%.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.