The World

It was fifty years ago this week that nearly half a million people met at Max Yasgur’s dairy farm in Bethel, New York for what would become known as Woodstock. The lineup included legends of rock including Janis Joplin, the Grateful Dead, Jimmy Hendrix, and the Who. Interestingly, the bands that were not playing included Led Zeppelin, the Byrds, Bob Dylan, who was a resident of Woodstock, and the Jeff Beck Group, who had disbanded just prior to Woodstock. The documentary film Woodstock, which was produced on a shoestring budget, won an academy award in 1970, and was credited with helping to save struggling Warner Brothers.

The 1960’s were shaped in part as a period in U.S. history where protests brought focus to the Vietnam War and dissatisfaction with political leadership. In contrast, Woodstock was considered an assemblage of peace and music.

Today, the protests in Hong Kong entered their 10th consecutive week this past weekend as protesters clashed with Police in violence. Beijing is growing frustrated with the protests and has threatened to send Chinese military if the Hong Kong police can’t get it under control.

Hong Kong operates with China as “one country, two systems,” and serves as an extremely important port for China; it is the capital gateway that links communist China with the western world. Roughly $1 trillion of capital each year flows between China and the world through Hong Kong. After Great Britain returned control of Hong Kong to China in 1997, China has been patient with closing its grip on the region. While the controversial extradition bill was the catalyst, the protests are now pushing for more democratic reforms. Along with the trade tariff war with China, we believe the protests in Hong Kong are a significant contributor to the heighted volatility in the U.S. capital markets.

Over the weekend, 50,000 citizens in Moscow protested Russian controls under President Vladimir Putin as the Russian economy sinks and the standard of living has fallen over the past five years. Similar to the United States, Russian citizens are using debt to help meet their monthly expenses. Russian citizens were debt free a generation ago. However, according to the country’s central bank, personal debt has doubled over the past five years and has reached $3,300 per person. With little prospect for wage growth, this will place a significant burden on Russia’s economy.

The Fed

Central banks around the world are loosening monetary policy and lowering short term interest rates. Last week, India, New Zealand, and Thailand lowered short term interest rates as the China – U.S. trade war intensified. We believe that the major central banks – including Europe, the United Kingdom and the United States – will continue to lower short term interest rates this year in an effort to stay in front of the global slowdown.

The increased risk of a hard Brexit at the end of October would be another catalyst to pump liquidity into the markets in order to mitigate the potential for a liquidity event.

Worth the Read

The Federal Reserve has announced a plan to develop a new round-the-clock, real-time payment and settlement service to support faster payments. The announcement can be found on the Fed’s website www.federalreserve.gov. We believe that the Federal government will want to own the digital currency and payment system. In a large part, we expect this initiative is a response to Facebook’s Libra currency and attempts to use cryptocurrency. With today’s technology, the wire transfer system appears antiquated. Any initiative the Fed puts forth to automate will be an improvement.

Fixed Income

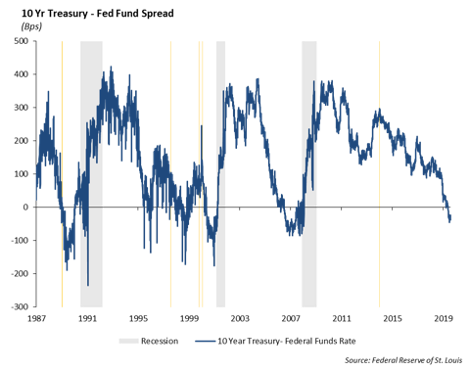

Who needs the Fed to lower rates when you have a trade war that has pushed rates lower by over 30bps across the curve in the past week? The 10-year US Treasury ended the week at 1.75%. Treasury curves have begun to flatten, and the 2 to 10-year curve flattened 15bps, now standing at only 10bps. We still believe flattening curves are not a signal of a recession, but we are remaining defensive.

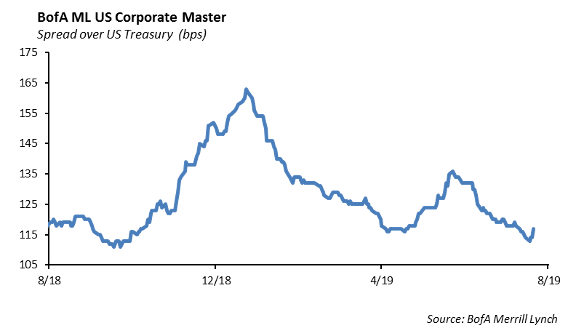

Investment grade spreads continued to widen during the week. Over the past two weeks, spreads have widened 15bps. This has created a buying opportunity for us to begin adding back to our credit exposure that we had taken off throughout the summer. We began adding to credit exposure by purchasing 10-year Boeing and Apple, which are trading at year to date wides. We also are participating in the new issuance market, which has provided increased concessions over the past two weeks. Last week, Occidental was the major focus, with a total book of $75bn for a total debt offering of $13bn to purchase Anadarko. Bonds tightened significantly on the break, but ultimately fell victim to the overall market widening. Currently, bonds are trading 2bps tight of issuance.

Municipal Bonds

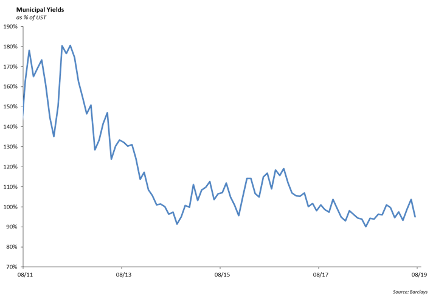

Muni yields have followed Treasuries lower, but have not been able to completely keep the pace. The 30-year muni ratio rose above 95% for the first time since April. Despite improving muni ratios, investors will have difficult decisions in buying muni’s as all tenors below 5 years are trading below 1%. We still caution investors from extending right now, and we believe muni’s can be a safe haven for investors in higher tax brackets during heighten volatility.

High Yield

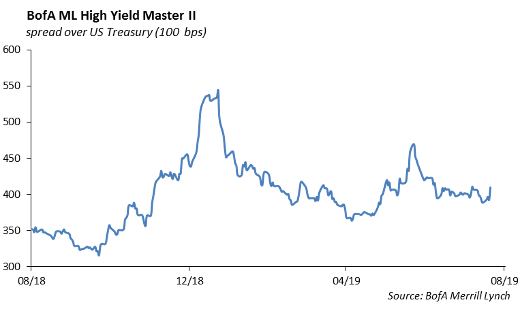

U.S. high yield credit continued its streak of consecutive spread widening, with most of the weakness happening at the beginning of last week. The 12 basis points of widening has the index sitting 102 basis points tight of year end 2018 levels. As a whole, the high yield credit market saw negative total returns, with the riskier tiers of CCCs and Bs leading the way. BBs actually saw positive total return to a tune of 0.05%. Last week, we broke back under the 10% year-to-date total return mark. BBs are still the outperformer on the year with YTD total return of 11.31%. This tier seems to gaining separation every week as migration to quality in high yield has been substantial.

High yield fund flows totaled $4 billion out of mutual funds and ETFs, marking the largest outflow since February 2018. We’re seeing money leave high yield pretty regularly now. However, investors remaining in the high yield space are shifting to the relative quality on of BBs, which has seemingly offset any losses the tier may take week over week.

The new issue market slowed down last week with $2.25 billion of volume. Two deals to note were Clear Channel Outdoor’s $1.25 billion offering and NCR Corporation $1 billion issuance. Clear Channel’s issuance priced passed the tights of price talk. While NCR’s issuance priced at price talk, bonds immediately tightened 20 bps off the break. We saw several potential high yield issuers pull their debt offerings due to volatility, including U.S. Farathane, Sirius Minerals, and Mattel.

With market volatility on everyone’s minds, there still appears to be opportunity and good reason to be involved in the corporate high yield space. With high yield bonds much more correlated to the equities than investment grade credits, any downturn in the stock market provides an entry point to back bid the street on high quality BBs names such as Ally Financial and Ball Corporation. These names, which generally trade at BBB levels help supplement additional income in investment grade portfolios while not sacrificing too much credit quality. The difference in credit quality between BBs and BBBs seems more muted than in years past. We pair this additional credit risk with remaining short duration, targeting maturities 3 years and in. Outside of short duration bonds, we still see value in longer-dated high yield new issuance. Investors are still starved for yield, and new issuance in high yield still provides significant concessions, highlighted by the NCR new issuance. Their 10yr split rated B-to-BB offering came at a yield to worst of 6.125% and immediately tightened more than 20 bps off the break. We caution investors from holding too many longer-dated high yield issuance over time as we still believe a credit downturn is looming.

Equities

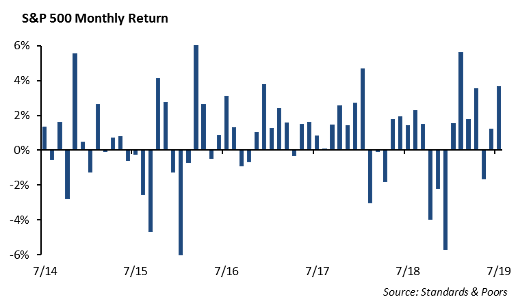

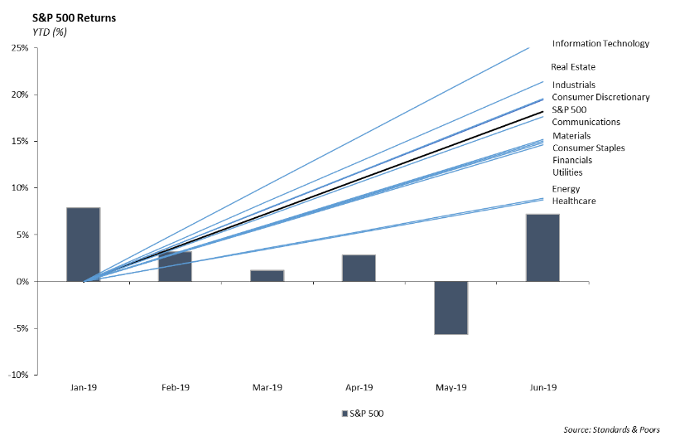

For the second week in a row, equity markets opened with a risk off mindset. Tech, consumer discretionary, and anything related to China was targeted heavily. Monday was the worst day for markets this year, with the S&P, DOW, and NASDAQ falling over 3%. Three days of recovery followed, and for the week, the S&P only saw declines of 0.46%. The index ended at 2918, which is up 16.43% YTD.

With declines like Monday’s, we seek opportunities to add to positions we have conviction behind. This week, we added to our position in Nike in our Large Cap Blend strategy. We believe there is value in Nike with revenue growth in all measures and in China, and the company has a depressed valuation to the discretionary sector as a whole. Other names on our buy list that we are looking to add to in a selloff period are MSFT, GOOGL, CSCO, PYPL, DIS and HON.

Technology fell 0.81% this week, and is down 1.30% MTD, and Communication Services was down 0.64% this week. We are still overweight in both sectors at this time. Energy has fallen 2.22% in the last week and is down 6.7% on a T1M basis. We continue to be underweight Energy in our models.

For Q2 2019, 90% of the companies in the S&P 500 have reported results. 75% of companies are reporting EPS above estimates, 57% are reporting sales above estimates. Blended earnings are currently at -0.7% decline.

Earnings this week include CSCO on Wednesday and Walmart on Thursday.

Portfolio Models

We are generally in a risk-off mode, and we believe results from expected returns on financial assets will be lower for the 2H19. We remain patient, however, and will add to the equity basis if the market sells off hard.

For Sector positioning, we remain underweight energy and overweight technology and communications sectors. Although we have been overweight Industrials most of the year, our thesis has shifted as there seems to be no relief in the ongoing trade war. We have been analyzing ETFs that offer exposure to the Aerospace and Defense Segment because we believe this sub-industry shows opportunity for future growth.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.