The Economy

We are at an inflection point. The economy is sputtering and showing signs of unexceptional growth. Last week, the Commerce Department released that employment increased by 1.2 million jobs and the unemployment rate fell to 10.2%. Also, the ISM Manufacturing survey moved to 54.2, underscoring some growth in manufacturing.

However, sustained economic growth is a long way off. The economy requires tremendous support in order to prevent a collapse and allow it to continue to grow. Meanwhile, Congress has been unable to agree on a fourth stimulus bill. So, this past weekend, President Trump signed by executive order several initiatives to provide additional stimulus, including additional unemployment benefits of $400 per week in aid.

With students going back-to-school and fall sports programs in limbo, business activity typically associated with the late summer is extremely slow. Back-to-school sales are slow, and we expect the college football season to be cancelled. The steps taken to keep people safe, such as social distancing and limiting large gatherings, continues to hurt economic growth. Until there is a way to control the spread of the virus, we expect these measures to remain in place and economic growth to falter.

We do not expect a V-shaped recovery in the economy. In fact, we expect economic growth to languish as parts of the economy remain inoperable. In spite of the pandemic, consumption has held up relatively well through the summer due to the financial assistance provided through the Cares Act. Without continued financial assistance, however, consumer demand could fall off a cliff.

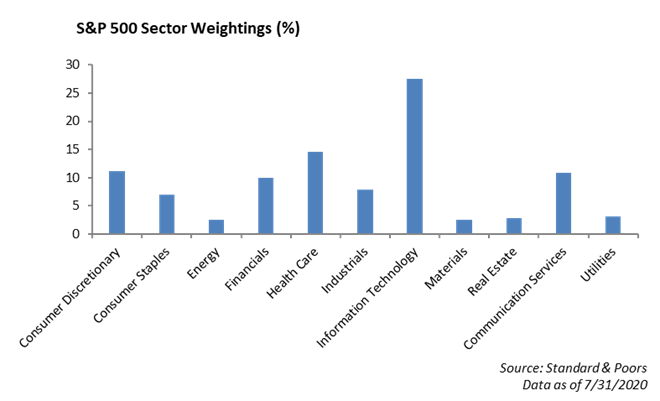

Equity

The shape of the S&P 500 benchmark has changed dramatically over the past year. Energy now makes up less than 3% of the index. The strength in technology has pushed its allocation to almost 30% of the index. As the economy continues to find a way to move through the pandemic, we are changing our sector allocations across portfolio models and equity strategies to set up portfolios for success through the second half of the year. Below is a breakdown of the S&P sector allocations:

UNDERWEIGHT SECTORS

Utilities: Underweight

This sector will usually outperform during times of uncertainty due to stable demand. During the pandemic, people will need water and electricity despite the current environment. However, this sector continues to trade at high valuation levels given the attractive dividend deals they pay. Moving forward through the pandemic, this sector is not set up to provide the safety net investors are looking for.

Real Estate: Underweight

There is currently low demand for properties and a high risk to cash flows for companies within this sector. The retail space is under stress as many companies are struggling to pay their rent. In addition, multifamily lease defaults are expected.

Materials: Underweight

The Materials sector has a negative outlook for the second half of the year due to the trading relationship between the United States and China and unstable economic environment amid the pandemic. A majority of top constituents within this sector are gas companies, which continue to see weak demand. Finally, there is low demand for chemicals and agriculture.

OVERWEIGHT SECTORS

Consumer Discretionary: Overweight

The Consumer Discretionary sector includes many industries that have been significantly impacted by the spread of COVID-19, such as hotels, autos, and apparel. Fundamentals within the sector will continue to be challenged, and consumer confidence will remain uncertain as COVID cases continue to spike. However, these difficulties are countered by the market cap of Amazon, which makes up a majority of the sector. The sector’s market cap in the internet retail industry outweighs the challenges faced by tested companies.

Industrials: Overweight

The airline industry continues to struggle as the recent spike in COVID cases challenges the possibility of sustained demand in the next several months. Earnings expectations have been negative for Industrials, falling by over 50% in the last quarter. However, we believe this sector is a good rebound play once the economy begins to recover. The Manufacturing Index has shown signs of improvement, and as a higher beta sector, the current market rally will continue to help in the near term.

Technology: Overweight

Demand within the Technology sector has been very high and will continue to remain high during the stay at home work environment. The large allocation to Microsoft and Apple give this sector stability when looking at the downside case. Earnings have not been affected by economic uncertainty, and the sector has benefited from the pandemic while other industries have suffered.

Communication Services: Overweight

Advertising focused companies have faced headwinds during the pandemic. However, increased demand for streamed entertainment and social media has positively impacted the Communication Services sector. Gaming companies, such as Activision and EA, have also seen a surge in demand, which will continue to push this sector forward.

Energy: Overweight

The Energy sector has been fundamentally challenged for an extended period. Oil is now $40/ barrel, and energy giants, Exxon and Chevron, make up almost half of this sector. With valuations so low and oil prices improving, there could be some upside in the near term.

NEUTRAL SECTORS

Healthcare: Neutral

HealthCare reform will be a focus with 2020 elections, causing volatility to increase within the sector. Chances of legislative changes are low but discussions always cause spikes in volatility. COVID is more of a double-edged sword. Certain sectors can benefit from tests and vaccines, but others will see fewer diagnostic tests, surgeries, and prescriptions.

Consumer Staples: Neutral

Typically, the consumer staples sector is a stable group when there is economic uncertainty. During this pandemic, consumers will continue to buy necessities such as food and cleaning supplies despite the current economy. However, if the market continues to rally, this could mean continued stagnation for the defensive sector.

Financials: Neutral

Extreme underperformance for Financials thus far makes valuations attractive. Earnings of the big banks confirmed stabilization within this sector. We believe the boost in demand from fixed income trading has now passed, and the necessary increase in loan loss reserves will be a headwind against continued low net interest margins.

Fixed Income

Fixed income markets experienced a rather quiet week as both rates and spreads were essentially unchanged. The 10-year US Treasury ended the week at 0.56%. Corporate new issuance did pick up during the week. Issuance came from higher quality issuers that are not frequently in the market, such as Google, AstraZeneca, and Regeneron. While concessions were very small, post issuance performance was strong. Most issues tightened 5bps as they began to trade, and spreads tightened even further during the days following issuance.

We have been active in new issuance and have found it to be the best place to extract performance out of an overvalued and very correlated market. Across our fixed income strategies, we continue to move up in quality and reduce credit exposure at the margin. We have been quick to sell performing new issues and play defense as we are finding less and less value in the market.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.