Does an Inverted Yield Curve Really Matter?

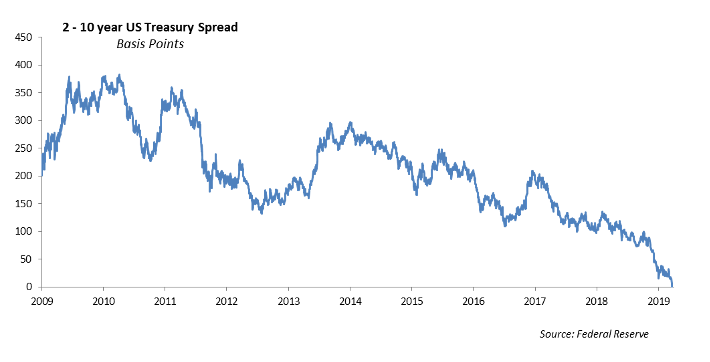

While the yield curve has flattened significantly, the yield difference between the 10 year and 2 year U.S. Treasury notes went negative -2 bps this past week. Out of the last seven times that the yield curve has inverted, six of them have resulted in a recession.

The media tends to substitute the word “recession” for a broad downturn in economic growth. However, a recession is two consecutive quarters of negative growth which underscores a contraction in the economy. We believe Gross Domestic Product, the output of our economy, is growing at roughly 1.6% annual.

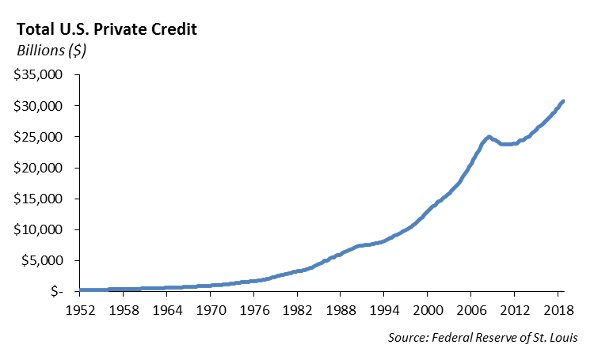

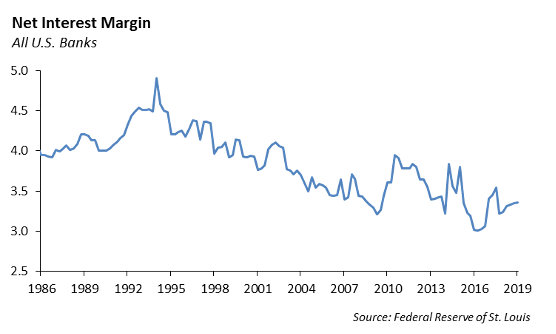

Our economy is fueled by credit, which is generated through our financial system. Private credit is the gasoline that runs the economic engine. Our financial system is leveraged and supported primarily by the banking system. When long term interest rates yield lower than short term interest rates, the leverage in the system is no longer positive. As a result, private credit expansion slows and net interest margins at banks contract.

With the yield on both the 10 year and the 2 year U.S. Treasury note trading below 2%, there has never been an inversion in the domestic yield curve at these low levels of interest rates. There is sufficient evidence that the U.S. economy is slowing; however, the inversion in the yield curve at these low rate is less meaningful given the lack of “carry trade” in the system.

In addition, the length of time that the curve needs to be inverted in order to have an impact on the behavior of investors is roughly three to six months. In other words, we would expect a sustained inversion in the curve to have an impact on investor behavior, and it will take time to assess the impact on the flow of credit.

Finally, the average net interest margin for the domestic banks is near 3.36% for 1Q 2019. As long as NIM is above 3.0% we expect the banks are making money. With a sustained inverted yield curve, we would expect to see compression on NIM for the banks.

The Economy

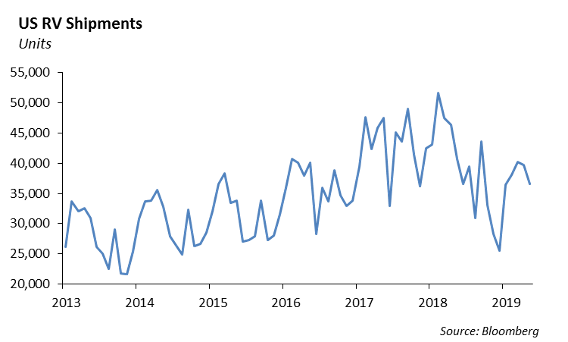

One of our favorite leading economic indicators is the total wholesale shipments of recreational vehicles reported by the RV Industry Association. So far this year, wholesale shipments of recreational vehicles are down 20.3%. As consumers pull back on spending, large discretionary purchases are postponed. Recreational vehicle sales are one of the most volatile sectors for consumers and a general predictor of what is happening in the economy. It is hard to tell if the trade tariffs with China are having an impact on the industry. But, generally speaking, slower RV shipments portend a slowing economy.

Fixed Income

Rates continued to fall last week, as weak global economic data kept bids on U.S. treasuries strong. We saw the curve continue to flatten, with the 30-year treasury dipping below 2 percent for a time. Like discussed earlier, the 2s10s curve did actually invert for about 20 minutes last week, while the 3-month rate is only sitting 15-20 basis points inside the 30-year. We saw President Trump delay some tariffs on Chinese imports, after the threat of these tariffs drove much of the selloff in early August. The positive effect this had on the market was short lived as disappointing results in China and Europe continue to drive U.S. rates lower. This week is pretty light on economic data with the July Fed minutes probably being the most watched release.

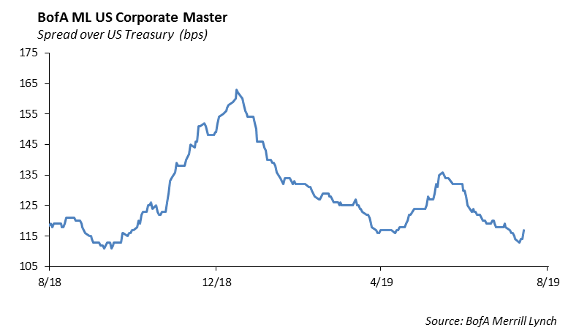

Investment grade spreads widened 2 to 6 basis points depending on rating tier. Investors appear to be reducing credit positions as fear of a looming recession has picked up. We also believe that investors will continue to lighten up on credit as liquidity seems to lessen up in the fall. Because of this we believe that there is no catalyst for U.S. rates to rise and would expect the yield curve to continue to drop or at the very least keep current levels consistent. We will take this opportunity to selectively increase our credit positions in higher quality “go-go” names and new issues that provide a healthy concession. Despite the recent volatility, companies are still tapping in the new issue market, happily trading off wider spreads with very low yields to fund M&A activity. We saw M&A activity from several companies such as VMware, Broadcom, CBS & Viacom, and high yield issuer CIT.

High Yield

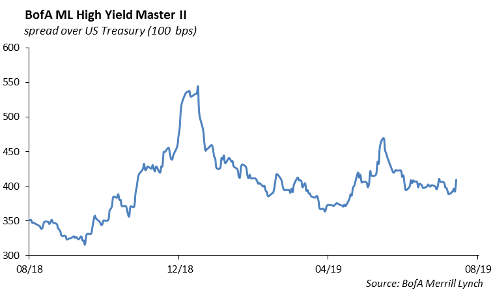

We saw much more spread widening in high yield last week as the index widened out 16 bps, losing about 15 basis points of total return. BBs still remain the best performer in the space as investors are firmly moving into a more defensive position and satisfactorily taking their 10 percent total return for the year. We expect the high yield secondary market to follow the stock market’s lead in volatility, and remain cautious in evaluating seemingly cheap entry points. New issue in high yield slowed down to almost a halt, with only 1 new issue taking place in Tenet Healthcare’s $4.2 billion senior secured notes. Tenet is a relatively well known high yield issuer and we saw the deal have good demand and priced to the low end of initial price talk. The high yield primary market is expected to remain quiet through Labor Day cementing the August as one of the weakest in recent memory.

In energy markets, WTI crude oil rose $0.37/bbl or 1%, breaking a two week losing streak.

Equities

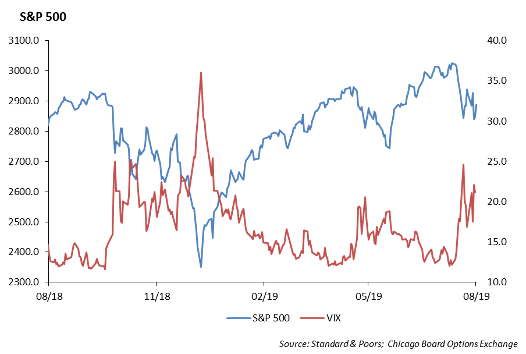

The S&P fell about 1% this week, ending at 2888. This is still up 15.23% YTD and is about 4.62% from all-time highs. The pullback is the second pullback this year of 5% or more. Since 2009, there has been a 5% pullback once every 122 days, or about 3 per year.

At this level, the S&P is just above our fair value range at $175 in earnings with 2% growth at 16 times. August is the second lowest average trading volume of any month of the year next to December, and with the lack of catalysts, earnings season ending and no Fed meetings, any headline that hits will move the market with these lower trading volumes.

The administration delayed the planned 10% tariffs on a good portion of consumer goods until Dec 15th but will still implement tariffs starting Sep 1. With staggered tariffs, there are more rooms for talks, although we do not believe we are closer to a long term deal, so expect continued volatility with geopolitical questions with a potential China response and protests in Hong Kong.

Looking at sector performance, Info Tech is still the top performer returning about 26% YTD. Although the most volatile sector, it has recovered nicely each time it has taken a hit, we like the sector as a whole and would add on any meaningful dips. The underperformer this year is Energy which is the only sector in the red, down 1%.

In specific earnings news, Walmart released a solid earnings report this week, the stock was up 6%. EPS came in at $1.27, a 5 cent beat. Revenue was $130.38 Billion which were up 1.8%, same store sales were up 2.8% vs 2.1% expected. E-commerce sales were up 37%, which stayed the same. With its rollout of next day delivery, online sales saw a nice rise. NextDay delivery covers ¾ of the population. Sam’s Club same-store sales grew 1.2%, which also beat estimates. They did mention tariffs will continue to put pressure on prices, as only a third of their products are brought in internationally. But all in all, good numbers from Walmart. Walmart is now up 21% YTD.

Portfolio Models

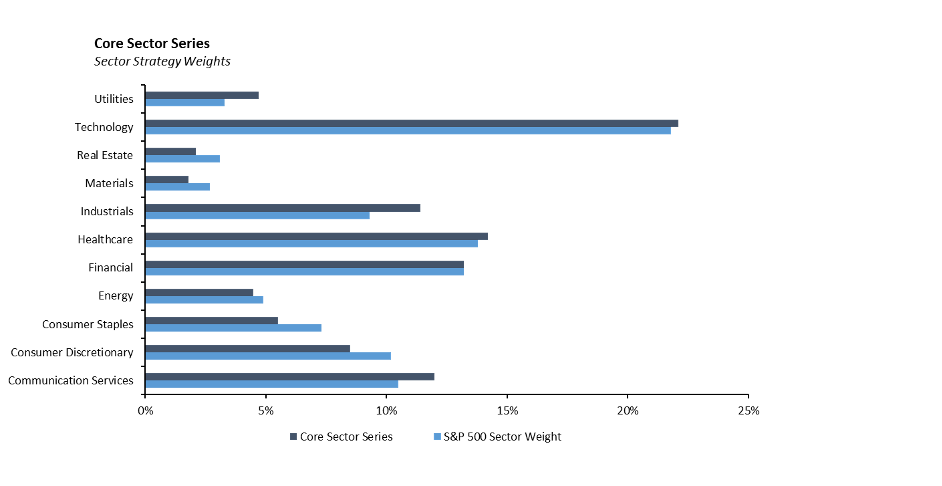

This week in models, the Core Sector Series is the topic of choice. With volatility picking up and uncertainty looming in the global economic landscape we continuously bring up sector exposure in our Investment Committees.

The Core Sector Series focuses on long term capital appreciation through the use of strategically selected sector ETFs. YTD we have seen technology, Real Estate and Consumer Staples lead the returns while Energy and Health Care have lagged. We are overweight Communications, Information Technology and Utilities in our Core Sector Series Models. We also are overweight Aerospace & Defense, a sub-sector of the Industrial industry. We see the industrial industry as a whole slowing from the trade disputes with China, higher input costs, and slower global growth. However, Aerospace & defense still remains attractive, remaining less cyclical than the industry as a whole and generating most of its revenue from the U.S. Military Spending (Expected U.S. military spending is $989 Trillion for the period of October 1, 2019 through September 30, 2020; This would be a 3.40% growth rate from estimated 2019 and 11% higher than actual 2018).

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.